- United States

- /

- Telecom Services and Carriers

- /

- NasdaqGS:CCOI

Assessing Cogent Stock After 47% Fall and Projected Free Cash Flow Rebound in 2025

Reviewed by Bailey Pemberton

If you’re staring at Cogent Communications Holdings stock and asking yourself what comes next, you’re definitely not alone. After all, this is a company that has provided a wild ride for investors. In just one week, Cogent edged up by 1.3%, while over the past month it’s delivered a much punchier 9.4% gain. Still, when you zoom out, the picture gets trickier: the stock is down a stunning 47.6% year-to-date and has lost 42.3% over the past year. Even stretching the timeline further, the declines persist, with negative returns of 7.0% over three years and 12.8% across five years.

What’s behind all this volatility? For much of the market, risk perception seems to have shifted rapidly, possibly driven by evolving trends in bandwidth demand, telecommunications infrastructure spending, and recent competitive moves among major industry players. Growth-focused investors might see recent positive movement as a sign of resilience, while cautious types could be wary of lingering headwinds.

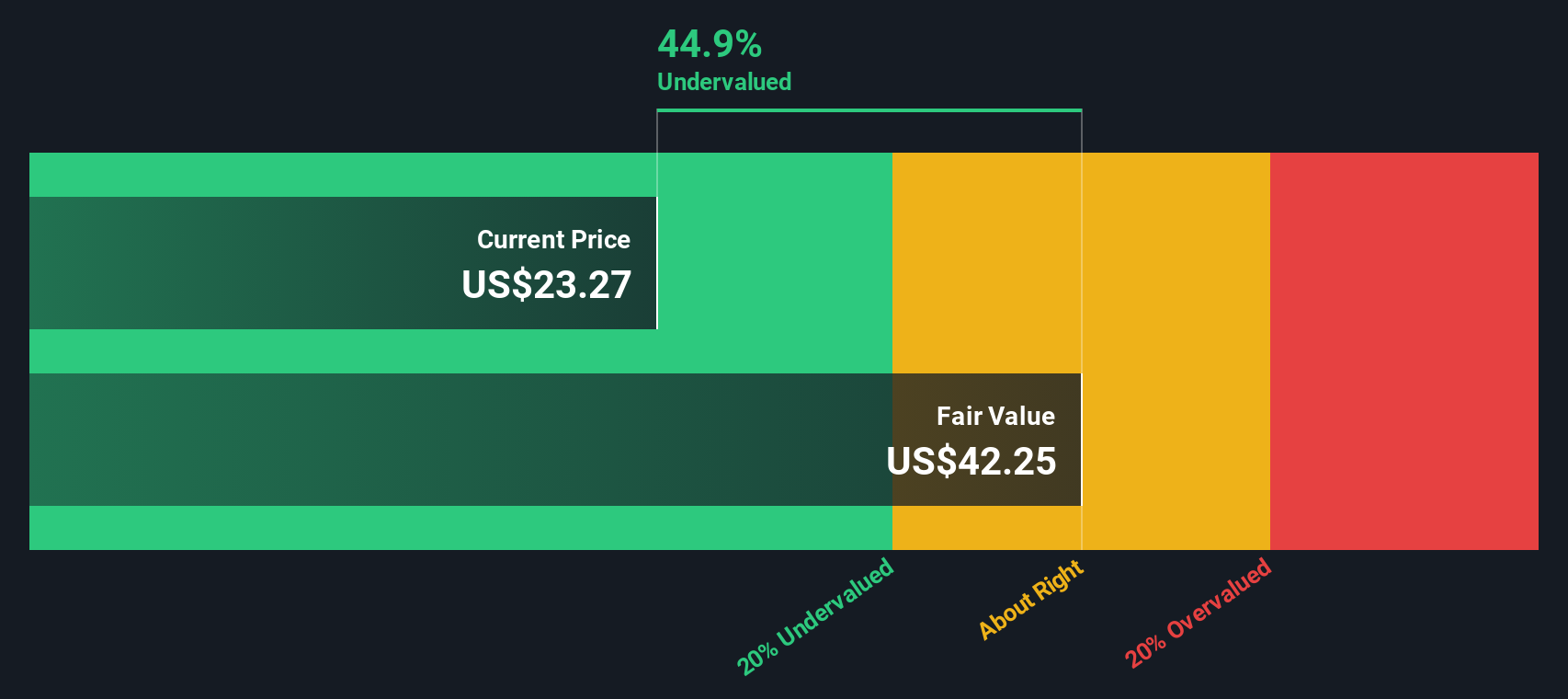

Now for the big question: is Cogent undervalued, fairly valued, or something else entirely? By our current measures, the company racks up a value score of 3 out of 6, meaning it checks the undervalued box on half the key indicators we track. There’s more than one way to judge what a stock is worth, so let’s dive deeper into the different valuation approaches. Stick around, because I’ll share an even more insightful way to look at valuation at the end of the article.

