Happy 2026!

2025 started out on an optimistic note, hit some major speed bumps within the first few months, before returning to business as usual with multiple markets ending the year at record highs.

So what’s in store for 2026? To answer that, we’ll be looking at market outlooks published by research teams around the world to see where they agree and where they don’t.

We’re also going to break down the major themes and what they could mean for key markets.

What Happened In Markets This Week?

Here’s a quick summary of what’s been going on:

🛢️ US oil firms are cautious after Trump seizes control in Venezuela ( NBC , TIME )

- Trump shocked global observers this week by capturing Venezuela’s president in a military raid and announcing the U.S. will oversee the country during a transition.

- He says Venezuela will turn over up to 50 million barrels of oil, with U.S. companies like Chevron, Exxon, and Conoco poised to rebuild the country’s oil sector.

- But so far, most firms are staying quiet or cautious. Chevron is still active, but Exxon and Conoco haven’t confirmed interest, and PDVSA says it’s only in negotiations – not a done deal.

- Venezuela’s oil is heavy, costly to process, and the infrastructure is wrecked. Experts say restoring production could take a decade and $200B.

- The U.S. is also marketing Venezuela’s crude and controlling the proceeds, raising legal and diplomatic questions from allies and rivals like China.

- While the broader political implications are still unfolding, from an investor lens this is a high-risk, low-clarity scenario.

🚗 Nvidia’s self-driving reveal spooks Tesla investors but Musk shrugs it off ( Yahoo )

- Nvidia showed off its new “Alpamayo” AI platform at CES, pitching it as the ChatGPT moment for autonomous vehicles. Mercedes will be first to roll it out with other carmakers lined up.

- Tesla stock dipped 3% as investors weighed whether this could finally challenge Tesla’s robotaxi lead.

- Elon Musk responded by saying Nvidia’s tech is at least 5 to 6 years away from competing seriously, citing the long road from working demos to real-world safety and scale.

- Nvidia’s strategy is open-source and chip-based, letting any automaker adopt it – unlike Tesla’s closed system. That could help Alpamayo scale faster across the industry.

- Still, Tesla’s head start in data and deployment matters. Nvidia’s future in AV is promising, but for now it’s more of a threat to other legacy OEMs than to Tesla itself.

💻 Intel pops on new AI PC chips ( Yahoo )

- Intel jumped 8% after showing off its new Panther Lake chips and Core Ultra Series 3 laptops at CES.

- These are Intel’s first chips on its next-gen 18A process, with up to 60% better performance and 27-hour battery life.

- The chips are AI-ready and headed for 200+ device models—plus new plans for gaming handhelds and robotics use cases.

- It's a big moment for Intel’s comeback narrative, as it fights to reclaim share from AMD and Nvidia.

- Execution remains key, but early orders and partner support show this isn’t just vaporware.

💹 Bank of Japan doubles down on rate hikes as inflation lingers ( Reuters )

- Japan’s central bank chief says more interest rate hikes are coming, after raising rates to a 30-year high of 0.75%.

- Inflation’s been above 2% for nearly four years, and a weak yen is still pushing up import prices.

- The BOJ wants to keep tightening “gradually” as wages rise and the economy moves out of deflation mode.

- Bond markets are already reacting – 10-year JGB yields hit a 27-year high this week.

- A tighter Japan could lift the yen and dampen carry trades, with ripple effects for global fixed income.

📈 Samsung forecasts record profit as AI memory demand goes wild ( Reuters )

- Samsung expects Q4 profit to triple to $13.8B, beating estimates and setting a new all-time quarterly record.

- The AI boom has sent memory chip demand (and prices) skyrocketing, with DRAM contract prices up 313% year over year.

- Analysts see chip shortages persisting into 2026, as hyperscalers race to build out data centers and AI factories.

- Mobile margins may take a hit, though, as higher chip costs eat into profits and price hikes are tough to pass on.

- Samsung’s HBM chips are getting buzz too – Nvidia customers reportedly say “Samsung is back,” fueling hopes of a market share grab.

Which markets will sink or swim in 2026?

In general, analysts are once again quite optimistic, but differ on the details.

Key Themes for Global Markets in 2026

JP Morgan defines the current era of risk and opportunity as “Multidimensional Polarization . ” From a geopolitical perspective, the world has become increasingly polarized – societies are now deeply divided into opposing groups.

Polarization is now also common when it comes to central bank policy, inflation, and market sectors that are AI related vs. those that aren’t. It even applies to sectors and companies within individual markets.

