- United States

- /

- Other Utilities

- /

- NYSE:UTL

Unitil (NYSE:UTL) Has Announced That It Will Be Increasing Its Dividend To $0.405

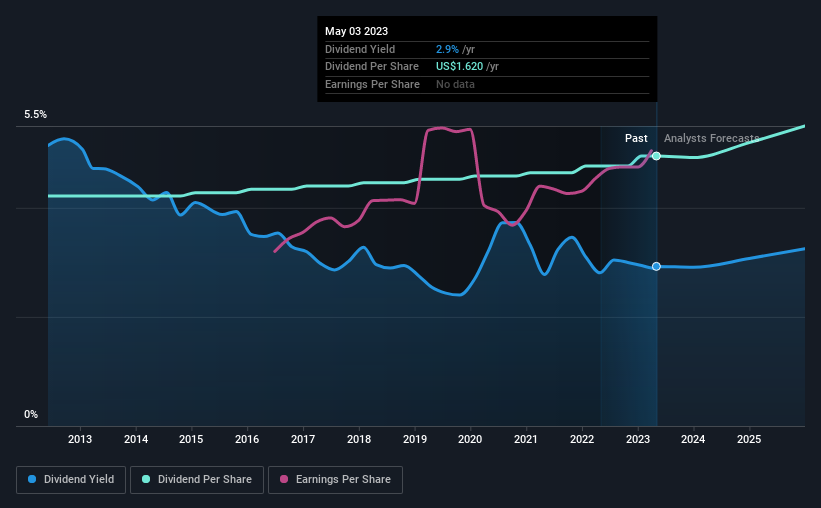

The board of Unitil Corporation (NYSE:UTL) has announced that it will be paying its dividend of $0.405 on the 30th of May, an increased payment from last year's comparable dividend. Based on this payment, the dividend yield for the company will be 2.9%, which is fairly typical for the industry.

Check out our latest analysis for Unitil

Unitil's Payment Has Solid Earnings Coverage

While it is always good to see a solid dividend yield, we should also consider whether the payment is feasible. Before making this announcement, Unitil was earning enough to cover the dividend, but it wasn't generating any free cash flows. No cash flows could definitely make returning cash to shareholders difficult, or at least mean the balance sheet will come under pressure.

The next year is set to see EPS grow by 13.7%. If the dividend continues on this path, the payout ratio could be 52% by next year, which we think can be pretty sustainable going forward.

Unitil Has A Solid Track Record

Even over a long history of paying dividends, the company's distributions have been remarkably stable. Since 2013, the dividend has gone from $1.38 total annually to $1.62. This works out to be a compound annual growth rate (CAGR) of approximately 1.6% a year over that time. Slow and steady dividend growth might not sound that exciting, but dividends have been stable for ten years, which we think makes this a fairly attractive offer.

Unitil May Find It Hard To Grow The Dividend

Investors could be attracted to the stock based on the quality of its payment history. Earnings per share has been crawling upwards at 4.0% per year. The company has been growing at a pretty soft 4.0% per annum, and is paying out quite a lot of its earnings to shareholders. This could mean the dividend doesn't have the growth potential we look for going into the future.

In Summary

Overall, we always like to see the dividend being raised, but we don't think Unitil will make a great income stock. While the low payout ratio is a redeeming feature, this is offset by the minimal cash to cover the payments. Overall, we don't think this company has the makings of a good income stock.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. Case in point: We've spotted 2 warning signs for Unitil (of which 1 is significant!) you should know about. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:UTL

Unitil

A public utility holding company, engages in the distribution of electricity and natural gas.

Average dividend payer with questionable track record.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

UnitedHealth Stock: Why Scale, Data, and Integration Still Matter in U.S. Healthcare

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)