Advertisement

- United States

- /

- Tech Hardware

- /

- NasdaqGS:AAPL

Fundamentals & Price Targets: Why Analysts Expect a Peak for Apple's (NASDAQ:AAPL) Stock

Analysis summary:

- Strong fundamentals but a possible value peak at $180 per share.

- Apple is entering a mature growth stage, and revenue growth is expected to be less than 10% going forward.

- AAPL hallmarks include a strong cash conversion with more free cash flows than earnings, large returns and a low debt level.

Apple Inc. ( NASDAQ:AAPL ) is currently a $2.7t market cap giant, which has recovered some 33% in the last two months. Considering the economic uncertainty, it can be good to reevaluate the key fundamentals for the company, and see if AAPL is close to topping out or if there is still room to grow the stock.

Check out our latest analysis for Apple

Key Fundamentals

While analyzing the fundamentals, we found some key points that make Apple a valuable company for investors. In no particular order, here is what stands out on a fundamental level.

Current Financial Performance

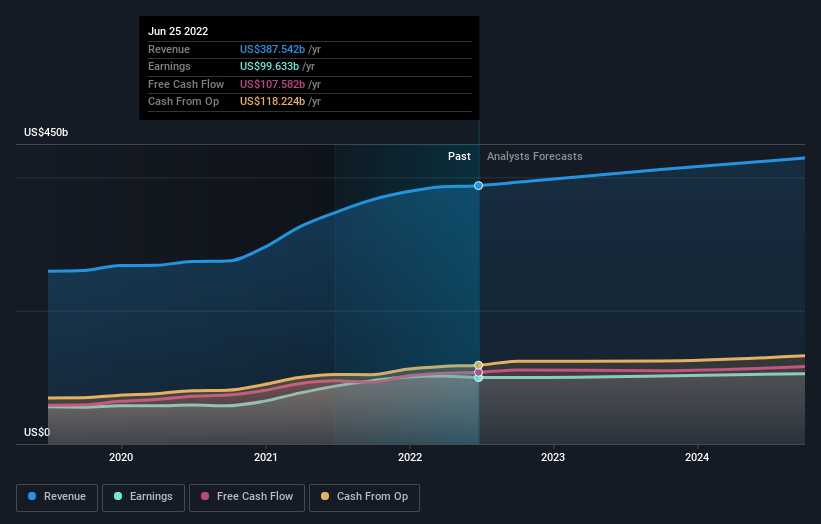

In the last 12 months, Apple has made $387.5b in revenue, and $167.9b in gross profit, putting the gross margin at 43.3%. Revenue grew 4.4% more than COGS, boosting the margins and making the company more productive at the production level.

Shifting to the bottom line, the last 12 months of earnings came in at $99.6b, striking a 25.7% net profit margin. Net margins have also grown some 2.8% from last year. On the other side of the earnings are the free cash flows attributable to investors - these came at $107.582b, even higher than the mentioned earnings. This means that the company is a great cash converter (negative accruals), which is sometimes a leading indicator of better performance.

Future Growth

The next important factor in our analysis is Apple's growth capacity. In the chart below, we can see the average estimates of analysts covering the company going to 2025:

Apple's 41 analysts estimate revenues of $411.6b in 2023, which would reflect a modest 6.2% increase in its sales over the past 12 months. Given that the CAGR in the last 5 years was 11.6% it is fair to expect growth to be lower than the historical figure as the company matures.

EPS are predicted to rise 4.0% to US$6.44, as a reflection of the estimated $102.8b in net income for FY 2022. Free cash flow is estimated to reach $113b in Q3 on a TTM basis, but analysts are expecting a relatively small drop by Q3 2023 to $109.9b.

We can see that the company is entering a sustainable growth phase, which means that they will have to continuously invest in the business and can expect single digit growth rates. Innovation and new projects, such as Apple finance and the Apple car, can supercharge this growth, but the company may not execute within expectations, so we can't count on these projects just yet.

Risk & Returns

Looking at the fundamentals, the key risk aspect to consider is the debt balance. The company has $119.7b in debt, giving it a debt to market cap of 4.3%. This is a relatively low debt to equity ratio, but the absolute value of debt is high, so management may be reluctant to take on much more leverage. The latest debt offering for Apple can be found here.

Returns are on the other side, and represent an important factor that makes the company valuable. Returns are measured against some form of company investment, whether it is equity, capital, assets or other combinations. The goal here is to see if the company is growing the bottom line, while keeping or reducing their total capital. For investors, this means that we are looking for companies that can increase profitability without making large investments in the business.

Apple is a great example of a high return company, it has a return on assets of 29.6% and a return on capital of 57.3%. We need to keep in-mind that the ROE and return on capital figures use that book value of equity as part of their calculation - this gets continuously reduced as part of the long-standing share buyback programs of Apple, so it may be best to use the return on assets as a better performance indicator - Apple is still mostly a hardware manufacturer, so hard assets are an appropriate part of their investment strategy.

What This Means For Investors

At the end of the day, we need to put all of these fundamentals into context and come up with a value for the company which helps us make better decisions regarding the stock. One way to do that is to look at analysts' price target estimates.

In the chart below, we can see how the analysts' price targets look for Apple:

We can see that analysts have settled on a $180 average price target, with a relatively low spread between estimates. This seems to be the first price target stabilization after a series of downwards revisions for Q1, 2023. It is possible that the company is hitting a short-term valuation ceiling, and analysts are cautious to keep the price targets growing before the company demonstrates that it can branch off and find new avenues for growth.

Alternatively, you can use our intrinsic valuation model to see the value of the future ash flows of Apple and combine both methods to form a better picture of the value of the stock.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Goran Damchevski and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Goran Damchevski

Goran is an Equity Analyst and Writer at Simply Wall St with over 5 years of experience in financial analysis and company research. Goran previously worked in a seed-stage startup as a capital markets research analyst and product lead and developed a financial data platform for equity investors.

About NasdaqGS:AAPL

Apple

Designs, manufactures, and markets smartphones, personal computers, tablets, wearables, and accessories worldwide.

Limited growth with questionable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.1% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|11.6% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|39.4% undervalued

TR

Community Contributor