- United States

- /

- Luxury

- /

- NYSE:NKE

NIKE, Inc. (NYSE:NKE) Passed Our Checks, And It's About To Pay A US$0.24 Dividend

Regular readers will know that we love our dividends at Simply Wall St, which is why it's exciting to see NIKE, Inc. (NYSE:NKE) is about to trade ex-dividend in the next 4 days. You can purchase shares before the 28th of February in order to receive the dividend, which the company will pay on the 1st of April.

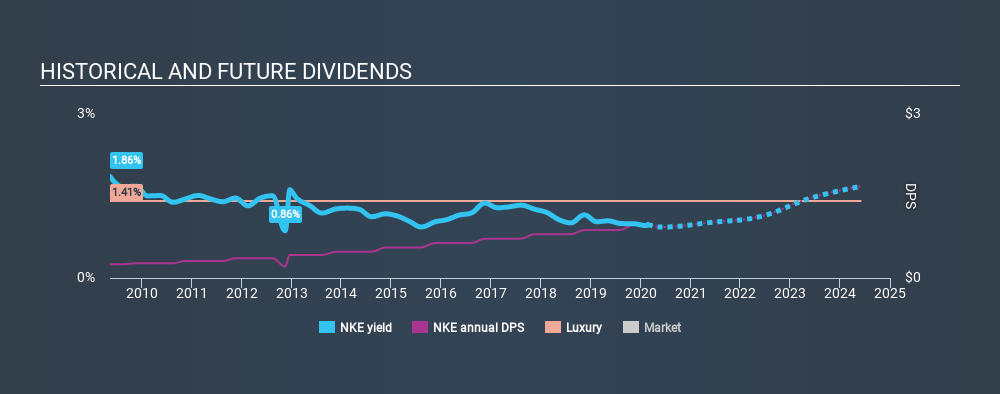

NIKE's next dividend payment will be US$0.24 per share, on the back of last year when the company paid a total of US$0.98 to shareholders. Calculating the last year's worth of payments shows that NIKE has a trailing yield of 1.0% on the current share price of $100.25. We love seeing companies pay a dividend, but it's also important to be sure that laying the golden eggs isn't going to kill our golden goose! We need to see whether the dividend is covered by earnings and if it's growing.

Check out our latest analysis for NIKE

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. That's why it's good to see NIKE paying out a modest 31% of its earnings. That said, even highly profitable companies sometimes might not generate enough cash to pay the dividend, which is why we should always check if the dividend is covered by cash flow. Thankfully its dividend payments took up just 41% of the free cash flow it generated, which is a comfortable payout ratio.

It's encouraging to see that the dividend is covered by both profit and cash flow. This generally suggests the dividend is sustainable, as long as earnings don't drop precipitously.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Companies with consistently growing earnings per share generally make the best dividend stocks, as they usually find it easier to grow dividends per share. Investors love dividends, so if earnings fall and the dividend is reduced, expect a stock to be sold off heavily at the same time. Fortunately for readers, NIKE's earnings per share have been growing at 14% a year for the past five years. Earnings per share have been growing rapidly and the company is retaining a majority of its earnings within the business. Fast-growing businesses that are reinvesting heavily are enticing from a dividend perspective, especially since they can often increase the payout ratio later.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. NIKE has delivered 15% dividend growth per year on average over the past ten years. It's exciting to see that both earnings and dividends per share have grown rapidly over the past few years.

The Bottom Line

From a dividend perspective, should investors buy or avoid NIKE? It's great that NIKE is growing earnings per share while simultaneously paying out a low percentage of both its earnings and cash flow. It's disappointing to see the dividend has been cut at least once in the past, but as things stand now, the low payout ratio suggests a conservative approach to dividends, which we like. Overall we think this is an attractive combination and worthy of further research.

Curious what other investors think of NIKE? See what analysts are forecasting, with this visualisation of its historical and future estimated earnings and cash flow.

If you're in the market for dividend stocks, we recommend checking our list of top dividend stocks with a greater than 2% yield and an upcoming dividend.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About NYSE:NKE

NIKE

Designs, develops, markets, and sells athletic and casual footwear, apparel, equipment, accessories, and services for men, women, and kids in North America, Europe, the Middle East, Africa, Greater China, the Asia Pacific, and Latin America.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)