3 ASX Stocks Estimated To Be Trading Up To 44.5% Below Intrinsic Value

Reviewed by Simply Wall St

Over the last 7 days, the Australian market has remained flat, yet it has risen 15% in the past 12 months with earnings expected to grow by 12% per annum over the next few years. In this context, identifying undervalued stocks can be a strategic move for investors looking to capitalize on potential growth opportunities.

Top 10 Undervalued Stocks Based On Cash Flows In Australia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Ingenia Communities Group (ASX:INA) | A$5.21 | A$9.40 | 44.6% |

| Medibank Private (ASX:MPL) | A$3.66 | A$6.48 | 43.5% |

| MLG Oz (ASX:MLG) | A$0.63 | A$1.16 | 45.7% |

| Ansell (ASX:ANN) | A$31.69 | A$56.23 | 43.6% |

| Megaport (ASX:MP1) | A$7.31 | A$13.50 | 45.8% |

| Genesis Minerals (ASX:GMD) | A$2.15 | A$3.96 | 45.7% |

| Charter Hall Group (ASX:CHC) | A$16.25 | A$29.26 | 44.5% |

| Millennium Services Group (ASX:MIL) | A$1.145 | A$2.24 | 48.9% |

| Little Green Pharma (ASX:LGP) | A$0.09 | A$0.17 | 46.8% |

| Superloop (ASX:SLC) | A$1.665 | A$3.31 | 49.7% |

Let's take a closer look at a couple of our picks from the screened companies.

