Advertisement

- United States

- /

- Software

- /

- NYSE:XZO

Exzeo Group (XZO) Q3: Net Margin Surges to 33.8%, Testing Overvaluation Concerns

Simply Wall St

Reviewed by Simply Wall St

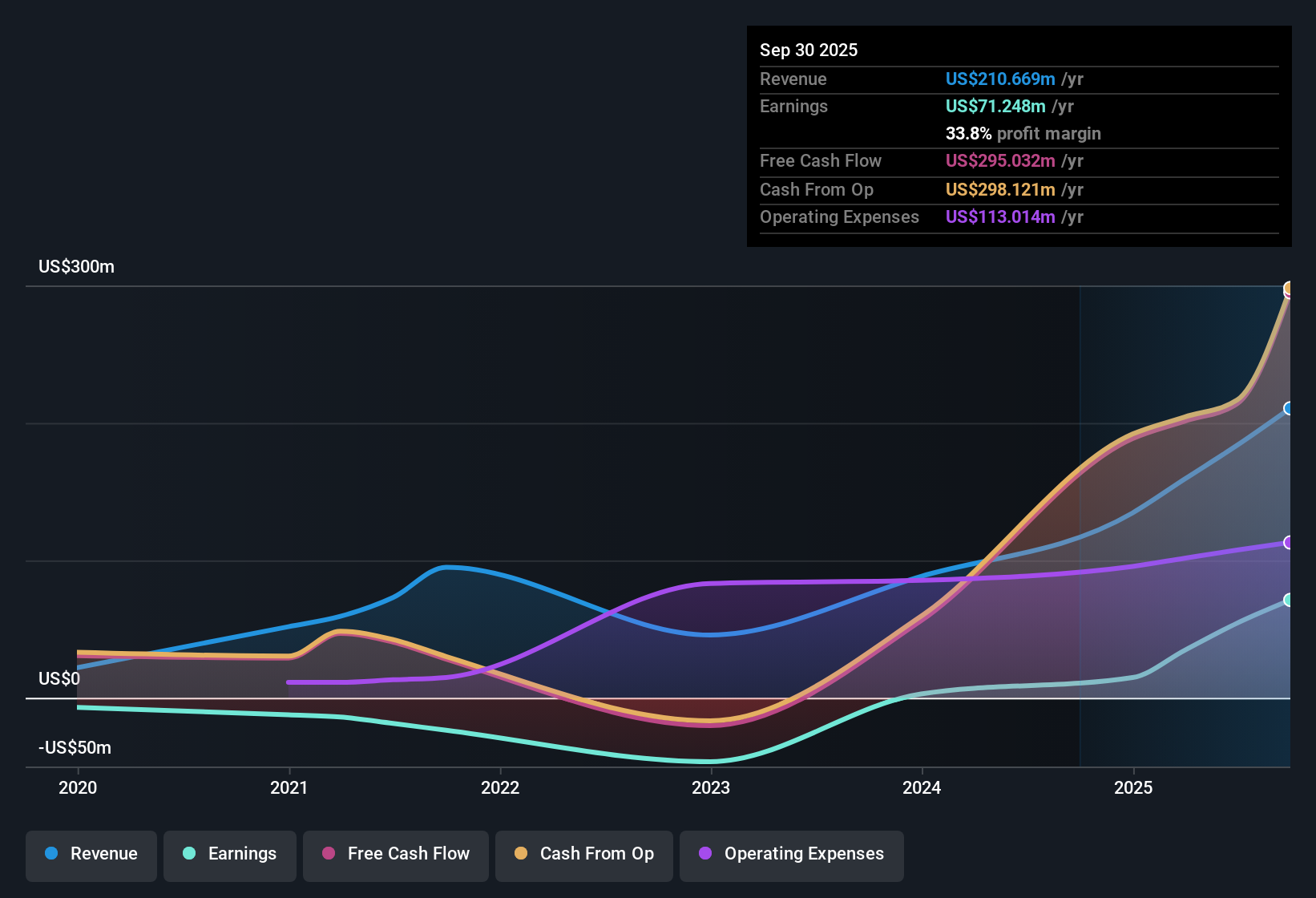

Exzeo Group (XZO) just posted Q3 2025 results with revenue of about $56.3 million, basic EPS of $0.25 and net income of roughly $21.2 million, marking another solid quarterly print. The company has seen revenue climb from $29.3 million in Q3 2024 to $56.3 million in Q3 2025, while basic EPS moved from $0.06 to $0.25 over the same period. This sets up a story of scaling profits and expanding margins that investors will be keen to track.

See our full analysis for Exzeo Group.With the latest numbers on the table, the next step is to compare this performance with the leading narratives around Exzeo Group to see which views hold up and which may need to be reconsidered.

Curious how numbers become stories that shape markets? Explore Community Narratives

Margins Strengthen With 33.8% Net Profit

- On a trailing 12 month basis, Exzeo turned $210.7 million of revenue into $71.2 million of net income, giving a 33.8% net profit margin compared with 9.5% last year.

