Advertisement

- United States

- /

- Transportation

- /

- NasdaqGS:SAIA

How Saia's (SAIA) Strong Earnings and Cost Control Strategy May Influence Investor Sentiment

Simply Wall St

Reviewed by Sasha Jovanovic

- Saia recently posted a strong quarterly report, with revenue and EBITDA both surpassing analyst expectations and leadership emphasizing customer service, cost control, and adapting operations as sector changes roll out.

- The company’s above-estimate earnings, achieved in a period of broader adjustments within the less-than-truckload industry, reflect its focus on operational efficiency and adaptability.

- We'll explore how Saia's strong operational results and emphasis on cost discipline influence its investment outlook going forward.

Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Saia Investment Narrative Recap

To be a shareholder in Saia, one needs to believe that disciplined cost management, expanding national coverage, and a focus on service quality can help offset freight industry challenges such as muted shipment growth and a structurally inflationary cost base. The recent earnings report, with revenue and EBITDA above expectations, reinforces Saia’s ability to flex its operating model, though the positive surprise has not reversed the stock’s downward trend, indicating that the main catalyst remains the company’s operational efficiency gains while the immediate risk continues to be sluggish freight volumes and persistent cost pressure.

Among recent developments, Saia’s report of a 1.2% decline in July 2025 shipments per workday, followed by further softness in August, is especially relevant given its context within the sector’s broader adjustments. This ongoing weakness in shipment growth directly ties to the near-term catalyst of Saia achieving higher capacity utilization and cost control through its expanding terminal network, a dynamic that remains under scrutiny as new facilities must ramp up to justify the significant capital investment.

By contrast, investors should also be aware that if shipment volumes remain under pressure due to weak industrial demand, then the risk of network overextension and...

Read the full narrative on Saia (it's free!)

Saia's outlook anticipates $3.9 billion in revenue and $456.7 million in earnings by 2028. This scenario assumes 6.6% annual revenue growth and a $166.6 million earnings increase from the current $290.1 million.

Uncover how Saia's forecasts yield a $337.25 fair value, a 15% upside to its current price.

Exploring Other Perspectives

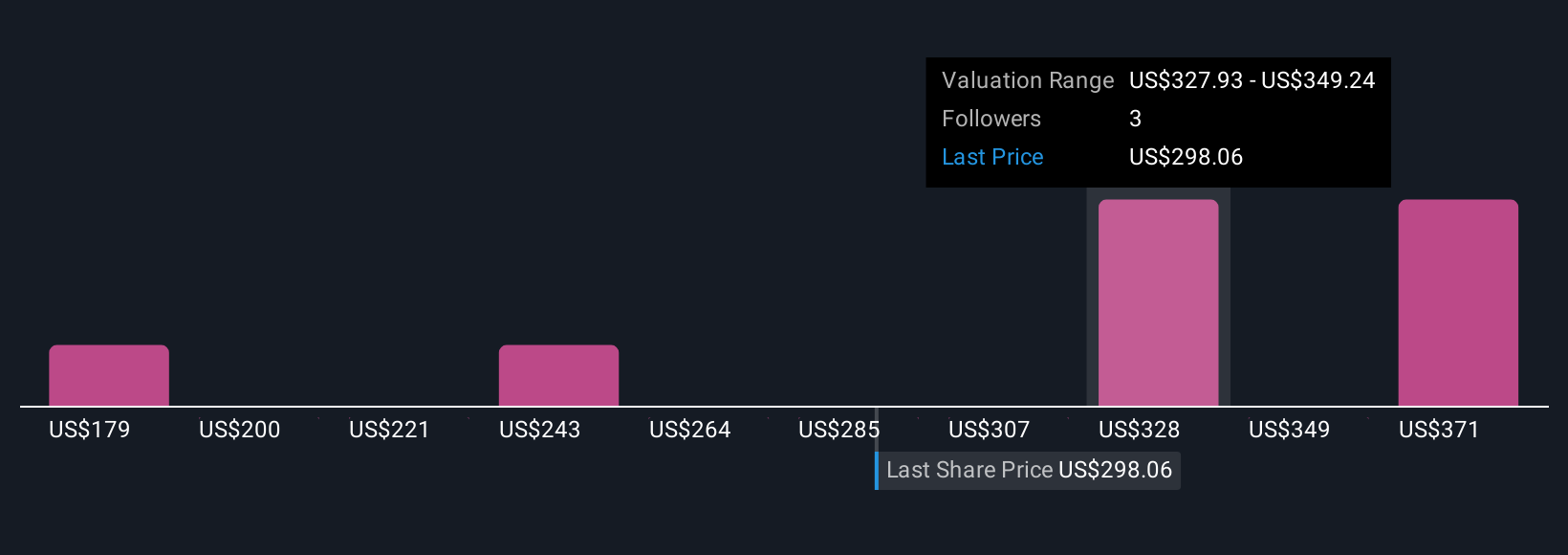

Across four fair value estimates from the Simply Wall St Community, projections for Saia’s worth span from US$178.76 to US$391.40. Many participants factor in the challenge of muted shipment growth, showing how individual expectations for the company’s future profitability can vary widely.

Explore 4 other fair value estimates on Saia - why the stock might be worth 39% less than the current price!

Build Your Own Saia Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Saia research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Saia research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Saia's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 24 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:SAIA

Adequate balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor