The beginning of 2026 was all about Gold. The yellow metal jumped from $4,300/oz at the start of January to $5,400/oz by the end of it - an increase of 26% in less than a month.

Many analysts thought the rally could see it hit $6,000/oz soon, especially after the Iran conflict started in February.

But gold had other plans.

Since the war began, it instead began its descent… down to today’s price of around $4,600/oz.

So what gives? Isn’t gold meant to be the safe haven investors turn to in times of volatility?

The story is more nuanced than you might first think. As you read this article, you’ll start to see why the descent actually makes sense… and why it’s unlikely to last very long.

What happened in the markets this week?

🛢️ Saudi Aramco’s profit surge highlights how infrastructure constraints can boost cash flow - Reuters

- What happened: Saudi Aramco reported a 26% increase in Q1 profit as a key pipeline reached capacity. The milestone helped the company move more crude efficiently and supported stronger earnings.

- How it impacts investors: Energy returns are still heavily influenced by infrastructure and operational bottlenecks, not just oil prices. On that note, Aramco investors will be celebrating a quarterly dividend 3.6% higher than last year’s.

- Next steps: Review Saudi Aramco’s company report to see how its dividend payments have changed over time. Or explore other global energy stocks and dividend opportunities.

🤖 Anthropic lands a US$1.8 billion cloud deal with Akamai Technologies - Reuters

- What happened: Anthropic signed a US$1.8 billion computing deal with Akamai Technologies to power growing demand for its AI models. Akamai’s stock jumped after the company revealed it had secured a long-term agreement with a major AI customer.

- How it impacts investors: The AI boom is creating opportunities well beyond the usual cloud giants. Companies with the right infrastructure are finding themselves in exactly the right place at the right time.

- Next steps: Explore our high growth tech & AI investing ideas to find companies building the backbone of AI. Also review whether this deal could be a new growth catalyst for Akamai Technologies, using its company report.

🍎 Apple and Intel may team up again in a surprise chip deal ( Reuters )

- What happened : Apple and Intel have reached a preliminary agreement for Intel to manufacture some chips for Apple. The deal would reunite the two companies after Apple previously moved its Macs to in-house chips.

- How it impacts investors : This could be a big credibility boost for Intel’s turnaround. When one of the world’s toughest customers comes knocking, the market tends to pay attention.

- Next steps: Intel has seen a rough few years as it struggled to compete with fellow chipmakers. Check out Intel’s company report to gauge whether this new deal could materially change Intel’s trajectory.

🚀 AMD jumped 19% after Q1 earnings, saying AI demand is bigger than expected - CNBC

- What happened : Advanced Micro Devices more than doubled its long-term forecast for the server CPU market, now expecting it to top US$120 billion by 2030. Revenue rose 38% year over year, and the stock jumped 19% after earnings.

- How it impacts investors: AI isn’t just a GPU story anymore. That opens the door for more chipmakers to benefit as companies race to build smarter systems.

- Next steps: Explore our semiconductor and AI investing ideas .

☁️ Cloudflare’s AI pivot comes with a painful workforce reset - CNBC

- What happened: Cloudflare fell 24% despite beating Q1 earnings estimates. The company announced it will cut more than 1,100 employees or over 20% of its workforce. CEO Matthew Prince said agentic AI has fundamentally changed how the company operates.

- How it impacts investors : AI may boost productivity, but it can also reshape cost structures and staffing needs overnight. Investors should watch which software companies turn automation into margin expansion rather than disruption.

- Next steps : Use our software screener to find companies improving profitability .

The story of the gold price roller coaster

Before we get into why gold prices are down, let’s first recall why it went up.

Like all commodities, gold ’s price reacts to the key economic forces: supply and demand.

Markets saw a massive shift in demand for the precious metal after a key geopolitical event - the Russia-Ukraine war in February 2022.

Remember how both the U.S. and Europe responded by blocking Russia’s access to its foreign currency reserves (the majority of which were the USD and Euro), worth between $300-$330 billion dollars?

That event became the catalyst to governments all over the world. Russia became an example of what could happen when a country relies too heavily on another country’s medium of exchange.

