- United States

- /

- Communications

- /

- NasdaqCM:LTRX

Earnings Update: Lantronix, Inc. (NASDAQ:LTRX) Just Reported Its First-Quarter Results And Analysts Are Updating Their Forecasts

As you might know, Lantronix, Inc. (NASDAQ:LTRX) recently reported its first-quarter numbers. Results look to have been somewhat negative - revenue fell 2.2% short of analyst estimates at US$17m, although statutory losses were somewhat better. The per-share loss was US$0.01, 33% smaller than the analysts were expecting prior to the result. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

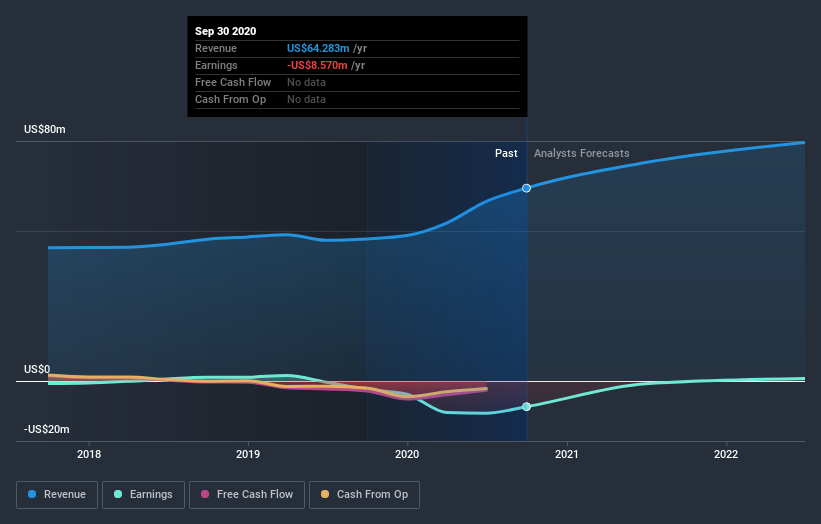

View our latest analysis for Lantronix

Following the latest results, Lantronix's three analysts are now forecasting revenues of US$72.8m in 2021. This would be a decent 13% improvement in sales compared to the last 12 months. The loss per share is expected to greatly reduce in the near future, narrowing 89% to US$0.035. Yet prior to the latest earnings, the analysts had been forecasting revenues of US$72.8m and losses of US$0.025 per share in 2021. So it's pretty clear the analysts have mixed opinions on Lantronix even after this update; although they reconfirmed their revenue numbers, it came at the cost of a per-share losses.

As a result, there was no major change to the consensus price target of US$6.17, with the analysts implicitly confirming that the business looks to be performing in line with expectations, despite higher forecast losses. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. Currently, the most bullish analyst values Lantronix at US$6.50 per share, while the most bearish prices it at US$6.00. With such a narrow range of valuations, the analysts apparently share similar views on what they think the business is worth.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Lantronix's past performance and to peers in the same industry. The analysts are definitely expecting Lantronix's growth to accelerate, with the forecast 13% growth ranking favourably alongside historical growth of 7.2% per annum over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 4.3% per year. Factoring in the forecast acceleration in revenue, it's pretty clear that Lantronix is expected to grow much faster than its industry.

The Bottom Line

The most important thing to take away is that the analysts increased their loss per share estimates for next year. Fortunately, they also reconfirmed their revenue numbers, suggesting sales are tracking in line with expectations - and our data suggests that revenues are expected to grow faster than the wider industry. The consensus price target held steady at US$6.17, with the latest estimates not enough to have an impact on their price targets.

With that in mind, we wouldn't be too quick to come to a conclusion on Lantronix. Long-term earnings power is much more important than next year's profits. We have forecasts for Lantronix going out to 2022, and you can see them free on our platform here.

Even so, be aware that Lantronix is showing 2 warning signs in our investment analysis , you should know about...

When trading Lantronix or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NasdaqCM:LTRX

Lantronix

Develops, markets, and sells industrial and enterprise internet of things (IoT) products and services in the Americas, Europe, the Middle East, Africa, and the Asia Pacific Japan.

Excellent balance sheet and overvalued.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)