- United States

- /

- Software

- /

- NYSE:YEXT

Does Recent Price Volatility Create an Opportunity in Yext in 2025?

Reviewed by Bailey Pemberton

- Wondering if Yext is actually a bargain or just another volatile tech name? You are not alone, and that is exactly what we are going to unpack here.

- The stock is up a solid 27.8% over the last year despite a -6.3% slip in the past week and a -4.3% dip over the last month, which hints that sentiment is still cautiously optimistic after a tough 5 year stretch of -47.8%.

- Recently, Yext has stayed in the conversation as investors reassess digital search and AI driven marketing tools, especially as businesses look for more measurable returns from their software spend. That renewed focus on efficient, outcome based software has put companies like Yext back on watchlists and helps explain the stronger year to date move of 27.1%.

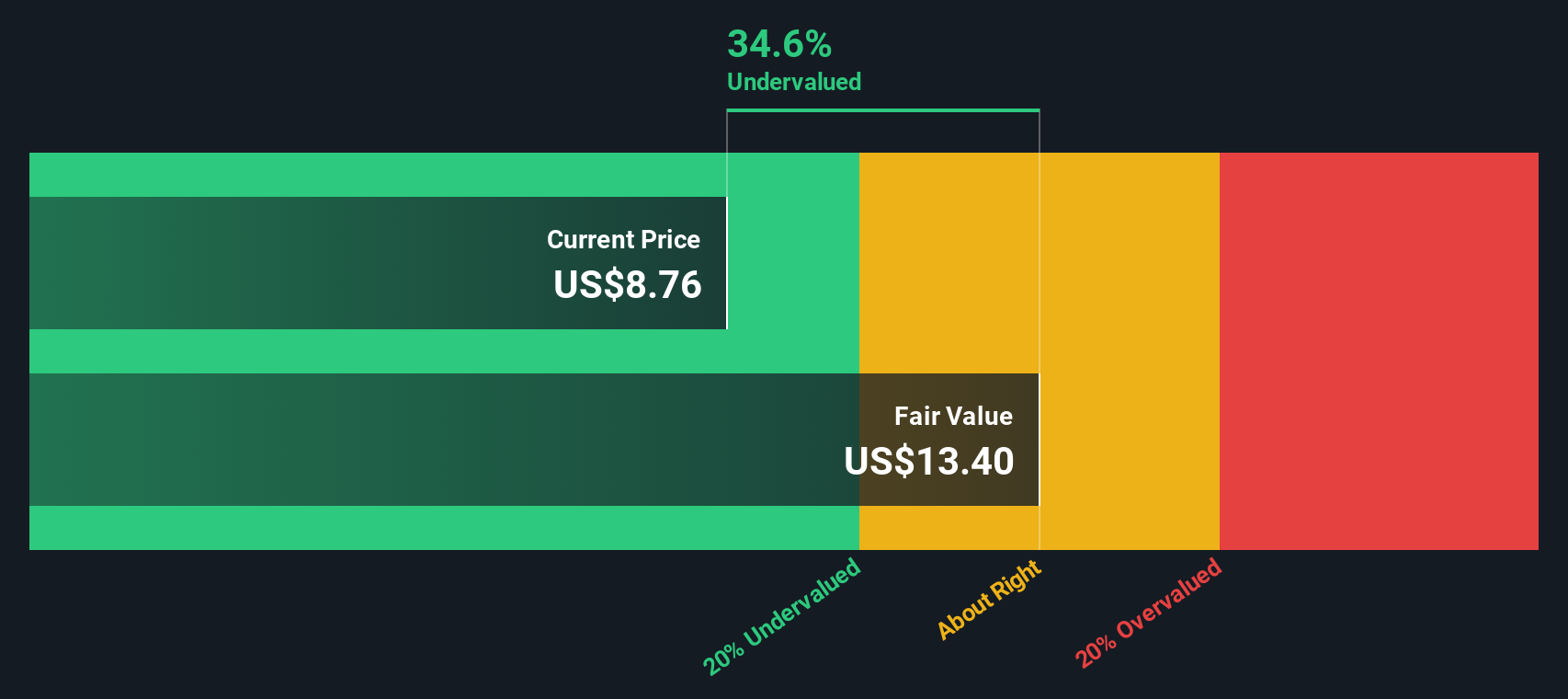

- On our checklist of 6 valuation tests, Yext currently scores just 2/6 for being undervalued, which suggests the market might be only partially pricing in its fundamentals. Next, we will walk through different valuation approaches to see what the numbers really say, then finish with a more holistic way to think about Yext's true worth beyond any single model.

Yext scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Yext Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business is worth by projecting the cash it can generate in the future and discounting those cash flows back to today. For Yext, the latest twelve month Free Cash Flow stands at about $62.1 Million, and analysts, combined with Simply Wall St extrapolations, see this rising to roughly $112.3 Million by 2035, with $101 Million expected around 2030.

Using a 2 Stage Free Cash Flow to Equity model, these annual cash flow projections are discounted to reflect risk and the time value of money. Summing those discounted values and dividing by the number of shares leads to an estimated intrinsic value of about $12.28 per share. Compared with the current market price, this implies the stock trades at roughly a 32.3% discount, indicating investors may not be fully pricing in Yext future cash generation.

This analysis suggests that Yext appears meaningfully undervalued on a pure cash flow basis, assuming the growth path and discount rate prove broadly accurate.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Yext is undervalued by 32.3%. Track this in your watchlist or portfolio, or discover 903 more undervalued stocks based on cash flows.

