Most of the large caps, including Nvidia, have now reported Q1 earnings. This week we are doing a recap of the key trends affecting earnings reports, including the AI trade which continues to dominate the narrative.

We are also taking a closer look at the software sector which is ‘ground zero’ for AI disruption, and the disconnect between sentiment and Q1 income statements.

What Happened In Markets This Week

Here’s a quick summary of what’s been going on:

🛢️ Rising bond yields and oil prices put pressure on rate-sensitive sectors ( CNBC )

- What happened: US Treasury yields continued to rise as the oil price crossed $100 once again. The 30-year Treasury yield reached 5.2%, its highest level since 2007, while bond yields in Germany, Japan, and the UK also hit multi-year highs. US 30-year yields are reflecting two problems: inflation in the immediate future and the long term outlook for US debt.

- How it impacts investors: Higher yields are tightening financial conditions and putting fresh pressure on rate-sensitive sectors and growth stocks. The market is grappling with higher energy costs and a “higher for longer” interest rate outlook.

- Next steps: Explore rate-sensitive sectors and inflation-resilient opportunities with Simply Wall St’s Discover tool .

🚀 SpaceX’s blockbuster IPO will further concentrate markets ( Reuters )

- What happened: SpaceX filed for its long anticipated IPO that could raise up to US$75 billion at a valuation approaching US$2 trillion. Investors were surprised by the size of the company’s losses in 2025 and 2026. Starlink is profitable, but not profitable enough to cover spending across the rest of the business, including xAI. Neither rockets nor data centers are cheap! The IPO also revealed that Musk will retain 85.1% of voting power.

- How it impacts investors: This could become a pivotal moment for public markets, with index fund demand pulling even more capital toward mega-cap technology and growth. The filing also highlights the power of retail investors who are likely to be a large part of the shareholder base.

- Next steps: SpaceX is the biggest space company, but not the only one. For other options check out the U.S. Aerospace And Defense watchlist .

🎵 Spotify’s AI remix push opens a new revenue lane for streaming ( The Guardian )

- What happened: Spotify signed a deal with Universal Music Group allowing Premium subscribers to create AI-generated remixes and covers using licensed music from participating artists. The feature will launch as a paid add-on with revenue shared between Spotify, artists, and songwriters.

- How it impacts investors: This is the type of innovation that can give streaming platforms (and others) new revenue opportunities. It also strengthens the competitive advantage for companies like Spotify with massive catalogs. Major labels like Universal also gain a new royalty stream from user-generated AI content.

- Next steps: Use the Spotify Technology company report to see how new products could influence long-term growth and the Spotify community page to see what other users have to say about the company.

🪓 Intuit plunges 20% on AI overhaul and TurboTax revenue miss ( Yahoo Finance )

- What happened: Intuit shares fell 20% after the company announced plans to cut around 3,000 jobs, or roughly 17% of its workforce, to fund a broader AI transformation strategy. Quarterly revenue and earnings beat expectations, but investors focused on restructuring costs and a small revenue miss from the TurboTax segment. The market appears ready to sell software stocks on any sign of weakness.

- How it impacts investors: Investors are reassessing legacy software companies facing potential AI disruption, even when current financial results are solid and the company is embracing AI. Without aggressive investment in AI, SaaS companies are very likely to be disrupted, but this will mean lower profits in the short term.

- Next steps : Check the narratives on the Intuit community page to make sure you are aware of potential positive and negative catalysts driving future earnings growth. Use the company report for any software company to see how much they are investing to remain relevant in an AI future.

Q1 Earnings Season: 2026 off to a Flying Start?

Over 90% of S&P 500 companies have now reported earnings for the first quarter, and by most measures it was the best quarter in years.

By the end of April, with Alphabet and the other big tech companies out of the way, it was already clear that year-on-year earnings growth for the quarter was going to be above 27%, the highest since Q4 2021 . The earnings beat rate and margin are both well above average.

Taking a closer look, 10 of the 11 sectors have reported positive earnings growth. The healthcare sector has reported a 3.2% decline in earnings, though this was a lot better than the 8.5% drop expected in March.

While most sectors have reported growth, the concentration amongst the index heavyweights was as apparent as ever. Most of the aggregate earnings growth (i.e. total dollars earned) can be attributed to the IT and Communications sectors, and in particular to Alphabet, Amazon and Meta .