- What stands out for a bullish view is how this profitability aligns with the growth story, with earnings up 507.9% year over year and a 5 year earnings CAGR of 53.9%, which heavily supports the idea that Exzeo is not just growing its top line but steadily converting that growth into bottom line gains.

- Supporters can point to revenue rising from $88.4 million in 2023 to $210.7 million on the latest trailing 12 month cut as evidence that scale is kicking in alongside better margins.

- At the quarterly level, net income moving from $5.3 million in Q3 2024 to $21.2 million in Q3 2025 suggests that these stronger margins are visible even when you zoom in on a single period.

P/E Looks Modest Versus Peers

- Exzeo trades at about 25.4 times trailing earnings, which is below the US Software industry average of 31.9 times and the peer average of 39.3 times, even though its earnings are forecast to grow around 19.5% per year and revenue about 12.6% per year.

- Consistent with a bullish angle that focuses on relative value, this mix of faster than market growth and a lower than peer P/E multiple suggests the stock is being priced more conservatively than many software names with weaker growth, even though the data points to stronger earnings momentum.

- Forecast earnings growth of 19.5% per year versus a US market forecast of 16.3% supports the idea that Exzeo is not just growing, but outpacing the broader market while still carrying a discount to typical software valuations.

- With revenue expected to grow 12.6% per year against a 10.7% market forecast, investors who focus on both top line and bottom line trajectories may see the current multiple as leaving room for the market to re rate if execution continues.

Price Stretches Above DCF Fair Value

- While the shares change hands at $19.94, the cited DCF fair value is $10.27, so the market price stands at roughly double the DCF based estimate even as profitability and growth metrics score well.

- From a more cautious, bearish leaning perspective, this gap between price and DCF fair value, combined with highly illiquid trading over the past three months, raises the possibility that solid fundamentals are already more than reflected in the stock and that execution risk in trading could amplify any pullbacks.

- Skeptics can argue that even with a 33.8% net margin and a 5 year earnings CAGR of 53.9%, paying almost twice the DCF fair value may leave little margin of safety if growth or margins slow from recent highs.

- Because shares are described as highly illiquid, any shift in sentiment around the 19.5% earnings growth forecast or the 12.6% revenue growth outlook could lead to sharper price swings than the fundamentals alone would suggest.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Exzeo Group's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

Explore Alternatives

Despite robust growth and expanding margins, Exzeo looks richly priced versus its DCF fair value, with illiquidity amplifying the risk of sharp downside moves.

If valuation risk and potential volatility make you uneasy, use our these 907 undervalued stocks based on cash flows to quickly focus on companies where prices still lag fundamentals and offer a wider safety margin.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Exzeo Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:XZO

Exzeo Group

Provides turnkey insurance technology and operations solutions to insurance carriers and agents.

Outstanding track record with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4034.1% undervalued

19 followersusers have followed this narrative

1 commentusers have commented on this narrative

5 likesusers have liked this narrative

DO

Double_Bubbler on Vertical Aerospace ·

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Fair Value:US$6089.9% undervalued

22 followersusers have followed this narrative

2 commentsusers have commented on this narrative

17 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8149.0% undervalued

42 followersusers have followed this narrative

3 commentsusers have commented on this narrative

8 likesusers have liked this narrative

Recently Updated Narratives

KI

KiwiInvest on Rocket Lab ·

Rocket Lab USA Will Ignite a 30% Revenue Growth Journey

Fair Value:US$97.8335.1% undervalued

136 followersusers have followed this narrative

8 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MH

mhbb on Mastersystem Infotama ·

Mastersystem Infotama will achieve 18.9% revenue growth as fair value hits IDR1,650

Fair Value:Rp1.63k13.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Procter & Gamble ·

Insiders Sell, Investors Watch: What’s Going On at PG?

Fair Value:US$1506.2% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

119 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.7% undervalued

963 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8683.3% undervalued

77 followersusers have followed this narrative

8 commentsusers have commented on this narrative

21 likesusers have liked this narrative

Trending Discussion

OI

OilStates on Oil States International ·

The article’s takeaways do not reflect Oil States’ current business mix or market realities. Nearly 75% of Company revenues now come from offshore and international projects, where industry investment is strengthening, not declining, and backlog is at the highest level in a decade. Oil States has intentionally exited lower-margin U.S. land markets, resulting in expanding margins, strong free cash flow, and a near-zero net-debt profile. Our offerings are concentrated in high-barrier, engineered offshore technologies where competitive pressure and regulatory risk are far lower than implied. These fundamentals therefore do not align with the structural-decline narrative presented. Find out more about the strong offshore/international, cash generation, and valuation upside potential in our latest investor presentation available here: https://ir.oilstatesintl.com/events-and-presentations/default.aspx

0

|0