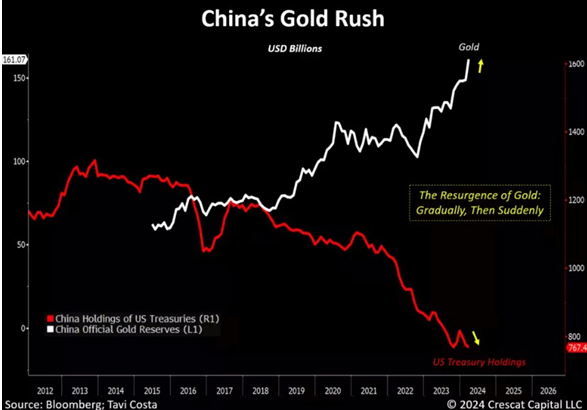

Beginning Q3 2022, multiple central banks including Russia, China, Turkey, India, and Poland began buying up more gold than they ever had since post-GFC.

China, seemingly at constant odds with the U.S. (we’ll see how this week’s Trump-Xi meeting goes), is a good example of a government that’s shifted away from the USD.

Estimates show central banks added over 1,000 metric tons (35.3m oz) per year in the last three years.

By the end of 2025, central banks held ~20% of all mined gold in the world. It was the first time in 20 years that central banks (excl. U.S.) held more gold than U.S. treasuries in their reserves.