With that backdrop, here are some key themes we’re seeing markets start with this year:

- The AI revolution : The hype behind AI has resulted in a massive capex (capital expenditure) cycle, which has contributed to economic growth (mainly in the US) and earnings growth for companies in the supply chain. Whether these capital investments later translate into productivity gains remains to be seen.

- Global AI leadership divide : The AI race isn't equally distributed globally. The United States and China lead AI adoption and investment, while Europe lags significantly. European technology sector capital commitments total just $250-300 billion over the next two years, compared to over $2 trillion in the U.S .

- High valuations across multiple regions: The concentrated run-up in certain sectors and regions, particularly US megacap technology, has pushed valuations to historic highs. This could act as a significant headwind for growth stocks, and possibly create an opportunity for value stocks.

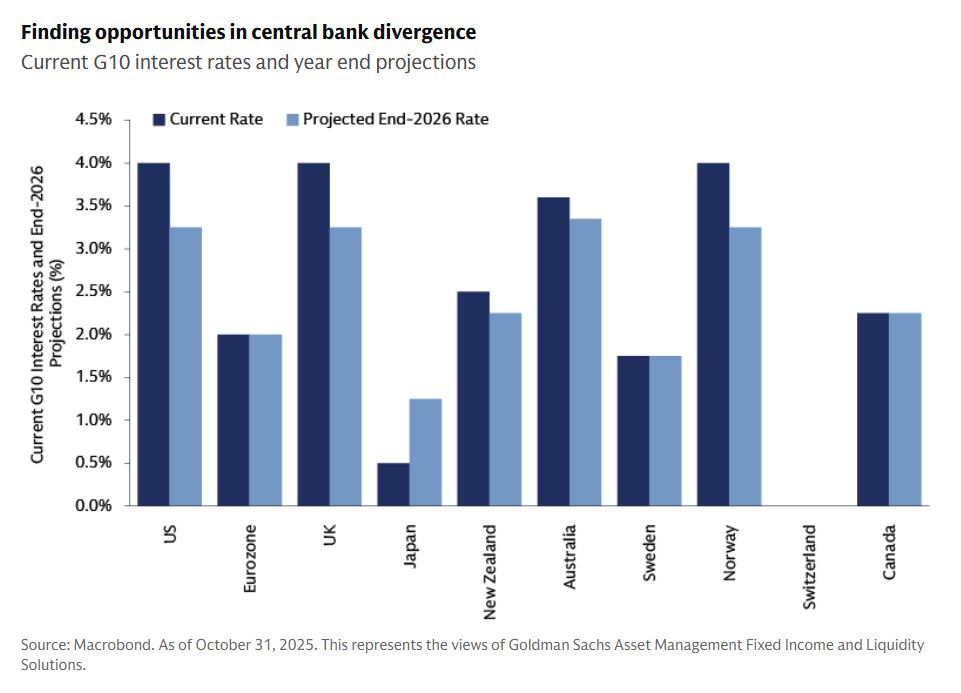

- Rate cuts in the West: The US Federal Reserve is expected to continue its easing cycle and the Bank of England seems to finally have room to bring rates down to more affordable levels. There is debate about the European Central Bank’s most likely path. Sticky inflation is expected to remain a factor, seen hovering around 3% rather than the 2% central banks are aiming for.

- Rate hikes in the East: In stark contrast, the Bank of Japan is expected to tighten policy and hike rates as its economy finally escapes decades of deflation. This divergence has profound implications for investors, as it will affect the cost of capital for companies that borrow cheaply in Japan (the Yen carry trade).

- Potential currency volatility: The monetary divergence is a prime catalyst for currency volatility, with a broad consensus forming around a weaker US dollar against a strengthening Euro and Yen, directly impacting the profitability of large multinational exporters and importers.

The Risks for Global Markets in 2026

Markets ‘climbed a wall of worry’ in 2025 - which is often the case. Skepticism results in cash building up on the sidelines, which then adds more fuel to subsequent rallies.

Most of the same risks are still present, with some becoming more significant:

- Geopolitical tension: US foreign policy in 2025 has added to the uncertainty for investors.

- US-China relations: A temporary trade deal was signed in October 2025, with a permanent deal due to be finalised later this year. But there are a lot of complicating factors that could upset the current truce before then .

- Government debt: There seems to be little sign that government spending (and borrowing) will be reigned in anytime soon.

- Market concentration and valuations : The dominance of the “ Magnificent 7” has continued, and expectations are sky high.

- US tariffs: Donald Trump’s unpredictable approach to tariffs could result in even higher tariffs for trade partners and another escalation in trade wars.

- Potential AI related job losses : So far, AI’s biggest impact has been on entry level jobs. If this spreads to more highly skilled roles the economic impact could be far more significant.