The two topics that dominated earnings calls were unsurprisingly the war in the Strait of Hormuz and AI .

The war, and the rising oil price, only really affected the second half of Q1. But, the impact of inflation still shows up at the sector level, which is a continuation of the trend we’ve seen over the last few quarters.

Most of the companies reporting lower margins are in interest rate and inflation sensitive sectors: consumer discretionary , consumer staples and real estate .

The winners (for earnings growth and margins) were the tech , communications , and financial sectors. Within the financial sector banks in particular have benefited from higher than expected yields, M&A activity and market volatility.

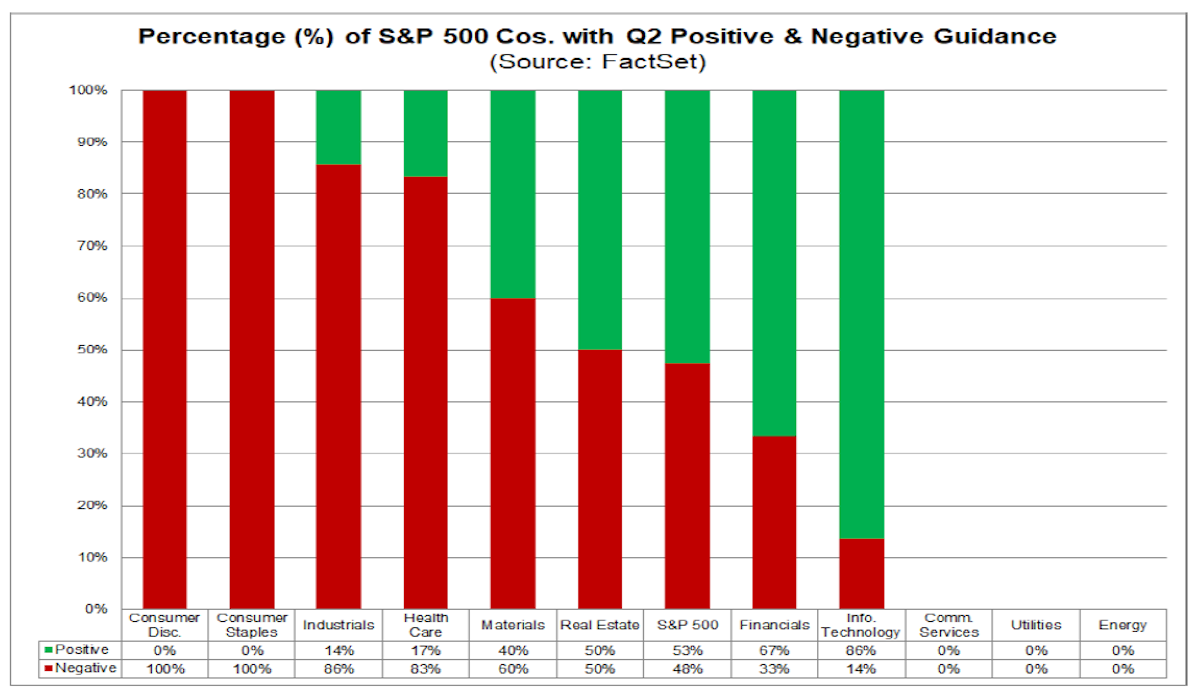

A similar pattern emerged with companies issuing Q2 guidance. Among the consumer companies issuing Q2 guidance, 100% lowered their guidance. Guidance from companies in the industrials and healthcare sectors was also negative in most cases.

Looking ahead, analysts still expect earnings growth to be up year-on-year for the remaining quarters in 2026, but they are pointing to a deceleration.

AI and the SaaSpocalypse

Over the last few years the hyperscapers have been committing ever-growing piles of cash to AI infrastructure. Investors have been asking if or when these investments will generate a return.

Google Cloud had a decent answer in Q1. Its backlog nearly doubled in a single quarter, from $240 billion to $462 billion , while operating margins nearly doubled too, from 17.8% to 32.9%. Results from Microsoft and Amazon reflected similar trends.

The catch is that while earnings are growing, free cash flows are collapsing. Amazon’s AWS unit has seen free cash flow fall from $25.9 to $1.2 billion in the last year , due to its capex.

NB: This implies a lot of depreciation to come in the future. Operating income will need to keep rising to offset the depreciation expense.

