Advertisement

UNIQA Insurance Group (VIE:UQA) Is Increasing Its Dividend To €0.57

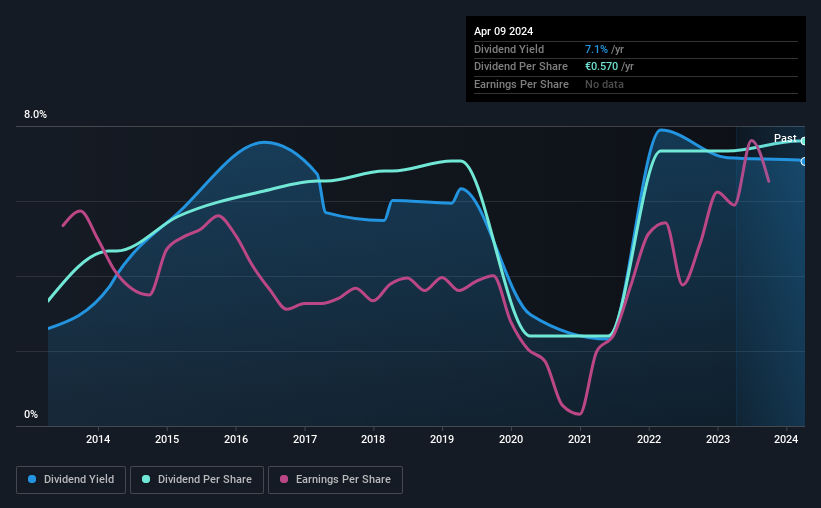

The board of UNIQA Insurance Group AG (VIE:UQA) has announced that it will be paying its dividend of €0.57 on the 17th of June, an increased payment from last year's comparable dividend. This will take the dividend yield to an attractive 7.1%, providing a nice boost to shareholder returns.

Check out our latest analysis for UNIQA Insurance Group

UNIQA Insurance Group's Earnings Easily Cover The Distributions

If the payments aren't sustainable, a high yield for a few years won't matter that much. However, UNIQA Insurance Group's earnings easily cover the dividend. As a result, a large proportion of what it earned was being reinvested back into the business.

If the trend of the last few years continues, EPS will grow by 11.9% over the next 12 months. If the dividend continues on this path, the payout ratio could be 37% by next year, which we think can be pretty sustainable going forward.

Dividend Volatility

While the company has been paying a dividend for a long time, it has cut the dividend at least once in the last 10 years. The annual payment during the last 10 years was €0.25 in 2014, and the most recent fiscal year payment was €0.57. This means that it has been growing its distributions at 8.6% per annum over that time. A reasonable rate of dividend growth is good to see, but we're wary that the dividend history is not as solid as we'd like, having been cut at least once.

The Dividend Looks Likely To Grow

Growing earnings per share could be a mitigating factor when considering the past fluctuations in the dividend. UNIQA Insurance Group has seen EPS rising for the last five years, at 12% per annum. A low payout ratio and decent growth suggests that the company is reinvesting well, and it also has plenty of room to increase the dividend over time.

UNIQA Insurance Group Looks Like A Great Dividend Stock

Overall, a dividend increase is always good, and we think that UNIQA Insurance Group is a strong income stock thanks to its track record and growing earnings. Distributions are quite easily covered by earnings, which are also being converted to cash flows. Taking this all into consideration, this looks like it could be a good dividend opportunity.

Companies possessing a stable dividend policy will likely enjoy greater investor interest than those suffering from a more inconsistent approach. However, there are other things to consider for investors when analysing stock performance. Taking the debate a bit further, we've identified 1 warning sign for UNIQA Insurance Group that investors need to be conscious of moving forward. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About WBAG:UQA

UNIQA Insurance Group

Operates as an insurance company in Austria and Central and Eastern Europe.

Established dividend payer and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor