- United States

- /

- Electronic Equipment and Components

- /

- NasdaqGS:CGNX

Cognex (CGNX) Profit Turnaround Reinforces Bullish Narratives Despite Premium Valuation

Reviewed by Simply Wall St

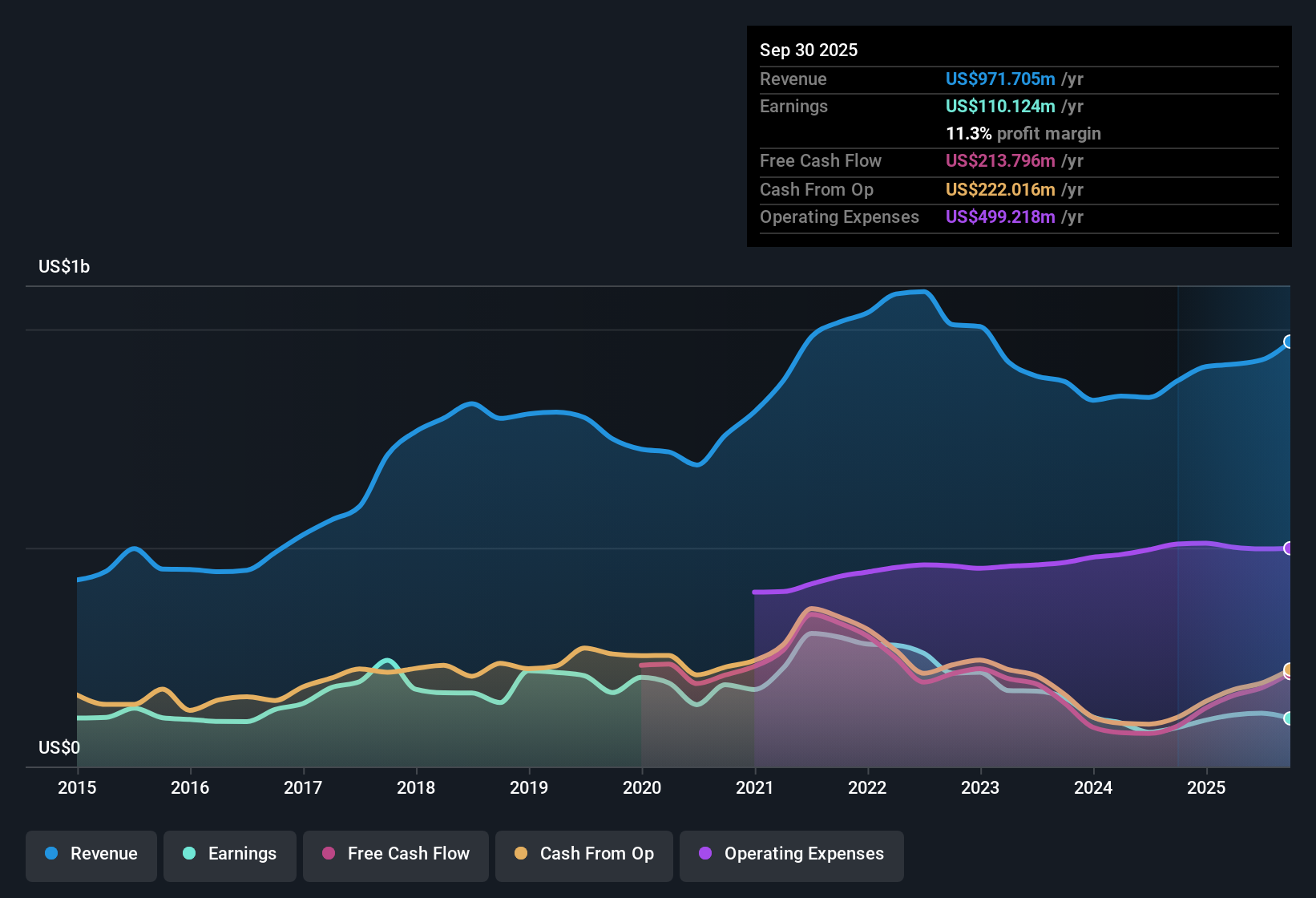

Cognex (CGNX) reversed its profit trajectory this year, with EPS up 23.8% after a prior five-year stretch of 20.4% annual declines. Net profit margin rose to 11.3%, marking notable improvement from 10.1% last year, while earnings outlook calls for a robust 23.7% annual growth, well ahead of the US market’s pace. Despite this, projected revenue growth of 8.3% is set to lag the national average, and shares, trading at $41.31, currently sit just below their estimated fair value of $42.15.

See our full analysis for Cognex.Next, let's see how these results measure up against the narratives that drive the market conversation, identifying which views are reinforced and where opinions may get challenged.

See what the community is saying about Cognex

Analyst Price Target Lags Current Growth

- Analysts expect Cognex to reach $241.2 million in earnings and $1.2 billion in revenue by 2028, assuming an annual revenue growth rate of 10.2% and a profit margin increase from 13.1% today to 19.4% over three years.

- According to the analysts' consensus view, these forecasts support a $48.25 price target. However, there is tension in the outlook:

- The current price of $41.31 is 14.4% below that target, suggesting that the growth trajectory is recognized but may not be fully reflected in the stock yet.

- Disagreement among analysts is pronounced, with the most bullish expecting $58.00 and the most bearish at $35.00. This makes it especially important to test whether the anticipated growth justifies the premium.

- The recent profit margin expansion to 11.3%, up from 10.1%, confirms tangible improvement in operating leverage. This development aligns with the consensus expectation for further margin gains in coming years.

Curious if Cognex's momentum is enough to shift the balance? Check what consensus forecasters expect next in the full company narrative. 📊 Read the full Cognex Consensus Narrative.

Margin Expansion Drives Cash Flow Upside

- The rise in net profit margin to 11.3%, with analysts predicting it will reach 19.4% within three years, signals that Cognex's cost controls and sales mix changes are materially boosting earnings quality.

- The analysts' consensus narrative argues that cost optimization and sales initiatives are generating reliable growth streams:

- EBITDA margin improvements are evidencing stronger free cash flow conversion. This both funds R&D investment and supports ongoing capital returns.

- This foundation gives stability even as recurring revenue models and new end-markets are rolled out. It confirms that operational discipline is translating into real-world financial progress.

Valuation Premium Stands Out

- Cognex trades at 63 times earnings, far above the US electronics industry average of 25.7x and the peer average of 35.1x. The share price of $41.31 sits just under the DCF fair value of $42.15.

- The analysts' consensus view highlights that to justify the 2028 price target of $48.25, Cognex would still need to be valued at 38x forward earnings, which is well above current industry norms:

- This premium only makes sense if projected margins and growth persist. This puts added pressure on management to deliver continued outperformance versus sector peers.

- The limited gap between today’s price and DCF fair value underscores that shares already reflect high expectations. As a result, future upside hinges on exceeding consensus forecasts.

Next Steps

To see how these results tie into long-term growth, risks, and valuation, check out the full range of community narratives for Cognex on Simply Wall St. Add the company to your watchlist or portfolio so you'll be alerted when the story evolves.

Wondering if the data points in a new direction? You can build your own perspective quickly and add your voice. Do it your way

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Cognex.

See What Else Is Out There

Cognex trades at a premium valuation, and its revenue growth is projected to lag the US market. This could limit future upside if forecasts are missed.

If you think steadier expansion matters most, check out stable growth stocks screener (2113 results) to compare companies delivering consistent sales and earnings gains regardless of market swings.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CGNX

Cognex

Provides machine vision products that capture and analyze visual information to automate manufacturing and distribution tasks worldwide.

Flawless balance sheet with proven track record and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)