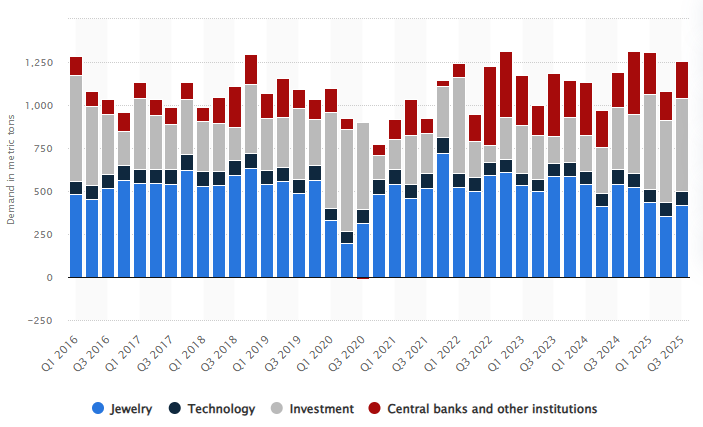

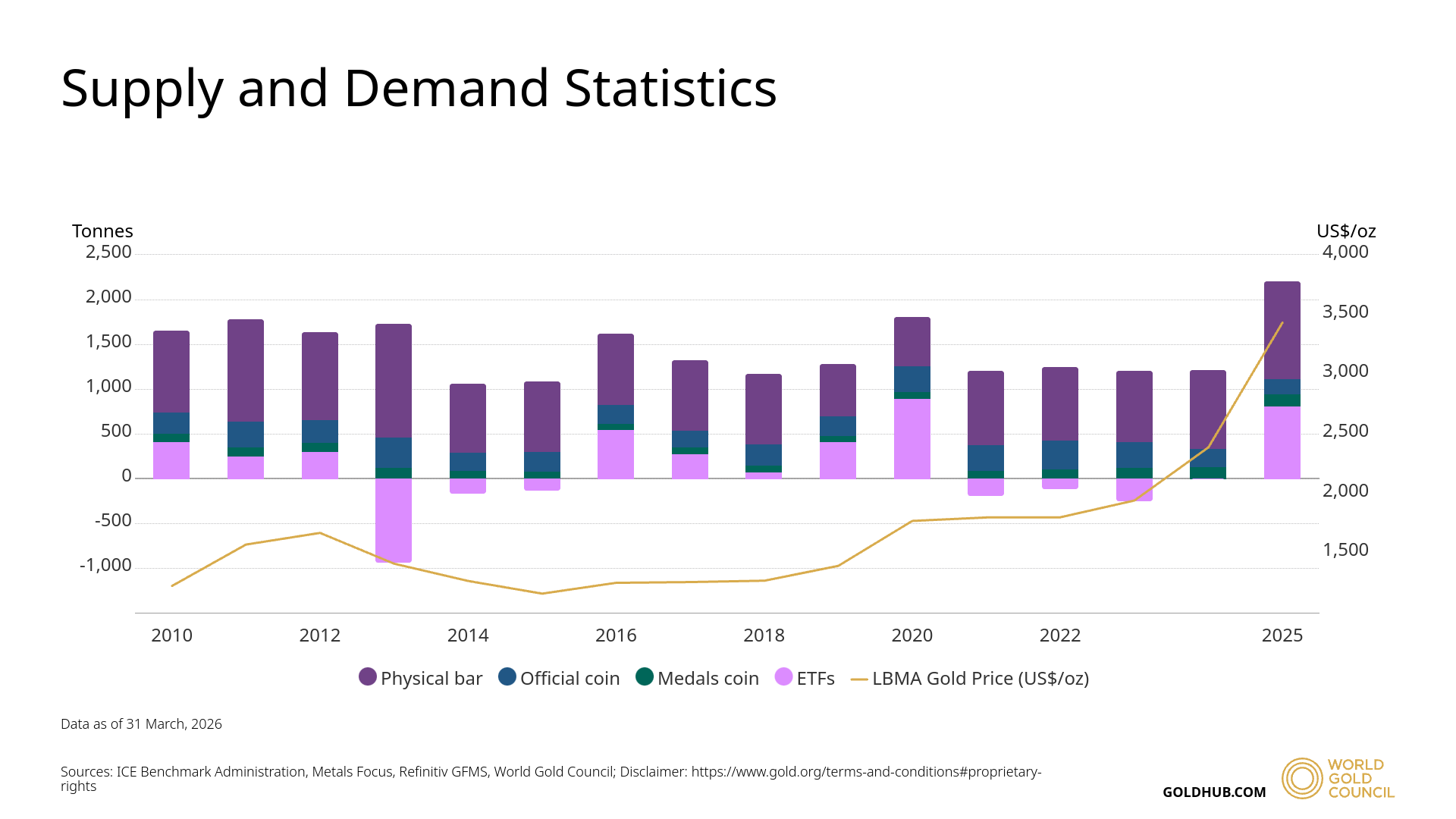

Similarly, retail and institutional investors surged as gold prices rallied. Global investment demand totalled 2,175 tons last year, its highest in history. This provided a further tailwind for gold’s jump earlier this year.

So why did gold prices drop in 2026?

The decline began in late-March, a month after the Iran conflict began.

We previously discussed how the economic landscape had begun to change as the closure of the Strait of Hormuz entered its third month.

Everything explained in that article matters. Fuel, gas, fertilizer and food price inflation is now back at multi-year highs for many countries, and governments are beginning to subsidize consumers with lower fuel excise taxes, cost-of-living subsidies, etc.

That means it’s likely that governments are drawing upon reserves to sustain the economy - and it’s also likely that gold’s higher-than-average price makes it an enticing commodity to swap or liquidate for funds.

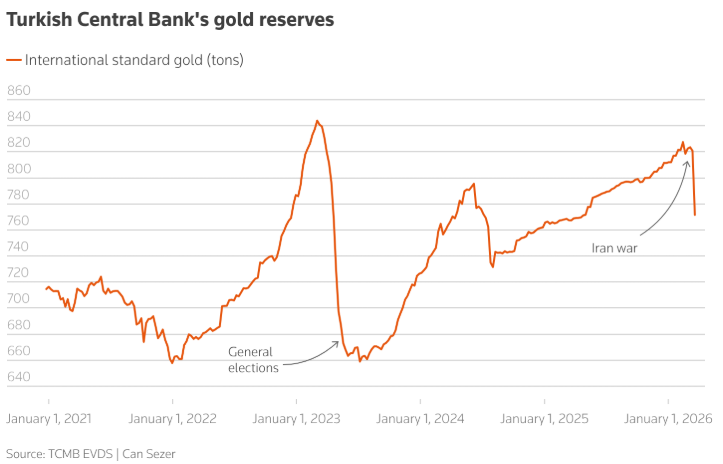

A good example is the Turkish Government, which sold over 127 tons of gold since the Iran conflict began - its largest and fastest sell-off in history - to support higher import costs and the falling Lira.