As always investors need to accept that risk is a part of the process. Rather than trying to time the market to avoid risk, portfolios should be constructed to reduce the impact.

Now let’s take a look at the drivers behind each region this year.

🇺🇸 United States: Growth Momentum Meets Valuation Concerns

The US economy remains strong, powered by a dual boost of fiscal stimulus and a wave of AI-related capex approaching an estimated US$500 billion in 2026. With this combination, analysts expect corporate earnings to remain solid.

The AI boom is broadening beyond the handful of mega-caps and start-ups that dominated early on. The current phase, which includes the buildout of tangible infrastructure, includes more companies and sectors. This includes:

- a wider range of semiconductor and hardware companies,

- power utilities

- industrials (electrical infrastructure, automation, manufacturing)

- real estate.

Performance is therefore expected to diversify beyond the tech sector, and ultimately beyond the US too. Some analysts suggest the best opportunities may now lie in unappreciated small and mid-cap "enablers."

However, expectations and valuations are high – which means risks are also rising. Some analysts believe value stocks are more compelling and that sectors like industrials, financials, and select consumer segments may benefit most as AI adoption broadens beyond technology companies.

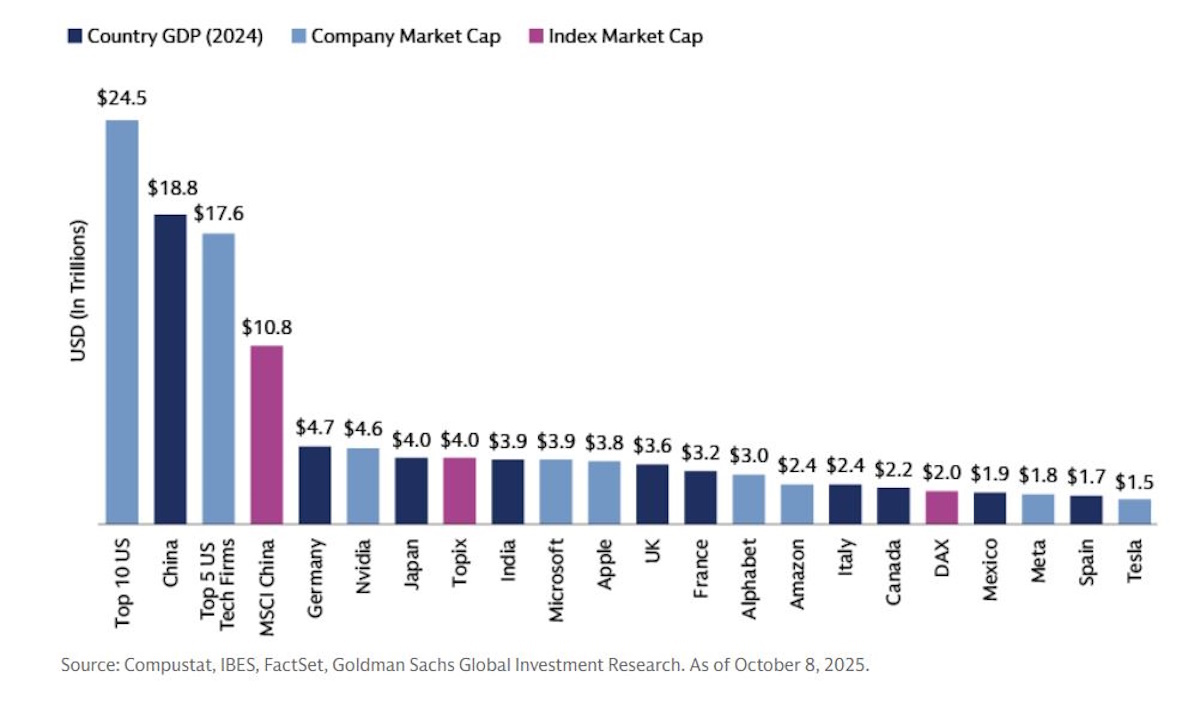

The valuation and concentration concerns are relevant to global investors too. The chart below shows how big the top 10 US companies and top 5 US tech companies are compared to entire economies and stock indexes. Any volatility in that part of the market would be felt around the globe.

In terms of policy changes, Morgan Stanley sees expiration of healthcare subsidies as a potential headwind or consumers and businesses. This, along with tariffs could lead to a rebound in inflation – which is a risk to the rate cutting cycle.

🇨🇦 Canada: Slowing Corporate Growth

Corporate profit growth is expected to slow in Canada, and the central bank is now holding rates steady. The commodity focussed economy will therefore be even more sensitive to the pace of global industrial activity and the trajectory of commodity prices.

