Advertisement

- India

- /

- Construction

- /

- NSEI:CORALFINAC

Coral India Finance and Housing Limited's (NSE:CORALFINAC) Subdued P/E Might Signal An Opportunity

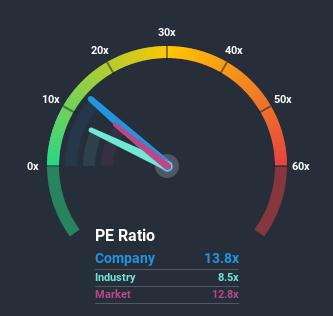

With a median price-to-earnings (or "P/E") ratio of close to 13x in India, you could be forgiven for feeling indifferent about Coral India Finance and Housing Limited's (NSE:CORALFINAC) P/E ratio of 13.8x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/E.

For example, consider that Coral India Finance and Housing's financial performance has been poor lately as it's earnings have been in decline. One possibility is that the P/E is moderate because investors think the company might still do enough to be in line with the broader market in the near future. If you like the company, you'd at least be hoping this is the case so that you could potentially pick up some stock while it's not quite in favour.

See our latest analysis for Coral India Finance and Housing

Does Growth Match The P/E?

In order to justify its P/E ratio, Coral India Finance and Housing would need to produce growth that's similar to the market.

Taking a look back first, the company's earnings per share growth last year wasn't something to get excited about as it posted a disappointing decline of 2.5%. This means it has also seen a slide in earnings over the longer-term as EPS is down 1.0% in total over the last three years. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

Weighing that medium-term earnings trajectory against the broader market's one-year forecast for a contraction of 4.2% shows the market is even less attractive on an annualised basis.

In light of this, the fact Coral India Finance and Housing's P/E sits in line with the majority of other companies is unanticipated but certainly not shocking. There's no guarantee the P/E has found a floor yet with recent earnings going backwards, despite the market heading down even harder. It's conceivable that the P/E falls to lower levels if the company doesn't improve its profitability, which would be difficult to do with the current market outlook.

The Key Takeaway

The price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our examination of Coral India Finance and Housing revealed its narrower three-year contraction in earnings isn't contributing to its P/E as much as we would have predicted, given the market is set to shrink even more. There could be some unobserved threats to earnings preventing the P/E ratio from matching this more attractive performance. Perhaps there is some hesitation about the company's ability to stay its recent course and resist the broader market turmoil. At least the risk of a price drop looks to be subdued, but investors seem to think future earnings could see some volatility.

It's always necessary to consider the ever-present spectre of investment risk. We've identified 4 warning signs with Coral India Finance and Housing, and understanding these should be part of your investment process.

It's important to make sure you look for a great company, not just the first idea you come across. So take a peek at this free list of interesting companies with strong recent earnings growth (and a P/E ratio below 20x).

If you’re looking to trade Coral India Finance and Housing, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:CORALFINAC

Coral India Finance and Housing

Provides investment services in the in India.

Flawless balance sheet average dividend payer.

Market Insights

Advertisement

Community Narratives

RIO is poised to weather a depressed iron ore environment, but commodity diversification comes with lower margins

Fair Value AU$110.51|3.0% overvalued

DU

Community Contributor

The demand for personalized medicine will keep Thermo Fisher Scientific thriving

Fair Value US$540.27|19.5% undervalued

UN

Community Contributor

Silver Play by A Family with 10x Potential

Fair Value UK£24.00|87.3% undervalued

RO

Community Contributor