Advertisement

- United States

- /

- Software

- /

- NasdaqGM:TLS

Telos Corporation's (NASDAQ:TLS) Revenues Are Not Doing Enough For Some Investors

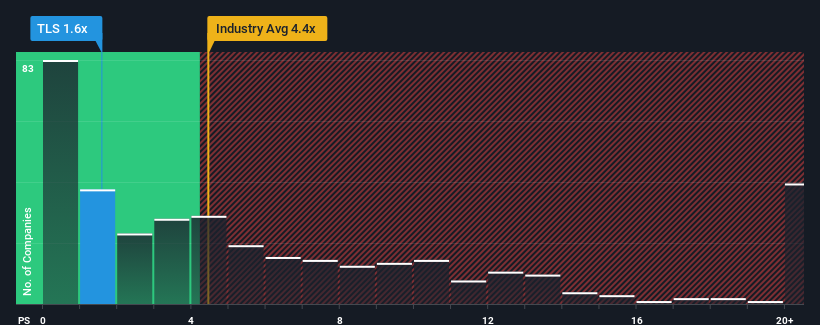

You may think that with a price-to-sales (or "P/S") ratio of 1.6x Telos Corporation (NASDAQ:TLS) is definitely a stock worth checking out, seeing as almost half of all the Software companies in the United States have P/S ratios greater than 4.4x and even P/S above 11x aren't out of the ordinary. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so limited.

See our latest analysis for Telos

How Telos Has Been Performing

Telos could be doing better as its revenue has been going backwards lately while most other companies have been seeing positive revenue growth. Perhaps the P/S remains low as investors think the prospects of strong revenue growth aren't on the horizon. So while you could say the stock is cheap, investors will be looking for improvement before they see it as good value.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Telos.Is There Any Revenue Growth Forecasted For Telos?

There's an inherent assumption that a company should far underperform the industry for P/S ratios like Telos' to be considered reasonable.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 31%. This means it has also seen a slide in revenue over the longer-term as revenue is down 29% in total over the last three years. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

Shifting to the future, estimates from the six analysts covering the company suggest revenue growth is heading into negative territory, declining 3.6% over the next year. With the industry predicted to deliver 15% growth, that's a disappointing outcome.

In light of this, it's understandable that Telos' P/S would sit below the majority of other companies. Nonetheless, there's no guarantee the P/S has reached a floor yet with revenue going in reverse. Even just maintaining these prices could be difficult to achieve as the weak outlook is weighing down the shares.

What We Can Learn From Telos' P/S?

Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

As we suspected, our examination of Telos' analyst forecasts revealed that its outlook for shrinking revenue is contributing to its low P/S. As other companies in the industry are forecasting revenue growth, Telos' poor outlook justifies its low P/S ratio. Unless there's material change, it's hard to envision a situation where the stock price will rise drastically.

You should always think about risks. Case in point, we've spotted 4 warning signs for Telos you should be aware of, and 1 of them is a bit unpleasant.

If these risks are making you reconsider your opinion on Telos, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Telos might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:TLS

Telos

Provides cyber, cloud, and enterprise security solutions in the United States and internationally.

Flawless balance sheet and undervalued.

Market Insights

Advertisement

Weekly Picks

WE

WealthAP on PayPal Holdings ·

The "Sleeping Giant" Stumbles, Then Wakes Up

Fair Value:US$8229.7% undervalued

60 followersusers have followed this narrative

4 commentsusers have commented on this narrative

31 likesusers have liked this narrative

WO

woodworthfund on Bumble ·

Swiped Left by Wall Street: The BMBL Rebound Trade

Fair Value:US$961.3% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

WE

WealthAP on Duolingo ·

Duolingo (DUOL): Why A 20% Drop Might Be The Entry Point We've Been Waiting For

Fair Value:US$268.6434.2% undervalued

32 followersusers have followed this narrative

5 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

AN

andre_santos on Mota-Engil SGPS ·

Mota-Engil's Intrinsic and Historical Valuation

Fair Value:€4.77.8% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

andre_santos on Ferrari ·

Ferrari's Intrinsic and Historical Valuation

Fair Value:€243.5633.7% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

andre_santos on SAP ·

SAP's Intrinsic and Historical Valuation

Fair Value:€162.7330.5% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

AG

Agricola on Excellon Resources ·

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Fair Value:CA$31.898.3% undervalued

71 followersusers have followed this narrative

13 commentsusers have commented on this narrative

23 likesusers have liked this narrative

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25422.2% overvalued

72 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0226.9% undervalued

1027 followersusers have followed this narrative

6 commentsusers have commented on this narrative

29 likesusers have liked this narrative