Why Cogent Communications Holdings is lagging behind its peers

Approach 1: Cogent Communications Holdings Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model is a method that estimates a company’s value by projecting its future cash flows and discounting them back to their present value. This approach aims to capture not just today’s earnings, but also how much money the business could generate in the future.

For Cogent Communications Holdings, the latest reported Free Cash Flow (FCF) stands at about -$185 Million, reflecting a recent dip. However, analysts expect a turnaround, forecasting FCF to rebound to $79 Million by 2027. Over the next ten years, projections from analysts as well as figures extrapolated by Simply Wall St suggest that FCF could steadily increase. For example, in 2026, FCF is expected to reach around $62 Million, climbing to approximately $148 Million by 2035. These numbers provide a long-term view of the company’s potential cash generation, all referenced in US Dollars ($).

Based on these projections and using the 2 Stage Free Cash Flow to Equity model, Cogent’s estimated intrinsic value per share is $52.46. This represents a 23.0% discount to the current share price, implying the stock is undervalued according to DCF analysis.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Cogent Communications Holdings is undervalued by 23.0%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

Approach 2: Cogent Communications Holdings Price vs Sales

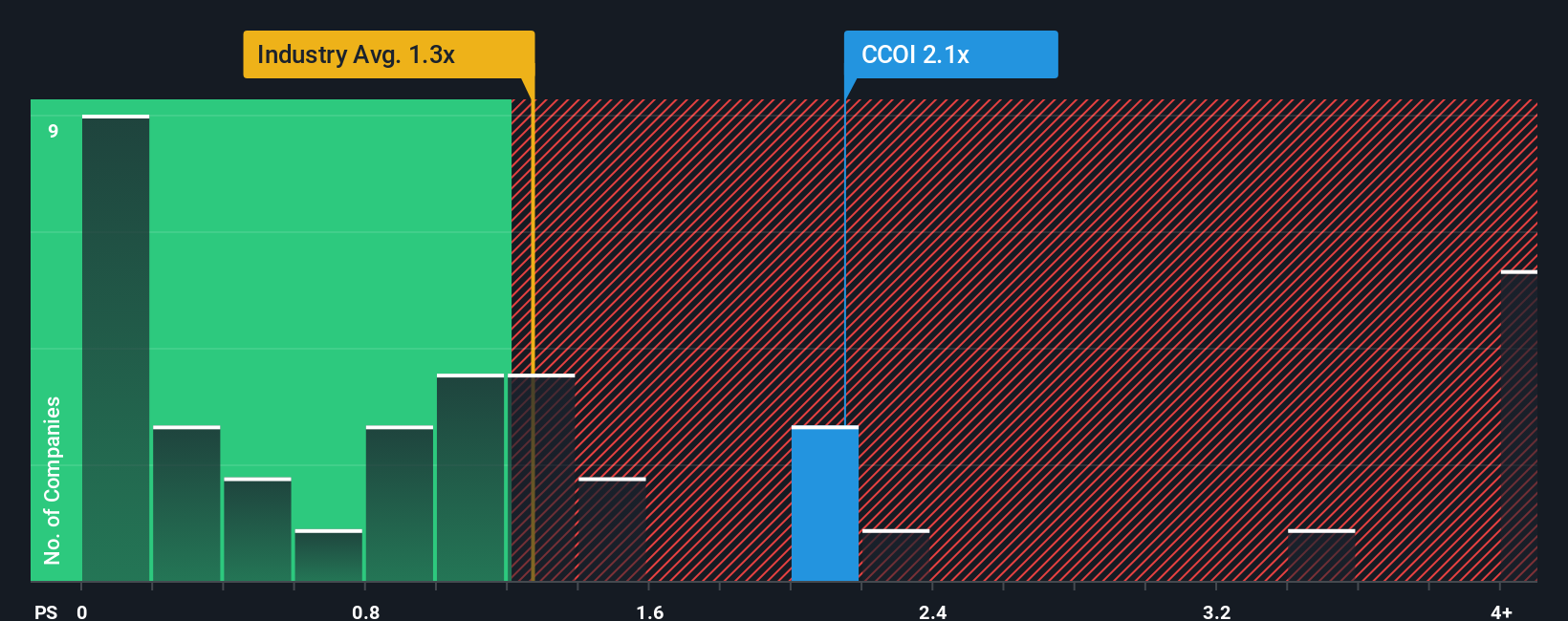

For many companies, especially those with variable or negative earnings, the Price-to-Sales (P/S) ratio is often the preferred valuation metric. This is particularly useful for businesses like Cogent Communications Holdings, where profits are volatile but revenue remains more stable and informative. The P/S ratio helps investors assess what the market is willing to pay for each dollar of sales. This is valuable for telecom businesses where recurring revenue streams are significant.

Interpretation of the P/S ratio depends on both growth prospects and risk. Higher expected revenue growth or lower perceived risk typically justifies a higher ratio. Companies facing headwinds or uncertain outlooks tend to trade at lower multiples. For Cogent Communications Holdings, the current P/S ratio is 2.08x. This figure stands higher than the telecom industry average of 1.22x but considerably lower than the average among its direct peers at 6.06x, highlighting a nuanced positioning within its sector.