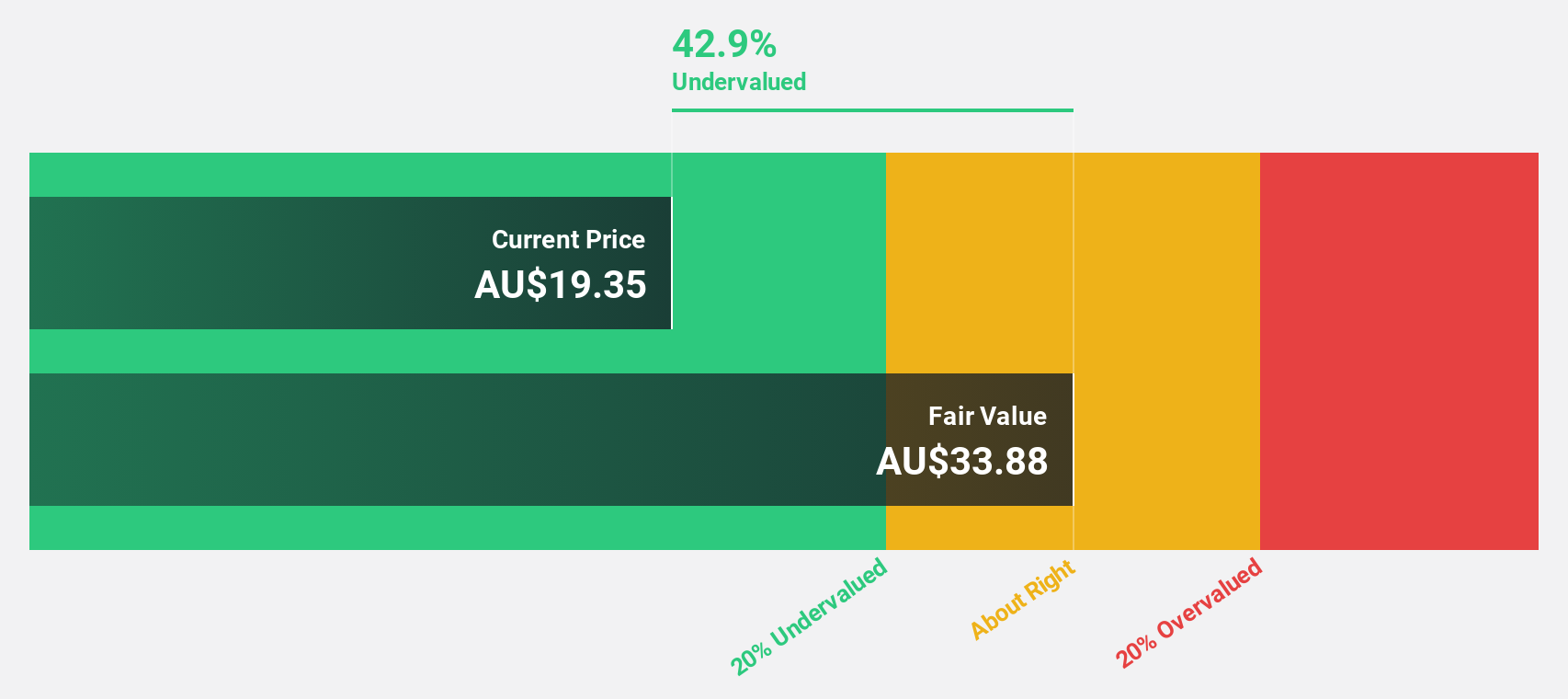

Charter Hall Group (ASX:CHC)

Overview: Charter Hall Group (ASX:CHC) is a leading Australian fully integrated property investment and funds management company with a market cap of A$7.69 billion.

Operations: Charter Hall's revenue segments include Funds Management (A$448.60 million), Property Investments (A$322.80 million), and Development Investments (A$73.30 million).

Estimated Discount To Fair Value: 44.5%

Charter Hall Group appears undervalued, trading at A$16.25, significantly below its estimated fair value of A$29.26. Despite a recent net loss of A$222.1 million for FY24, the company forecasts post-tax operating earnings growth of 4% and distribution growth of 6% for FY25. Analysts expect annual revenue growth of 8.3% and a return to profitability within three years, suggesting potential upside based on cash flow analysis.

- The analysis detailed in our Charter Hall Group growth report hints at robust future financial performance.

- Dive into the specifics of Charter Hall Group here with our thorough financial health report.

Duratec (ASX:DUR)

Overview: Duratec Limited (ASX:DUR) provides assessment, protection, remediation, and refurbishment services for steel and concrete infrastructure in Australia with a market cap of A$365.11 million.

Operations: Duratec's revenue segments include Energy (A$46.64 million), Defence (A$220.16 million), Buildings & Facades (A$111.33 million), and Mining & Industrial (A$155.64 million).

Estimated Discount To Fair Value: 43.5%

Duratec Limited, recently added to the S&P Global BMI Index, appears undervalued with a current trading price of A$1.47 against an estimated fair value of A$2.60. The company reported FY24 sales of A$555.79 million and net income of A$21.43 million, with earnings per share increasing from the previous year. Despite a dividend decrease, Duratec's revenue is forecast to grow at 7.3% annually, outpacing the broader Australian market's growth rate and supporting its undervaluation based on cash flow analysis.

- Our earnings growth report unveils the potential for significant increases in Duratec's future results.

- Unlock comprehensive insights into our analysis of Duratec stock in this financial health report.

Sandfire Resources (ASX:SFR)

Overview: Sandfire Resources Limited, with a market cap of A$4.74 billion, is a mining company involved in the exploration, evaluation, and development of mineral tenements and projects.

Operations: The company's revenue segments include the Motheo Copper Project with $346.47 million, MATSA Copper Operations generating $565.68 million, and Degrussa Copper Operations contributing $29.40 million.

Estimated Discount To Fair Value: 29.9%

Sandfire Resources, recently added to the S&P/ASX 100 Index, trades at A$10.37, below its estimated fair value of A$14.79. Despite a net loss of US$17.35 million for FY24, revenue grew to US$935.19 million from US$803.97 million previously. Forecasts indicate an 8.8% annual revenue growth and profitability within three years, supporting its undervaluation based on cash flows and future earnings potential despite current challenges in return on equity projections (12%).

- The growth report we've compiled suggests that Sandfire Resources' future prospects could be on the up.

- Click to explore a detailed breakdown of our findings in Sandfire Resources' balance sheet health report.

Next Steps

- Navigate through the entire inventory of 41 Undervalued ASX Stocks Based On Cash Flows here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:CHC

Charter Hall Group

Charter Hall is one of Australia’s leading fully integrated property investment and funds management groups.

Excellent balance sheet established dividend payer.