Advertisement

- United Kingdom

- /

- Specialty Stores

- /

- LSE:ASC

Should You Worry About ASOS Plc’s (LON:ASC) ROCE?

Today we are going to look at ASOS Plc (LON:ASC) to see whether it might be an attractive investment prospect. In particular, we'll consider its Return On Capital Employed (ROCE), as that can give us insight into how profitably the company is able to employ capital in its business.

First, we'll go over how we calculate ROCE. Next, we'll compare it to others in its industry. Then we'll determine how its current liabilities are affecting its ROCE.

What is Return On Capital Employed (ROCE)?

ROCE measures the amount of pre-tax profits a company can generate from the capital employed in its business. In general, businesses with a higher ROCE are usually better quality. Overall, it is a valuable metric that has its flaws. Author Edwin Whiting says to be careful when comparing the ROCE of different businesses, since 'No two businesses are exactly alike.

How Do You Calculate Return On Capital Employed?

Analysts use this formula to calculate return on capital employed:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

Or for ASOS:

0.074 = UK£35m ÷ (UK£1.2b - UK£772m) (Based on the trailing twelve months to August 2019.)

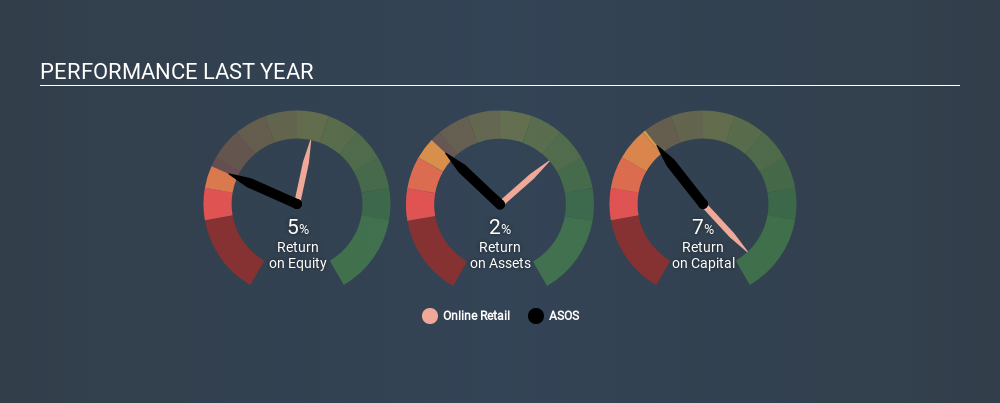

So, ASOS has an ROCE of 7.4%.

See our latest analysis for ASOS

Does ASOS Have A Good ROCE?

When making comparisons between similar businesses, investors may find ROCE useful. In this analysis, ASOS's ROCE appears meaningfully below the 12% average reported by the Online Retail industry. This could be seen as a negative, as it suggests some competitors may be employing their capital more efficiently. Setting aside the industry comparison for now, ASOS's ROCE is mediocre in absolute terms, considering the risk of investing in stocks versus the safety of a bank account. Readers may find more attractive investment prospects elsewhere.

ASOS's current ROCE of 7.4% is lower than its ROCE in the past, which was 28%, 3 years ago. So investors might consider if it has had issues recently. You can click on the image below to see (in greater detail) how ASOS's past growth compares to other companies.

When considering this metric, keep in mind that it is backwards looking, and not necessarily predictive. ROCE can be misleading for companies in cyclical industries, with returns looking impressive during the boom times, but very weak during the busts. ROCE is only a point-in-time measure. What happens in the future is pretty important for investors, so we have prepared a free report on analyst forecasts for ASOS.

How ASOS's Current Liabilities Impact Its ROCE

Current liabilities are short term bills and invoices that need to be paid in 12 months or less. The ROCE equation subtracts current liabilities from capital employed, so a company with a lot of current liabilities appears to have less capital employed, and a higher ROCE than otherwise. To counter this, investors can check if a company has high current liabilities relative to total assets.

ASOS has total liabilities of UK£772m and total assets of UK£1.2b. Therefore its current liabilities are equivalent to approximately 62% of its total assets. With a high level of current liabilities, ASOS will experience a boost to its ROCE.

The Bottom Line On ASOS's ROCE

Even so, the company reports a mediocre ROCE, and there may be better investments out there. But note: make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a P/E ratio below 20).

If you like to buy stocks alongside management, then you might just love this free list of companies. (Hint: insiders have been buying them).

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About LSE:ASC

ASOS

Operates as an online fashion retailer in the United Kingdom, the European Union, the United States, and internationally.

Fair value with imperfect balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2533.3% undervalued

153 followersusers have followed this narrative

0 commentsusers have commented on this narrative

26 likesusers have liked this narrative

HA

HarishPK on Amdocs ·

Why Amdocs is a high conviction Buy for me?

Fair Value:US$82.0328.6% undervalued

33 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

IV

Ivoed on SBM Offshore ·

Why SBM Offshore’s €30 Share Price May Be Too Harsh On Its Backlog

Fair Value:€44.527.2% undervalued

16 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

CL

Clive_Thompson on Green Tea Group ·

One of China's Fastest-Growing Restaurant Chains Trades on Just 7x Earnings and an 8% Dividend

Fair Value:HK$8.723.9% undervalued

46 followersusers have followed this narrative

3 commentsusers have commented on this narrative

20 likesusers have liked this narrative

Recently Updated Narratives

BL

Blaxland on Lincoln Minerals ·

Asymmetric potential

Fair Value:AU$0.002250.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

John_Eric on Workday ·

Workday's Backlog Just Grew Faster Than Its Revenue.The Market Shrugged.

Fair Value:US$550.167.3% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

John_Eric on SPX Technologies ·

I Fell in Love With a Data-Center Cooling Stock. Then I Opened the Filings.

Fair Value:US$2036.2% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28020.0% undervalued

271 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9119.1% overvalued

136 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

KI

KiwiInvest on Amazon.com ·

Amazon's high growth, high tech segments propel its profits, while traditional segments plod along

Fair Value:US$475.0942.2% undervalued

163 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

Trending Discussion

YA

Yash_Upadhyaya on Reddit ·

Steve blamed "choppy" Google referral traffic for the miss on US daily active user (DAU) WHILST being in a standoff with Google on the AI licensing deal... hmm 🤔 One way or another a deal is happening. What's gonna be interesting is to see how good or bad (which the market is pricing in) would it be. PS - I don't own the stock but like the company.

1

|0