The same can be said for the individual and institutional investors who hold gold; with other positions likely in the red, the liquidity and return gold provides makes it an easy choice to offload.

In a sense, gold is indeed acting as a hedge against volatility - but this time as an asset in the balance sheet rather than a hedging instrument.

👉 Explore junior gold miners with strong balance sheets that may be better equipped to navigate economic uncertainty, while offering upside if their potential isn’t yet fully reflected in their market value.

The long-term outlook for gold: will it hit $6,000/oz this year?

Earlier in the year, the general consensus among the big banks was for gold to surge to at least $6,000/oz, with estimates ranging between $5,400 to $6,300.

Many of these analysts have since revised their expectations, at least while the Strait of Hormuz remains closed:

- Goldman Sachs sees gold hitting $5,400 by year-end.

- UBS believes it could still reach as high as $5,600 .

- Morgan Stanley revised its target from $5,700 to $5,200 .

So even though gold is currently sitting at around ~$4,700 amidst the conflict, today’s revised estimates still see gold bouncing back within the year.

Commentary across the board echoes the structural trends around gold.

1. Central banks’ buying momentum is expected to rise as de-dollarization continues

While some governments have hit the pause (or even rewind) button on gold investment, many continue or plan to resume buying activity after the geopolitical climate stabilizes.

The World Gold Council estimates central bank buying to still total 700 to 900 tons this year. A survey conducted among central banks also showed that an overwhelming 95% of them believed their own gold reserves would increase in the next 12 months.

Deutsche Bank recently published a research note stating it expected gold to hit $8,000 by 2031 due to mass de-dollarization.

Wells Fargo is even more bullish , thinking gold could hit $8,000 by next year.

2. Gold prices will be pushed upward due to the Global Sovereign Debt crisis

The U.S., UK and Japan have debt-to-GDP ratios of 123%, 101% and 240%, respectively. This matters because high levels of debt mean more interest, which could mean higher chances of default.

While these entities defaulting on debt will bring about a much larger problem, these ratios have incentivized governments, institutions, and investors alike to invest in assets outside the fiat monetary system to hedge against default risk. One of such assets is gold.

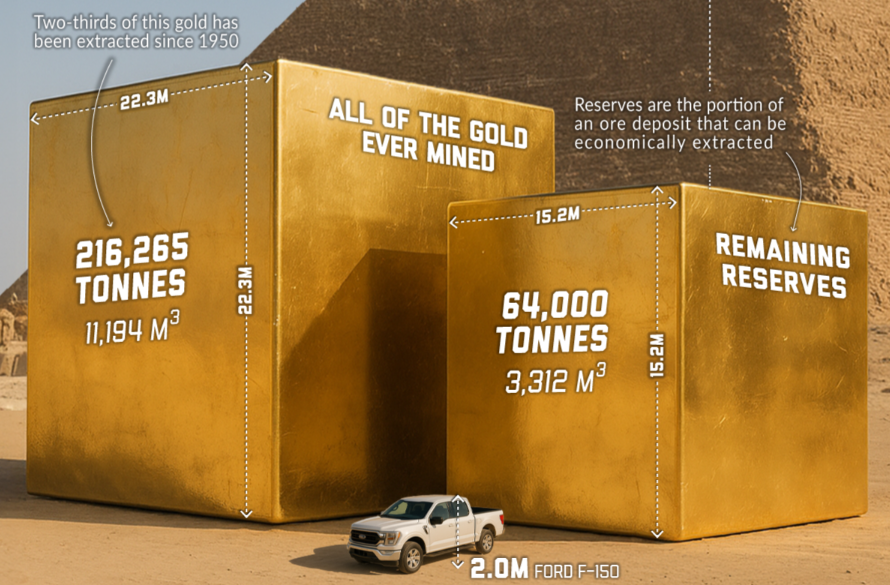

3. Gold supply is finite and we’re running out

Nearly 75% of the world’s gold reserves have been mined. Around two-thirds of that were mined in just the last 70 years.