For the hyperscalers the constraint is now capacity rather than demand. Google Cloud’s token processing reached 16 billion tokens per minute , up 60% quarter-over-quarter, but still couldn’t keep up with demand.

Datacenters are currently facing a shortage in memory chips. As a result the leading chipmakers Samsung, SK hynix and Micron have added hundreds of billions to their market caps. Historically supply has always caught up with demand, so this isn’t expected to be a permanent constraint.

The software paradox

Earlier this year, Anthropic launched a series of plugins capable of performing complex workflows in the legal, accounting and finance domains. The market then dumped SaaS (software as a service) stocks, which were already under pressure.

The premise is that agentic AI systems are now capable of replacing these platforms at a fraction of the cost. The share prices of leading SaaS platforms like Adobe, Salesforce and Intuit are down 40 to 70% over the last year.

So far AI has had no impact on quarterly results for SaaS companies, particularly as far as competition goes. Most have managed to reduce their headcount to some extent, but also increased investment in AI. On balance, revenue and margins for most SaaS companies has continued along the same trajectory as before.

With share prices down, these stocks are now either looking ‘cheap,’ or they are value traps.

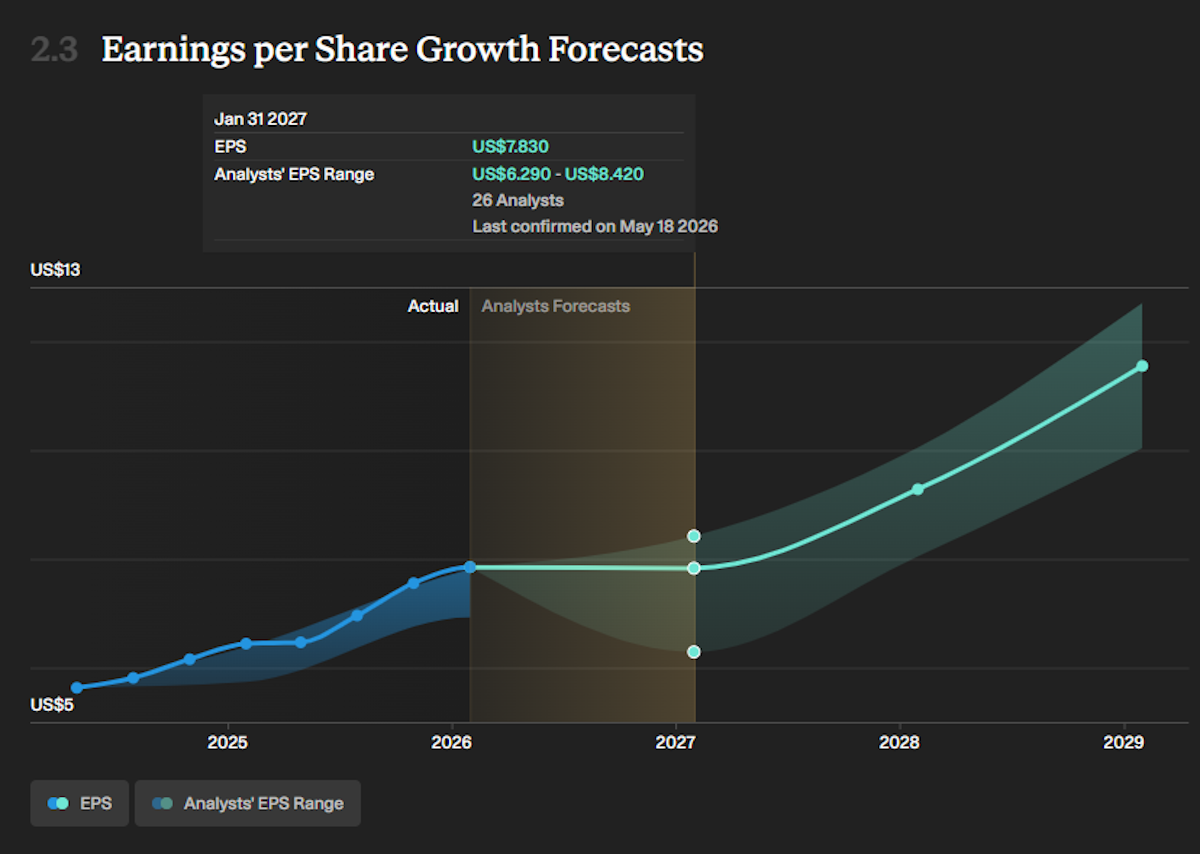

The reality is that some SaaS companies probably will be disrupted, while others will manage to position themselves within the AI eco-system. The uncertainty is reflected in analyst forecasts for Salesforce’s EPS:

