Advertisement

- Japan

- /

- Electronic Equipment and Components

- /

- TSE:3156

Restar And 2 Other Undiscovered Gems With Promising Potential

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a period of cautious sentiment driven by the Federal Reserve's recent rate cut and ongoing political uncertainties, smaller-cap indexes have faced particular challenges. Despite these headwinds, the resilience of certain economic indicators, such as robust retail sales and job data in the U.S., suggests potential opportunities for discerning investors. In this environment, identifying stocks with solid fundamentals and growth potential becomes crucial—especially those that remain under the radar but are poised to benefit from improving economic conditions.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Canal Shipping Agencies | NA | 8.92% | 22.01% | ★★★★★★ |

| Suez Canal Company for Technology Settling (S.A.E) | NA | 22.31% | 13.60% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Parker Drilling | 46.05% | 0.86% | 52.25% | ★★★★★★ |

| Standard Bank | 0.13% | 27.78% | 30.36% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Invest Bank | 135.69% | 11.07% | 18.67% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Castellana Properties Socimi | 53.49% | 6.65% | 21.96% | ★★★★☆☆ |

| DIRTT Environmental Solutions | 58.73% | -5.34% | -5.43% | ★★★★☆☆ |

Below we spotlight a couple of our favorites from our exclusive screener.