Certain sectors like real estate and energy may benefit from infrastructure spending related to AI data center development.

🇬🇧 UK: Monetary Policy Tailwinds

A key differentiator for UK markets is the improving inflation outlook. Annual headline inflation is expected to fall from 3.8% to 2.2% by end-2026, driven by the removal of green levies on energy bills and lower energy costs. This disinflationary process should allow the Bank of England to continue easing, with rates forecast to decline to 3.25%.

The combination of falling rates and stable growth could work for both domestic-focused companies and those benefiting from a weaker pound. Earnings for UK companies are expected to grow 13.7%, which makes the current P/E ratio of ~21x appear attractive on a relative basis.

💶 Europe: Structural Challenges Limit AI Benefits

The outlook for Europe is more fragile than the US. While fiscal stimulus in Germany and reindustrialization efforts are providing support, the region may lag as the effects of 2025's tariff front-loading weigh on its manufacturing sector.

However, analysts are optimistic about certain value and cyclical stocks that could benefit from infrastructure and defense spending and reindustrialization initiatives.

Analysts at Jefferies highlighted well-positioned financials (e.g. Société Générale ), building materials (e.g. Geberit , Heidelberg Materials ), and automotives (e.g. Volvo ).

Looking further ahead Europe faces challenges due to its limited AI infrastructure buildout. Unlike the U.S., Europe lacks strong AI dynamics to drive productivity growth. Investment spending is concentrated in "old-world" industries like automobiles and pharmaceuticals rather than software, semiconductors, and AI technologies.

🇦🇺 Australia: Tied to Commodity Demand

Australia’s economy would benefit from interest rate cuts, but analysts are divided on the outlook for rates. At the same time its fortunes are closely linked to the strength of China's economy, its largest trading partner, especially concerning commodity demand.

Aside from commodity producers, its financial sector could gain from stable economic conditions and reasonable valuations.

🇯🇵 Japan: Now Shareholder Friendly

Japan is again a consensus favorite among analysts for 2026, a remarkable shift after decades of stagnation. The country is benefiting from several long-term tailwinds.

The economic policies of new Prime Minister Sanae Takaichi, dubbed "Sanaenomics," are expected to boost domestic spending, transitioning the economy away from its reliance on exports.

A significant shift is underway, forcing companies to unlock vast sums of cash for share buybacks, dividends, and investment. This focus on shareholder returns is fundamentally making the market more attractive to international investors.

Specific sectors likely to benefit from government policy include defense, nuclear energy, and technology (AI, semiconductors).

🇮🇳 India: The Secular Growth Market

India represents a secular growth story, rather than a cyclical one.

Strong GDP growth, a young and growing population, and digitalization are all contributing to the narrative. In addition, its role as a key beneficiary of global supply chain diversification away from China is boosting its manufacturing sector.

India's established technology services sector is also positioned to benefit from global AI adoption.

India is positioned as one of the most attractive long-term markets - but it has underperformed when investors chased stimulus driven returns in China.

🇨🇳🇭🇰 China and Hong Kong: Stimulus vs. a Slowing Economy

In recent years, China’s market has been driven by strong policy support, a leadership position in key innovation areas like AI and EVs, and a massive pool of household savings that represents "dry powder" for the market. Policy-driven rallies remain a distinct possibility.

However, investors need to be cautious and extremely selective. The domestic economy is still weak, particularly the property sector. Intense internal competition is eroding profit margins, and US-China trade tensions remain a wild card, sensitive to political and regulatory shocks.

🇰🇷 Korea: AI and Governance Tailwinds

South Korea was the top performing market in 2025 and a major beneficiary of the current phase of the AI capex cycle. While the cycle continues, companies like Samsung and SK Hynix are likely to boost sentiment.

However, a change in global sentiment around AI would affect Korea more than most countries, so the market does come with a large potential risk.

In addition to the tech tailwinds, ongoing governance reforms are making the market more transparent and attractive to international investors, helping to close the so-called "Korea discount."

🌍 Emerging Markets

Emerging Markets generally had a great year in 2025, supported by loosening local monetary policy, a softer US dollar, and strong global demand for tech exports. They are expected to continue to benefit from lower local interest rates, attractive valuations, and improving corporate governance.

However, investors need to assess each market and each company as a separate entity. Emerging economies are decoupling from one another and there are unique factors and risks affecting each market.

In particular, trade relations with the US could improve – or deteriorate – very quickly.

