- Australia

- /

- Hospitality

- /

- ASX:FLT

Unveiling 3 High Insider Ownership ASX Growth Companies With Up To 23% Earnings Growth

Reviewed by Simply Wall St

The Australian stock market has shown robust performance today, with the ASX200 climbing approximately 0.9%, buoyed by a strong showing on Wall Street and broad gains across all sectors. In this climate of overall market positivity, companies with high insider ownership can be particularly compelling, as they often indicate a management team deeply invested in the company's success and aligned with shareholder interests.

Top 10 Growth Companies With High Insider Ownership In Australia

| Name | Insider Ownership | Earnings Growth |

| Cettire (ASX:CTT) | 28.7% | 26.7% |

| Acrux (ASX:ACR) | 14.6% | 115.3% |

| Clinuvel Pharmaceuticals (ASX:CUV) | 13.6% | 26.7% |

| Biome Australia (ASX:BIO) | 34.5% | 114.4% |

| Liontown Resources (ASX:LTR) | 16.4% | 59.4% |

| Ora Banda Mining (ASX:OBM) | 10.2% | 92.9% |

| Plenti Group (ASX:PLT) | 12.8% | 106.4% |

| Hillgrove Resources (ASX:HGO) | 10.4% | 45.4% |

| Change Financial (ASX:CCA) | 26.6% | 76.4% |

| DUG Technology (ASX:DUG) | 28.1% | 43.2% |

We'll examine a selection from our screener results.

Emerald Resources (ASX:EMR)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Emerald Resources NL is involved in the exploration and development of mineral reserves in Cambodia and Australia, with a market capitalization of approximately A$2.60 billion.

Operations: The company generates revenue primarily through mine operations, which amounted to A$339.32 million.

Insider Ownership: 18.5%

Earnings Growth Forecast: 23.1% p.a.

Emerald Resources is positioned intriguingly within the Australian market, with earnings expected to increase at a robust rate of 23.08% annually, surpassing the national average of 12.9%. Revenue forecasts also outpace general market projections, aiming for an 18.6% yearly growth against a modest 5.3%. However, shareholder dilution over the past year tempers this optimism slightly, despite no significant insider trading activities reported in recent months.

- Delve into the full analysis future growth report here for a deeper understanding of Emerald Resources.

- In light of our recent valuation report, it seems possible that Emerald Resources is trading beyond its estimated value.

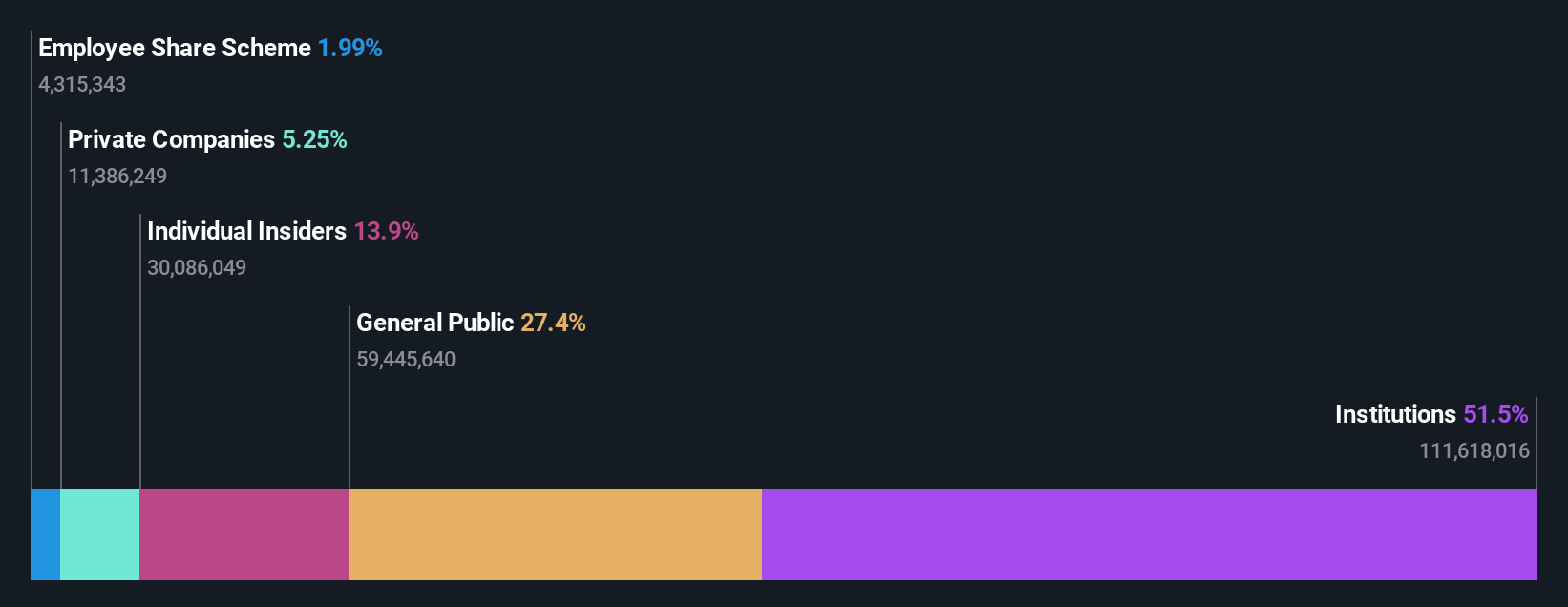

Flight Centre Travel Group (ASX:FLT)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Flight Centre Travel Group Limited operates as a travel retailer serving both leisure and corporate sectors across Australia, New Zealand, the Americas, Europe, the Middle East, Africa, and Asia with a market capitalization of approximately A$4.75 billion.