Some software companies, including SaaS platforms, are already providing valuable tools for AI development and deployment. They provide software for observability, MLOps, data infrastructure, security and EDA (Electronic Design Automation). The key companies are included in the AI Enablers and Infrastructure Software watchlist.

Others that don’t completely match this profile now, are attempting to reposition themselves to do so. ServiceNow for example is positioning itself as the vendor-neutral orchestration layer for multi-vendor AI systems.

The big risk is faced by platforms with monthly subscription models which can be replaced by AI tools that charge based on usage rather than a fixed monthly subscription. For these companies, maintaining a moat might require them to take a pay cut.

💡 The Insight: Use the 7 Powers framework to assess a company’s moat

The current uncertainty around software stocks is probably creating opportunities, if you can figure out which software companies can adapt their moats for the AI world.

Hamilton Helmer’s book 7 Powers: “The Foundations of Business Strategy” looks at the way companies establish durable competitive advantages. The core premise is that true business power requires both a unique benefit and a barrier to imitation.

The 7 Powers form a useful framework to assess these companies as their strategy evolves:

1. Scale Economies The bigger you get, the cheaper it costs to serve each customer. This is where companies like Salesforce and Adobe still have a sizable advantage.

2. Network Economies More users make the product more valuable for everyone. As an example, AI coding tools improve as code suggestions are accepted or rejected. More users leads to more rapid improvement.

3. Counter-Positioning A new player adopts a business model that an incumbent literally cannot copy without destroying their own economics. This is where incumbents with subscription models are vulnerable, and will need to adapt.

4. Switching Costs Leaving is painful, so customers don't. Microsoft's near-perfect Azure renewal rates aren't an accident. Once enterprise workflows, security policies, and internal tools are wired into a cloud stack, migration costs are enormous. Copilot deepens this further: AI that learns a company's documents, tone, and processes becomes genuinely hard to rip out.

5. Branding Customers pay more (or choose you first) based on trust, not just specs. For sensitive tasks like accounting, a trusted brand might outweigh cost.

6. Cornered Resource You hold something critical that others can't access at any price. Proprietary training data is the AI version of this. A platform with a decade of human interaction data, or a medical network with clinical records, has a training input moat that can't be purchased.

7. Process Power Deep operational know-how that competitors can observe but can't replicate quickly. Google’s research and innovation culture is a good example.

Key Events Next Week

Monday

- 🇺🇸 US Memorial Day – Markets Closed

- ⏸️ Notes: US equity and bond markets are closed for Memorial Day. Expect lighter volumes across global markets.

Tuesday

- 🇺🇸 US CB Consumer Confidence (May)

- 📊 Forecast: 92, Previous 92.8

- ➡️ Why it matters: A further decline would confirm consumers are taking strain due to energy costs and inflation.

Wednesday

- 🇦🇺 Australia Inflation YoY (April)

- 📈 Forecast : 5.1%, Previous: 4.6%

- ➡️ Why it matters: Another hot print would end any hopes for near-term easing.

Thursday

- 🇺🇸 US GDP Q1 2026 (Second Estimate)

- 📊 Forecast: 2.0%, Previous 0.5%

- ➡️ Why it matters: The headline number would only confirm the original estimate, but economists will be looking at any revisions to the consumer spending or inventories components.

- 🇺🇸 US Initial Jobless Claims (w/e 23 May)

- 📉 Forecast: 215k, Previous: 209k

- ➡️ Why it matters: While claims remain near the bottom of the range, and inflation edges higher the Fed has little flexibility to cut.

Earnings season is winding down, but there are still some prominent tech names reporting this week:

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Richard Bowman and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Richard Bowman

Richard is an analyst, writer and investor based in Cape Town, South Africa. He has written for several online investment publications and continues to do so. Richard is fascinated by economics, financial markets and behavioral finance. He is also passionate about tools and content that make investing accessible to everyone.