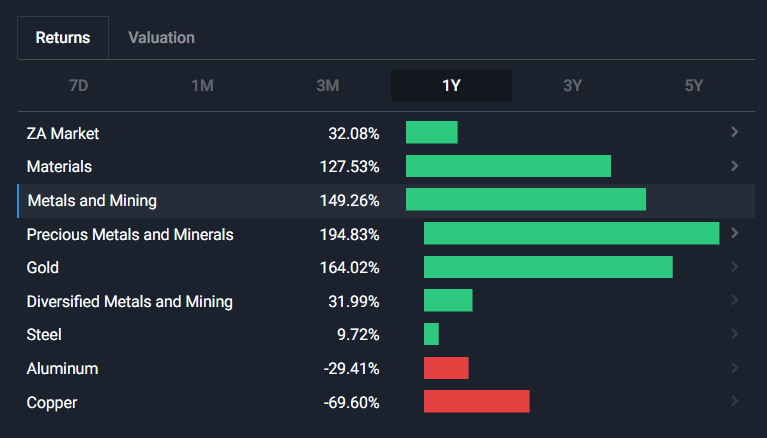

Each market structure is also a key return driver. South Africa’s equity market, for example, had its best year in 20 years in 2025 – driven primarily by gold and other precious metals. Future returns will be closely tied to the same industries.

💡 The Insight: Diversification vs ‘Diworse-ification’

Once again, there’s a lot riding on the AI trade, and once again, investors have some significant risks to keep in mind.

Diversification is probably the best way to protect your portfolio from these risks. And it’s certainly better than trying to predict future performance. But, in this polarized world, there’s a real risk of diversifying into low quality stocks, or ETFs that hold them.

Peter Lynch coined the term ‘diworsification’, which means making things worse by diversifying for the sake of it. Most of the listed companies out there might not be any better than the ones you want to diversify away from.

As an example, you might be concerned about having too much exposure to US AI stocks, so you decide to invest in European AI stocks. The result ends up being that you limit your upside, but ultimately have the same downside risk.

So how do you avoid this trap?

- Be careful of highly correlated sectors: Companies in some sectors are highly correlated regardless of where they are located. Examples include technology and gold miners. Others, like financials and consumer businesses, are more exposed to domestic economies.

- Be selective : If you can’t find a stock that meets all the right criteria, keep that capital in cash and wait until you do find a winner.

- Be even more selective when it comes to growth stocks: The higher the expectations, the higher the valuation is likely to be, and that implies more potential downside.

- Cash is king : Companies with strong balance sheets and free cash flow are in a much better position to weather a downturn than those trading on hopes and dreams.

Looking for companies with strong fundamentals? Check out these screeners:

Alternatively, have a look at the narratives written by members of the community .

Key Events Next Week

Tuesday

- 🇺🇸 US Inflation Rate YoY DEC

- Previous: 2.7%

- ➡️ Why it matters: The inflation rate fell meaningfully in November, so this print could confirm the softer trend, or suggest it was an anomaly.

Wednesday

- 🇨🇳 CN Balance of Trade DEC

- 📉 Forecast: $105B, Previous: $111.68B

- ➡️ Why it matters: A narrowing surplus suggests Chinese exports are falling, though the magnitude is marginal.

- 🇺🇸 US PPI MoM OCT

- 📈 Forecast: 0.4%, Previous: 0.3%

- ➡️ Why it matters: A small increase in producer prices is unlikely to affect Fed policy.

- 🇺🇸 US Retail Sales MoM NOV

- 📈 Forecast: 0.3%, Previous: 0%

- ➡️ Why it matters: A rebound in consumer spending indicates economic resilience.

Thursday

- 🇬🇧 GB GDP 3-Month Avg NOV

- ▶️ Forecast: -0.1%, Previous: -0.1%

- ➡️ Why it matters: UK growth remains close to zero - but stable.

- 🇬🇧 GB Industrial Production MoM NOV

- 📉 Forecast: 1.0%, Previous: 1.1%

- ➡️ Why it matters: A slight slowdown in output is in line with GDP numbers.

- 🇩🇪 DE Full Year GDP Growth 2026

- 📈 Forecast: 0.2%, Previous: -0.2%

- ➡️ Why it matters: A return to positive territory would signal a potential recovery for Europe's largest economy.

Earning’s season gets under way this week with the major banks and a handful of other companies:

- JP Morgan

- Bank of America

- Wells Fargo

- Morgan Stanley

- Citigroup

- Goldman Sachs

- BlackRock

- Delta Air Lines

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Richard Bowman and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Richard Bowman

Richard is an analyst, writer and investor based in Cape Town, South Africa. He has written for several online investment publications and continues to do so. Richard is fascinated by economics, financial markets and behavioral finance. He is also passionate about tools and content that make investing accessible to everyone.