Operations: The company generates revenue primarily through its leisure and corporate travel services, with the leisure segment bringing in A$1.28 billion and the corporate segment contributing A$1.06 billion.

Insider Ownership: 13.3%

Earnings Growth Forecast: 18.8% p.a.

Flight Centre Travel Group, trading significantly below its estimated fair value, shows promise with earnings expected to grow by 18.84% annually and revenue projected to increase at 9.7% per year—outpacing the Australian market's average of 5.3%. Despite this growth, there is no substantial insider buying or selling reported recently. The company has turned profitable this year and its Return on Equity is anticipated to be high at 21.8% in three years' time.

- Dive into the specifics of Flight Centre Travel Group here with our thorough growth forecast report.

- Our expertly prepared valuation report Flight Centre Travel Group implies its share price may be lower than expected.

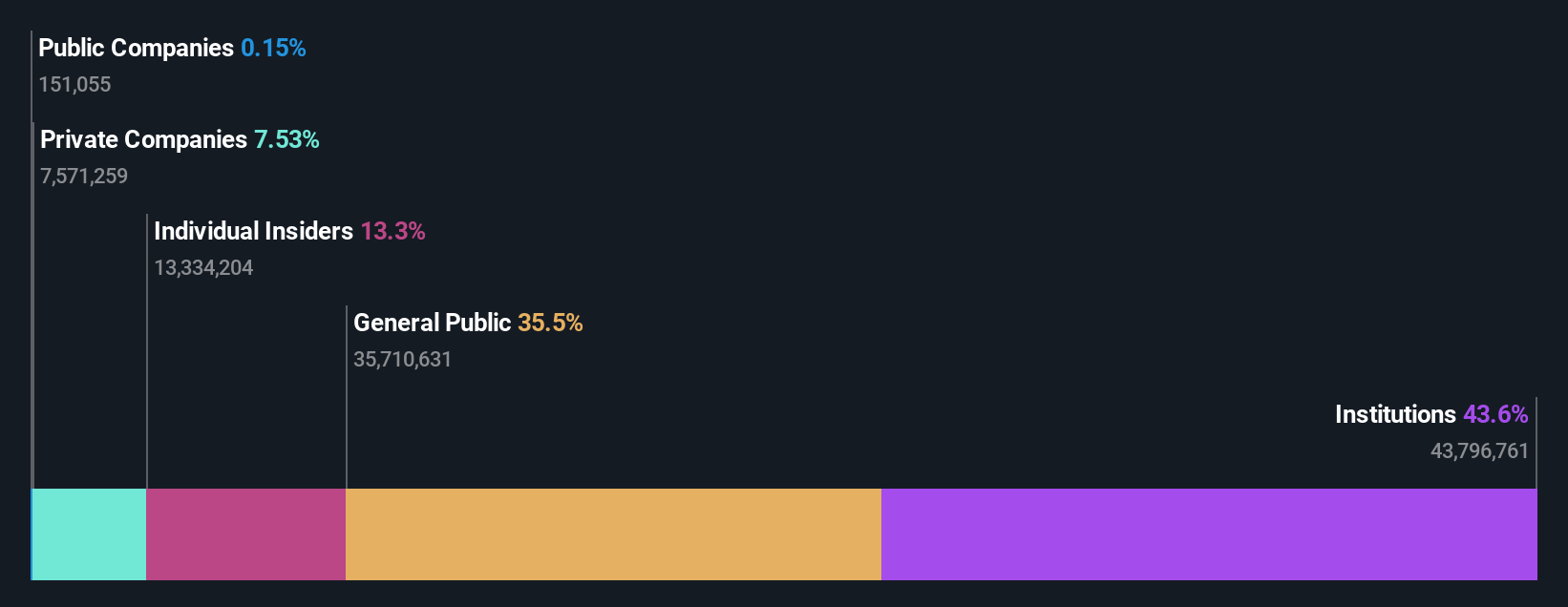

PWR Holdings (ASX:PWH)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: PWR Holdings Limited specializes in the design, prototyping, production, testing, validation, and sale of cooling products and solutions across multiple countries including Australia, the US, and several European nations, with a market capitalization of approximately A$1.17 billion.

Operations: The company generates revenue primarily through two segments: PWR C&R, which brought in A$37.35 million, and PWR Performance Products, contributing A$104.44 million.

Insider Ownership: 13.4%

Earnings Growth Forecast: 15.4% p.a.

PWR Holdings is poised for robust growth with earnings expected to rise by 15.4% annually, surpassing the Australian market's average of 12.9%. The company's revenue growth forecast at 12.9% per year also outstrips the general market prediction of 5.3%. Additionally, PWR Holdings maintains a strong insider commitment, evident from recent months where insiders bought more shares than they sold, although not in substantial volumes. This aligns with a high forecast Return on Equity of 30.6% in three years, signaling potential strength in financial performance and governance.

- Click here to discover the nuances of PWR Holdings with our detailed analytical future growth report.

- According our valuation report, there's an indication that PWR Holdings' share price might be on the expensive side.

Turning Ideas Into Actions

- Click here to access our complete index of 92 Fast Growing ASX Companies With High Insider Ownership.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:FLT

Flight Centre Travel Group

Provides travel retailing services for the leisure and corporate sectors in Australia, New Zealand, the Americas, Europe, the Middle East, Africa, Asia, and internationally.

Undervalued with excellent balance sheet.