- Australia

- /

- Capital Markets

- /

- ASX:L1G

L1 Group (ASX:L1G): Assessing Valuation After a 52% Year-to-Date Share Price Surge

Reviewed by Simply Wall St

L1 Group (ASX:L1G) has quietly delivered a strong year so far, with shares up more than 50% YTD as investors reassess its earnings growth, capital-light model and performance-driven fee streams.

See our latest analysis for L1 Group.

That strength is not just a one off spike, with the latest A$1.06 share price sitting on a solid year to date share price return of around 52 percent that signals positive momentum as investors lean into its scalable fee engine.

If L1 Group has you watching quality capital light models more closely, it is worth scanning for other opportunities using our screener of fast growing stocks with high insider ownership.

With earnings still growing double digits but the share price already running hard, is L1 Group an overlooked compounder trading below its true worth, or is the market already baking in years of fee driven expansion?

Price to Earnings of 33.2x: Is it justified?

L1 Group's current A$1.06 share price equates to a price to earnings ratio of 33.2 times, which screens as expensive against key benchmarks.

The price to earnings multiple compares what investors are paying today for each dollar of L1 Group's earnings, a common yardstick for capital markets businesses. With earnings forecast to grow in the mid teens annually and revenue expected to outpace the broader Australian market, this richer multiple suggests investors are already paying up for sustained, high quality profitability.

Compared to the wider Australian Capital Markets industry average of 21.9 times earnings, L1 Group trades on a markedly higher valuation, indicating the market is assigning it a premium status. However, when set against a peer group average of 68.1 times earnings, its 33.2 times multiple looks far more restrained, implying the stock may sit in a middle ground where investors recognise its growth and earnings quality but have not pushed it to the extremes seen elsewhere.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price to Earnings of 33.2x (ABOUT RIGHT)

However, risks remain, including the share price trading above analyst targets and reliance on ongoing performance fees in volatile markets.

Find out about the key risks to this L1 Group narrative.

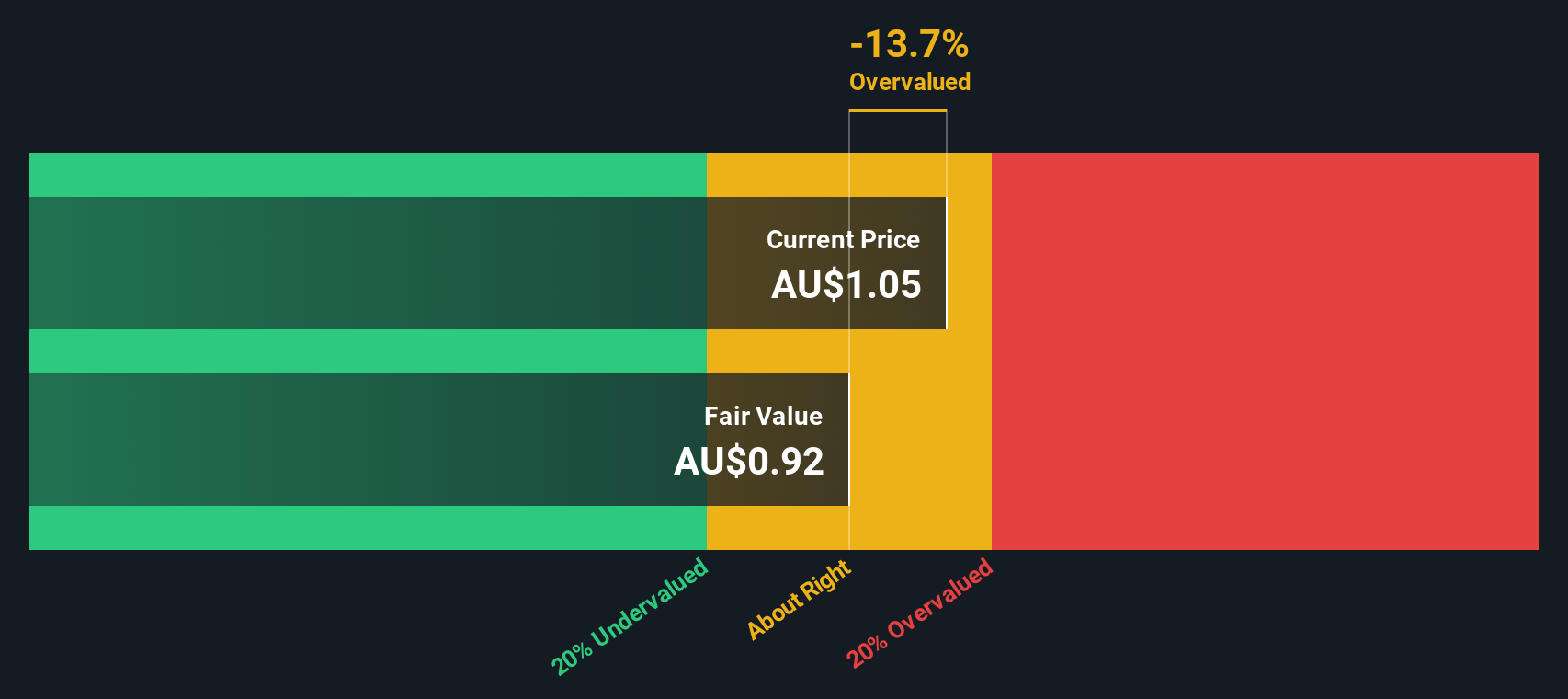

Another View on Value

Our DCF model paints a cooler picture, with L1 Group’s A$1.06 share price sitting above an estimated fair value of about A$0.91, which implies it may be modestly overvalued. Is the market rightly paying up for a durable fee engine, or getting ahead of itself?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out L1 Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 905 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own L1 Group Narrative

If you see the numbers differently, or would rather test your own assumptions, you can build a personalised view in just a few minutes: Do it your way.

A great starting point for your L1 Group research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Before you move on, lock in an edge by lining up your next opportunities with fresh, data driven stock ideas tailored to different strategies and themes.

- Explore potential multi baggers early by scanning these 3609 penny stocks with strong financials that already support their growth stories with improving fundamentals.

- Focus on these 25 AI penny stocks that combine artificial intelligence with scalable business models and rising demand.

- Consider these 905 undervalued stocks based on cash flows where current prices may not fully reflect the strength of their future cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:L1G

Reasonable growth potential with imperfect balance sheet.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Unicycive Therapeutics (Nasdaq: UNCY) – Preparing for a Second Shot at Bringing a New Kidney Treatment to Market (TEST)

Rocket Lab USA Will Ignite a 30% Revenue Growth Journey

Dollar general to grow

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Trending Discussion