- South Africa

- /

- Packaging

- /

- JSE:TPC

Here's Why Shareholders May Want To Be Cautious With Increasing Transpaco Limited's (JSE:TPC) CEO Pay Packet

Key Insights

- Transpaco will host its Annual General Meeting on 29th of November

- CEO Phil Abelheim's total compensation includes salary of R7.23m

- Total compensation is 1,114% above industry average

- Transpaco's total shareholder return over the past three years was 162% while its EPS grew by 16% over the past three years

Under the guidance of CEO Phil Abelheim, Transpaco Limited (JSE:TPC) has performed reasonably well recently. As shareholders go into the upcoming AGM on 29th of November, CEO compensation will probably not be their focus, but rather the steps management will take to continue the growth momentum. However, some shareholders may still be hesitant of being overly generous with CEO compensation.

View our latest analysis for Transpaco

How Does Total Compensation For Phil Abelheim Compare With Other Companies In The Industry?

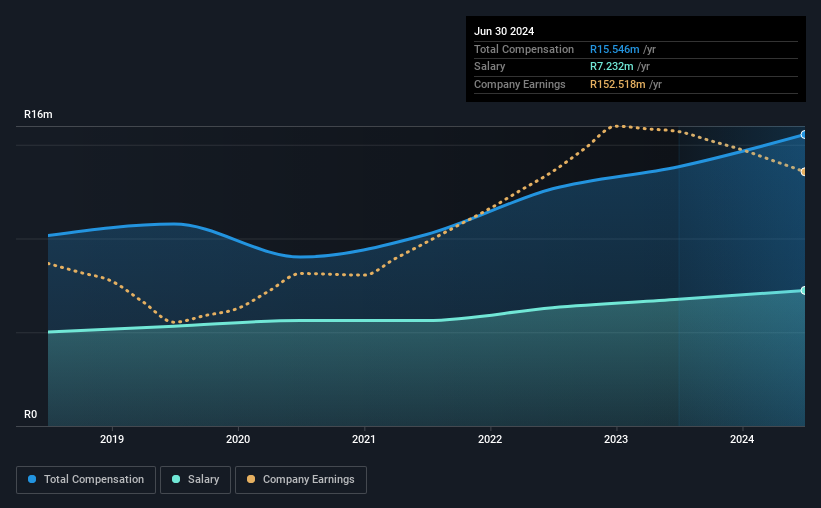

At the time of writing, our data shows that Transpaco Limited has a market capitalization of R1.0b, and reported total annual CEO compensation of R16m for the year to June 2024. That's a notable increase of 12% on last year. While we always look at total compensation first, our analysis shows that the salary component is less, at R7.2m.

In comparison with other companies in the South Africa Packaging industry with market capitalizations under R3.6b, the reported median total CEO compensation was R1.3m. Hence, we can conclude that Phil Abelheim is remunerated higher than the industry median. Furthermore, Phil Abelheim directly owns R144m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | R7.2m | R6.8m | 47% |

| Other | R8.3m | R7.1m | 53% |

| Total Compensation | R16m | R14m | 100% |

On an industry level, around 68% of total compensation represents salary and 32% is other remuneration. Transpaco pays a modest slice of remuneration through salary, as compared to the broader industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

A Look at Transpaco Limited's Growth Numbers

Transpaco Limited's earnings per share (EPS) grew 16% per year over the last three years. In the last year, its revenue is down 4.0%.

This demonstrates that the company has been improving recently and is good news for the shareholders. It's always a tough situation when revenues are not growing, but ultimately profits are more important. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Transpaco Limited Been A Good Investment?

We think that the total shareholder return of 162%, over three years, would leave most Transpaco Limited shareholders smiling. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

To Conclude...

Seeing that the company has put up a decent performance, only a few shareholders, if any at all, might have questions about the CEO pay in the upcoming AGM. Still, not all shareholders might be in favor of a pay raise to the CEO, seeing that they are already being paid higher than the industry.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. That's why we did some digging and identified 2 warning signs for Transpaco that you should be aware of before investing.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Transpaco might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About JSE:TPC

Transpaco

Engages in the manufacturing, recycling, and distribution of paper and plastic packaging products in South and Southern Africa.

Excellent balance sheet average dividend payer.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Unicycive Therapeutics (Nasdaq: UNCY) – Preparing for a Second Shot at Bringing a New Kidney Treatment to Market (TEST)

Rocket Lab USA Will Ignite a 30% Revenue Growth Journey

Dollar general to grow

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Trending Discussion