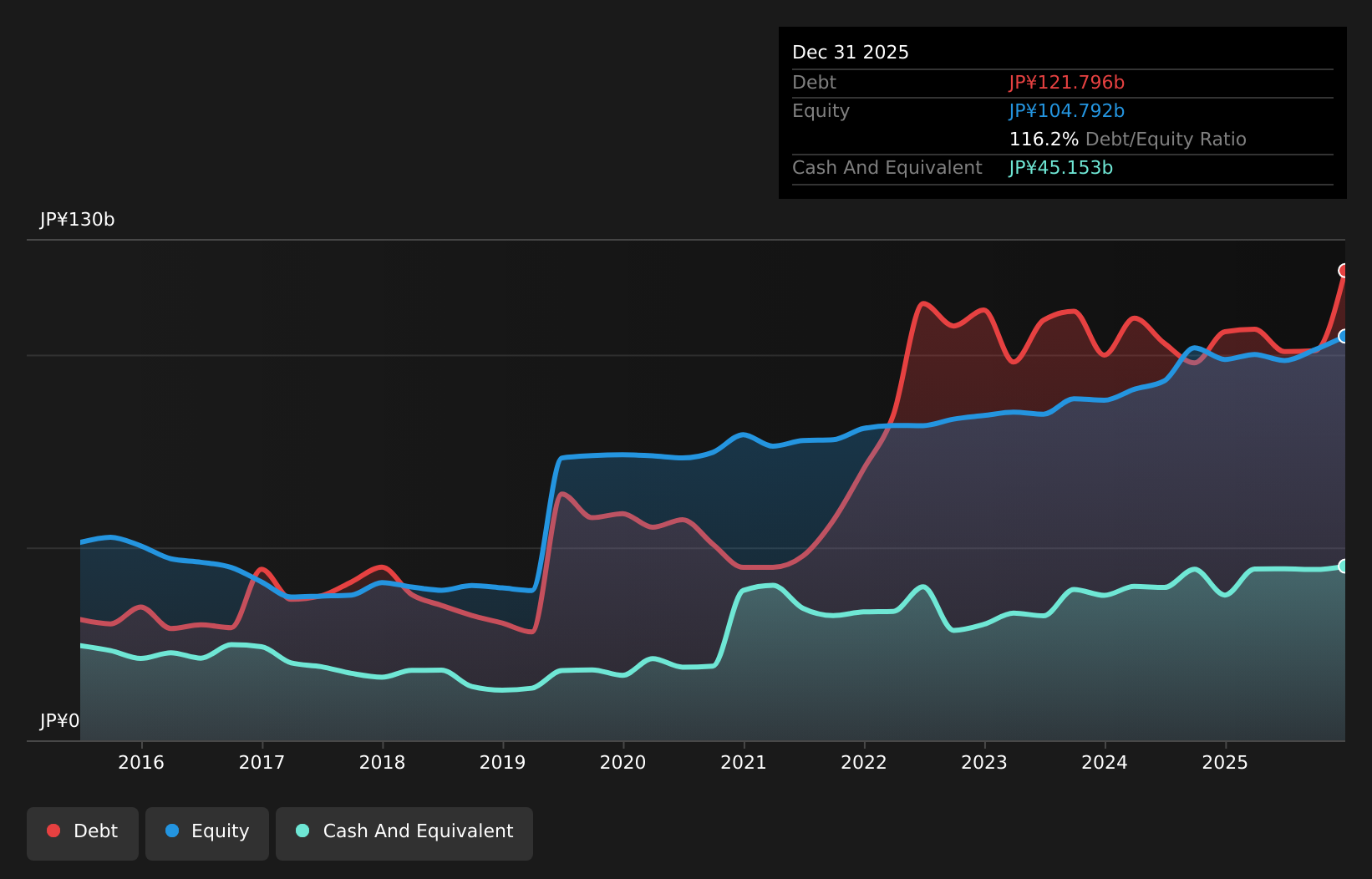

Restar (TSE:3156)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Restar Corporation operates in the electronics trading sector both within Japan and globally, with a market capitalization of approximately ¥76.79 billion.

Operations: Restar Corporation generates revenue through its electronics trading business in Japan and internationally. The company has a market capitalization of approximately ¥76.79 billion.

Restar, a nimble player in its field, has been making waves with a notable earnings growth of 37.9% over the past year, outpacing the broader electronic industry's -2.2%. The company recently executed a share buyback program repurchasing 8.31% of its shares for ¥6.91 billion, aiming to boost shareholder returns and capital efficiency. Despite facing a significant one-off loss of ¥4.3 billion impacting recent financials, Restar's price-to-earnings ratio stands at an attractive 9.6x compared to Japan’s market average of 13.4x, suggesting potential value for investors eyeing this dynamic entity.

- Unlock comprehensive insights into our analysis of Restar stock in this health report.

Gain insights into Restar's past trends and performance with our Past report.

Mars Group Holdings (TSE:6419)

Simply Wall St Value Rating: ★★★★★★

Overview: Mars Group Holdings Corporation, with a market cap of ¥60.42 billion, operates in Japan through its subsidiaries in the amusement, automatic recognition system, and hotel and restaurant sectors.

Operations: Mars Group Holdings generates revenue primarily from its amusement segment, which accounts for ¥37.59 billion, followed by the smart solution related business at ¥5.34 billion and the hotel/restaurant sector contributing ¥2.48 billion.

Mars Group Holdings, a relatively small player in its sector, has been debt-free for the past five years and boasts high-quality earnings. Over the last year, its earnings surged by 40.1%, significantly outpacing the Leisure industry's modest growth of 0.5%. Trading at nearly 83% below estimated fair value suggests potential undervaluation. Recent guidance indicates expected net sales of ¥41,800 million and an operating profit of ¥12,200 million for fiscal year ending March 2025. The company doubled its dividend to ¥120 per share from last year's ¥60 per share, reflecting confidence in financial health and future prospects.

- Dive into the specifics of Mars Group Holdings here with our thorough health report.

Assess Mars Group Holdings' past performance with our detailed historical performance reports.

