- United States

- /

- Tech Hardware

- /

- NasdaqGS:IVAC

Forecast: Analysts Think Intevac, Inc.'s (NASDAQ:IVAC) Business Prospects Have Improved Drastically

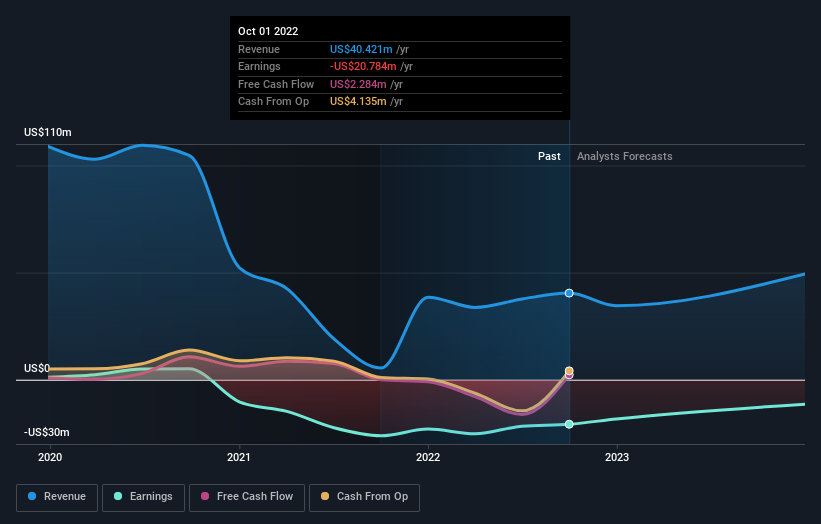

Intevac, Inc. (NASDAQ:IVAC) shareholders will have a reason to smile today, with the analysts making substantial upgrades to next year's forecasts. The consensus statutory numbers for both revenue and earnings per share (EPS) increased, with their view clearly much more bullish on the company's business prospects.

Following the upgrade, the current consensus from Intevac's twin analysts is for revenues of US$49m in 2023 which - if met - would reflect a huge 22% increase on its sales over the past 12 months. Losses are predicted to fall substantially, shrinking 45% to US$0.45. Yet prior to the latest estimates, the analysts had been forecasting revenues of US$40m and losses of US$0.63 per share in 2023. So there's been quite a change-up of views after the recent consensus updates, with the analysts making a sizeable increase to their revenue forecasts while also reducing the estimated loss as the business grows towards breakeven.

Check out our latest analysis for Intevac

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. For example, we noticed that Intevac's rate of growth is expected to accelerate meaningfully, with revenues forecast to exhibit 17% growth to the end of 2023 on an annualised basis. That is well above its historical decline of 25% a year over the past five years. Compare this against analyst estimates for the broader industry, which suggest that (in aggregate) industry revenues are expected to grow 5.7% annually. Not only are Intevac's revenues expected to improve, it seems that the analysts are also expecting it to grow faster than the wider industry.

The Bottom Line

The most important thing here is that analysts reduced their loss per share estimates for next year, reflecting increased optimism around Intevac's prospects. They also upgraded their revenue estimates for next year, and sales are expected to grow faster than the wider market. More bullish expectations could be a signal for investors to take a closer look at Intevac.

Still, the long-term prospects of the business are much more relevant than next year's earnings. At least one analyst has provided forecasts out to 2023, which can be seen for free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:IVAC

Intevac

Engages in the designing, developing, and manufacturing thin-film processing systems in the United States, Europe, and Asia.

Flawless balance sheet and slightly overvalued.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Salesforce Stock: AI-Fueled Growth Is Real — But Can Margins Stay This Strong?

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)