A new record of 3,672 tons of gold was mined last year. Using that as a basis, you can calculate that all economically recoverable gold will be extracted in the next 15-20 years.

With central banks and investors stockpiling gold - scarcity could be another factor pushing gold prices up in the next few years.

💡 To be fair, there’s around 132,110 tons more of verified gold resources … they’re just not economically viable to mine. This can change in the future as gold prices and mining technology evolve.

4. Gold has an extremely large moat

There have long been talks of Bitcoin being “digital gold” , but it’s been 17 years since Bitcoin was invented and economic activity around it has still been highly volatile and far from close to gold’s.

Additionally, Bitcoin may be able to replicate gold’s decentralized nature, high liquidity, and limited supply, but there’s one glaring difference that can never be changed: gold is a physical asset, Bitcoin is not.

Speaking of physical assets - yes, platinum and silver are also precious metals, and in fact, platinum is 30 times rarer than gold.

But gold has an extremely large moat. It has thousands of years of history of being used as the financial asset and the precious metal, and it’ll be extremely hard to change that viewpoint for an entire world.

Additionally, gold having relatively limited industrial use means supply and demand is generally all about it being an inflation hedge, balance sheet asset and safe haven.

Platinum and silver both have industrial uses that can impact their economics, making them a less viable option for investors and central banks looking for gold’s specific use case.

👉 Looking for gold more stocks to explore? Check out our list of “elite” gold miners with strong balance sheets and low production costs.

💡 The Insight: Gold’s pullback may be setting up the next leg higher

Gold’s recent decline may raise concerns but doesn’t necessarily change the long term investment case. The recent sell-off appears to be driven more by short term liquidity needs than by a deterioration in fundamentals.

Throughout history, gold has tended to perform best when confidence in traditional financial systems begins to weaken.

Today, several structural forces continue to support that trend: central banks are reducing their reliance on the USD, sovereign debt levels are climbing, and economically recoverable gold reserves are becoming scarce.

Rather than viewing gold’s volatility as a sign the story is over, investors may want to see it as a reminder that some of the strongest long-term opportunities are found when a structural trend temporarily moves in reverse.

Key events next week

Monday

- 🇨🇳 Industrial Production (YoY)

- Forecast : 5.5%, Previous : 5.7%

- Why it matters : A key gauge of factory activity and global demand. Slower growth could signal weaker momentum across China’s manufacturing and export sectors.

Tuesday

- 🇨🇦 Inflation Rate (YoY)

- Forecast : 3.0%, Previous : 2.4%

- Why it matters : A rebound in inflation could reduce the chances of further rate cuts and keep borrowing costs elevated for longer.

Wednesday

- 🇬🇧 Inflation Rate (YoY)

- Forecast : 2.6%, Previous : 3.3%

- Why it matters : A softer reading would support expectations for rate cuts, while persistent inflation could keep the Bank of England cautious.

Thursday

- 🇺🇸 FOMC Minutes

- Why it matters : Investors will look for clues on how concerned policymakers remain about inflation and when the next rate cut could occur.

Friday

- 🇯🇵 Inflation Rate (YoY)

- Forecast: 1.8% , Previous: 1.5%

- Why it matters: Rising inflation would strengthen the case for further policy normalisation and could have a meaningful impact on the yen and global bond markets.

The user stuart_roberts holds no position in CNSX:UG. Simply Wall St has no position in any of the companies mentioned.

Featured narratives may be promoted for a fee. These narratives are general in nature and reflect the authors’ own opinions only. They do not represent the views of Simply Wall St and do not constitute a recommendation to buy or sell any stock. Any scenarios or fair value estimates discussed are exploratory only, are not indicative of the company’s future performance, and do not take into account your objectives or financial situation. The authors’ analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Stella and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Stella Ong

Stella Ong is an Equity Analyst with over 10 years of experience investing in international markets. She has worked across multiple brokers, delivering equity research, market analysis, and financial commentary, and currently hosts Simply Wall St’s Market Insights and Weekly Picks podcasts.