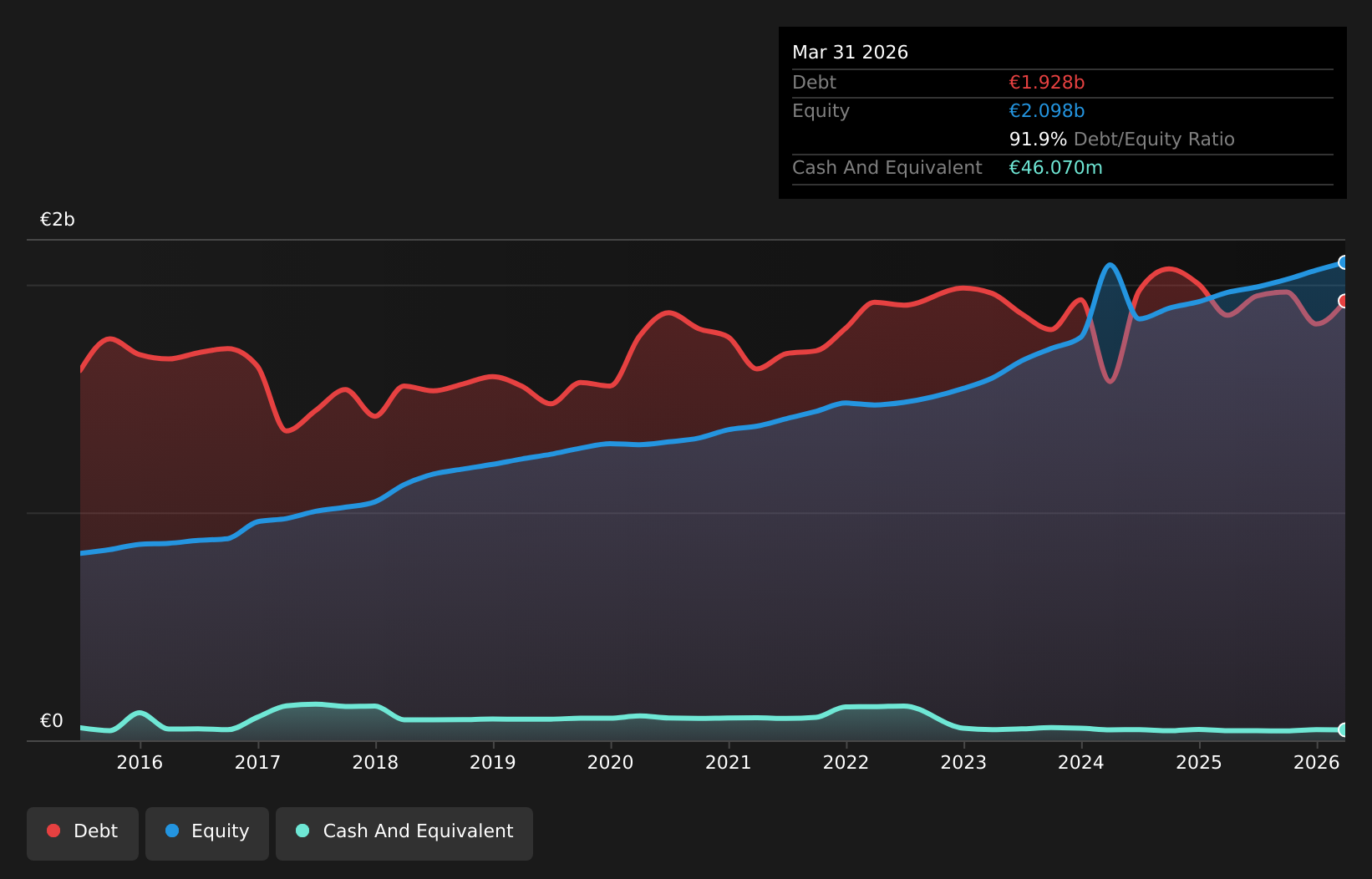

BKS Bank (WBAG:BKS)

Simply Wall St Value Rating: ★★★★☆☆

Overview: BKS Bank AG, along with its subsidiaries, offers a range of banking products and services and has a market capitalization of approximately €678.74 million.

Operations: BKS Bank generates revenue primarily from its Corporate Customers segment (€167.67 million), followed by Private Customers (€114.13 million) and Financial Markets (€89.67 million).

BKS Bank, with its total assets of €10.8 billion and equity of €1.9 billion, is a financial player worth noting for its high earnings growth of 23.7% over the past year, outpacing the industry average of 13.9%. Despite having a low allowance for bad loans at 56%, it faces challenges with non-performing loans at 3.4%. The bank's funding structure is primarily low-risk, with customer deposits making up 75% of liabilities. Trading significantly below its estimated fair value by nearly 59%, BKS offers potential upside but requires careful consideration due to these mixed indicators in its financial health.

- Navigate through the intricacies of BKS Bank with our comprehensive health report here.

Review our historical performance report to gain insights into BKS Bank's's past performance.

Taking Advantage

- Get an in-depth perspective on all 4624 Undiscovered Gems With Strong Fundamentals by using our screener here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:3156

Restar

Engages in electronics trading business in Japan and internationally.

Established dividend payer with proven track record.

Market Insights

Advertisement

Community Narratives

RIO is poised to weather a depressed iron ore environment, but commodity diversification comes with lower margins

Fair Value AU$110.51|4.1% overvalued

DU

Community Contributor

The demand for personalized medicine will keep Thermo Fisher Scientific thriving

Fair Value US$540.27|21.5% undervalued

UN

Community Contributor

Silver Play by A Family with 10x Potential

Fair Value UK£24.00|88.8% undervalued

RO

Community Contributor