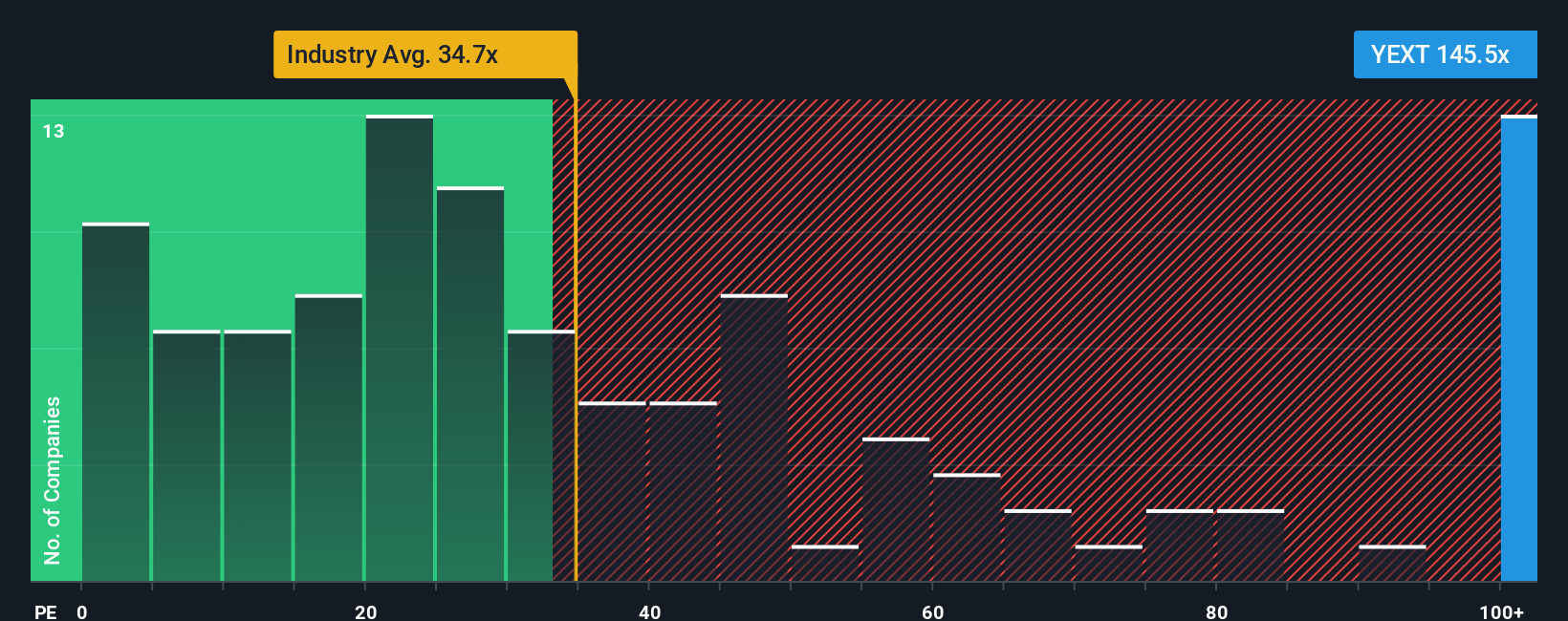

Approach 2: Yext Price vs Earnings

For companies that are generating consistent profits, the price to earnings, or PE, ratio is a useful way to gauge how much investors are willing to pay today for each dollar of current earnings. A higher PE typically reflects stronger growth expectations or lower perceived risk, while a lower PE can signal slower growth, more uncertainty, or simply that the market is overlooking the business.

Yext currently trades at around 38.63x earnings, which is above both the broader Software industry average of about 32.92x and the peer group average of roughly 25.02x. On the surface, that might suggest the stock is a bit expensive compared with similar names.

Simply Wall St also calculates a Fair Ratio, a proprietary estimate of what Yext PE should be given its specific earnings growth outlook, margins, risk profile, industry and market cap. For Yext, this Fair Ratio is about 27.65x. Because it is tailored to the company fundamentals rather than broad group averages, this measure offers a more nuanced benchmark. Comparing Yext current PE of 38.63x to the Fair Ratio of 27.65x indicates that the shares are trading at a premium that appears meaningfully stretched on earnings alone.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1443 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Yext Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, which are simply the stories investors tell about a company, backed up by their own assumptions for future revenue, earnings, margins and fair value. A Narrative on Simply Wall St connects three things: what you believe about the business, how that belief translates into a financial forecast, and ultimately what you think a fair price per share should be today. Narratives live in the Community page of the platform, where millions of investors share and compare their views using the same simple framework, so it is very easy to see how different stories lead to different values. Once you have a Narrative, deciding when to buy or sell becomes clearer; you just compare your Fair Value to the current market Price and act when the gap is big enough for your risk tolerance. Because Narratives are updated as new data, news and earnings arrive, your story and valuation can evolve instead of staying frozen. For Yext, for example, the most optimistic Narrative on the platform might see a fair value near $10.00 while the most cautious sits closer to $8.25, reflecting different expectations about AI driven growth, margins and competitive risk.

Do you think there's more to the story for Yext? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:YEXT

Yext

Provides a platform that offers answers to consumer questions in North America and internationally.

Excellent balance sheet and slightly overvalued.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)