Simply Wall St's proprietary "Fair Ratio" adds another layer of analysis by blending in company-specific factors such as revenue growth, profitability, margins, risk, and size. This metric offers a more tailored expectation compared to broad industry or peer averages, which can overlook unique aspects of a business. According to this calculation, Cogent's Fair Ratio is 0.91x, suggesting the stock’s current P/S is slightly above where these combined fundamentals would typically place it.

Comparing the Fair Ratio (0.91x) to Cogent's actual P/S (2.08x), the gap is greater than 0.10, which leads to a view that the share price is overvalued based on this metric.

Result: OVERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Cogent Communications Holdings Narrative

Earlier, we mentioned there is an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is your investment story, the set of assumptions and beliefs you have about Cogent Communications Holdings’s future, which link together expected revenue growth, earnings, and profit margins to arrive at your own fair value estimate.

Narratives are more than just numbers; they put your analysis into context, letting you map out the "why" behind your forecast and see how your perspective stacks up against others in the market. On Simply Wall St’s Community page, Narratives are easy to use and embraced by millions of investors, helping you sense-check your outlook with just a few clicks.

Because Narratives update dynamically when new news or earnings are released, they ensure that your investment view always reflects the latest available data. This empowers you to confidently decide whether to buy, hold, or sell, by directly comparing your Fair Value to Cogent’s current share price, all underpinned by your own assumptions and updated as new information arrives.

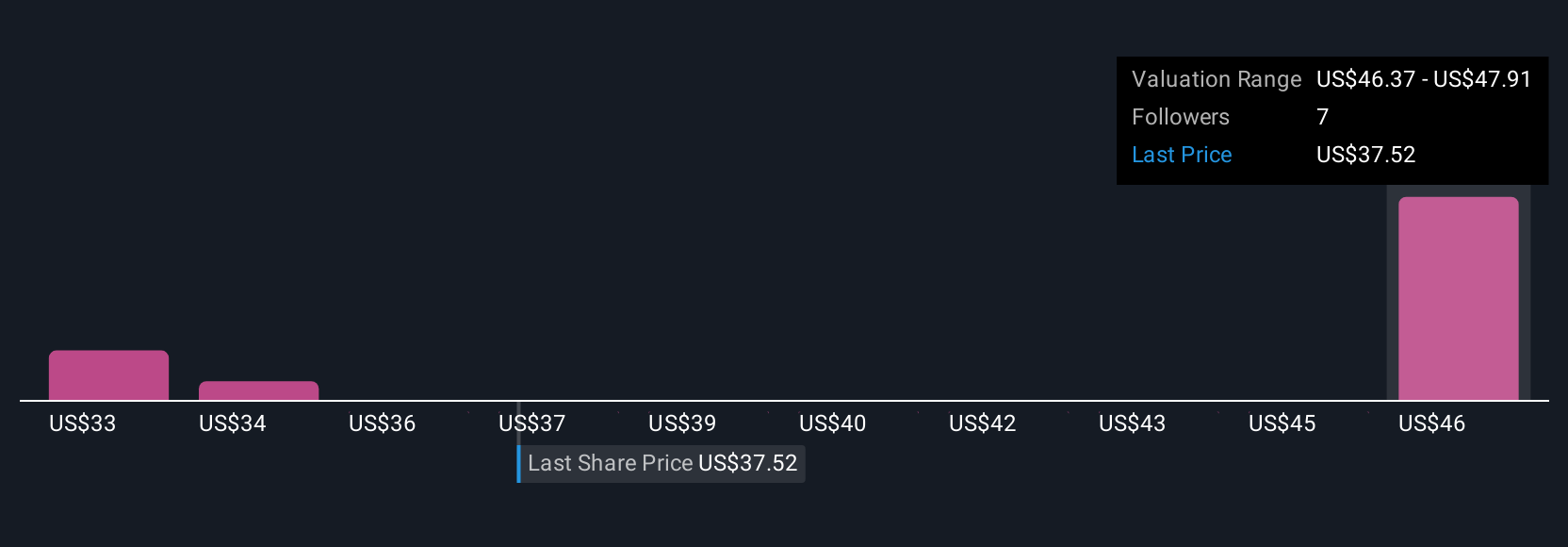

For example, a bullish investor might see massive growth potential from Cogent’s network expansion and set a fair value as high as $75, while a more cautious investor, concerned about commoditization and leverage, could justify a fair value as low as $30. Narratives highlight these differences, helping you invest with conviction based on your unique outlook.

Do you think there's more to the story for Cogent Communications Holdings? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CCOI

Cogent Communications Holdings

Through its subsidiaries, provides high-speed Internet access, private network, and data center colocation space services in North America, South America, Europe, Oceania, and Africa.

Moderate risk and good value.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Fiverr International will transform the freelance industry with AI-powered growth

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion