- United States

- /

- Software

- /

- NYSE:CRM

Is Salesforce Now Attractively Priced After AI Push And Recent Share Price Rebound?

Reviewed by Bailey Pemberton

- If you have been wondering whether Salesforce is still a buy at today’s price, you are not alone. This breakdown is designed to help you decide if the current tag makes sense or not.

- After a bumpy ride this year, with the stock still down 20.1% year to date and 25.1% over the last year, the recent 10.7% jump in the past week and 9.3% gain over the last month hints that sentiment around its long term growth story might be turning.

- Part of that shift has been driven by ongoing headlines about Salesforce doubling down on AI powered CRM tools and expanding its Data Cloud platform, moves that investors see as a way to deepen its moat against rivals like Microsoft and Oracle. At the same time, coverage around activist investor interest and continued acquisitions in niche software segments has reminded the market that Salesforce is still actively reshaping its business mix for profitable growth.

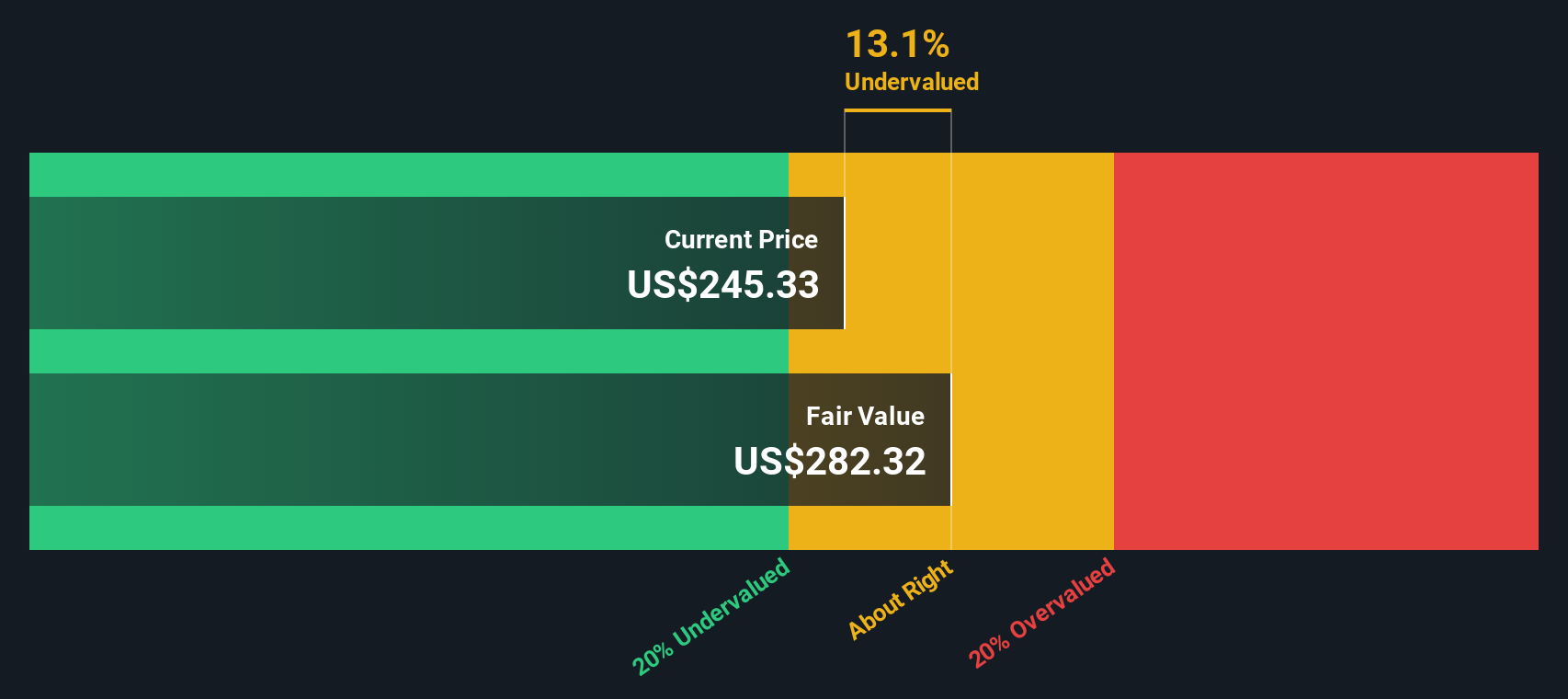

- On our checklist based valuation framework, Salesforce earns a 4/6 valuation score, suggesting it screens as undervalued on most but not all measures. Next, we will unpack those methods, then finish by exploring an even more intuitive way to think about what the stock is really worth.

Find out why Salesforce's -25.1% return over the last year is lagging behind its peers.

Approach 1: Salesforce Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth by projecting the cash it can generate in the future, then discounting those cash flows back to today in dollar terms. For Salesforce, the model starts from last twelve months Free Cash Flow of about $12.8 billion and then applies analyst forecasts, followed by more conservative long term assumptions.

Analysts see Salesforce’s annual Free Cash Flow rising into the mid to high teens over the next decade, with projections reaching roughly $19.7 billion by 2030. Beyond the first few years, Simply Wall St extrapolates those estimates using a 2 Stage Free Cash Flow to Equity approach, which tapers growth as the business matures.

On this basis, the DCF model arrives at an intrinsic value of around $358 per share. Compared with the current market price, that implies Salesforce is trading at a 26.2% discount, suggesting the stock screens as meaningfully undervalued on cash flow fundamentals.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Salesforce is undervalued by 26.2%. Track this in your watchlist or portfolio, or discover 907 more undervalued stocks based on cash flows.

Approach 2: Salesforce Price vs Earnings

For a consistently profitable business like Salesforce, the price to earnings ratio is a practical way to judge valuation because it links what investors pay directly to the profits the company generates today.

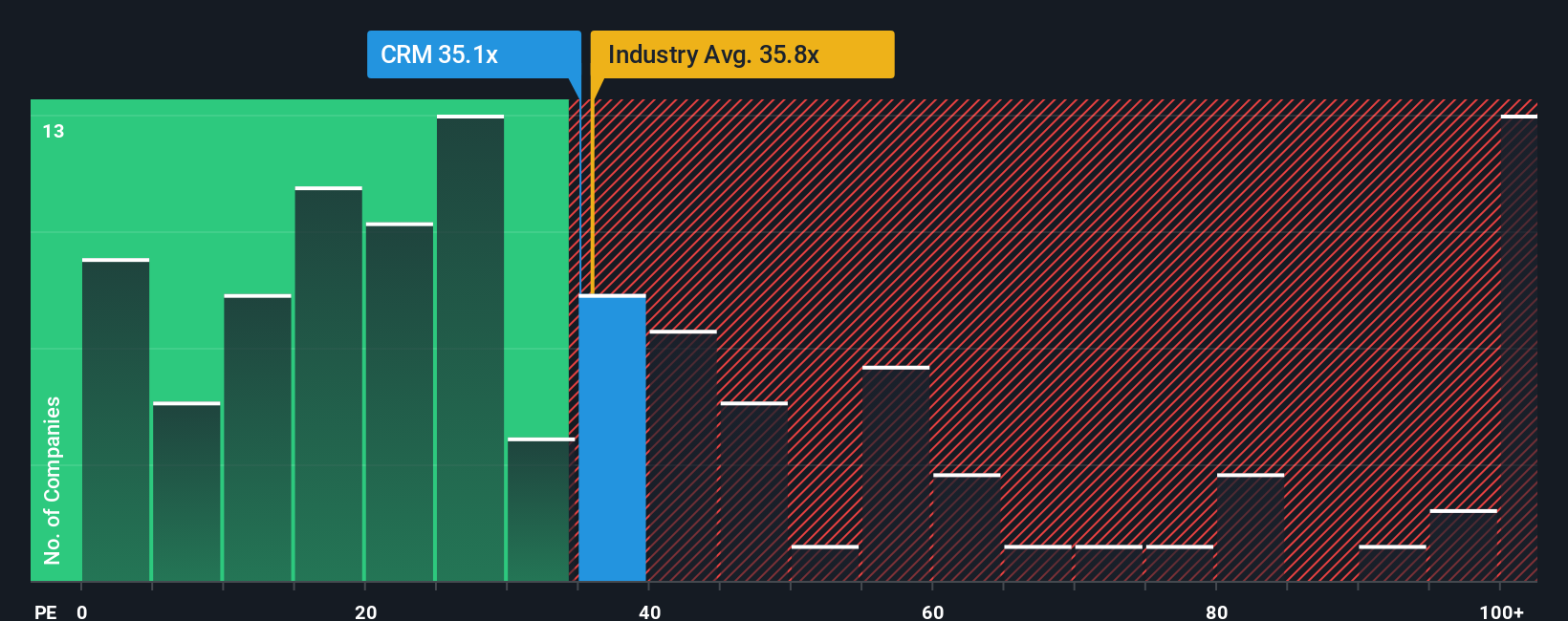

What counts as a fair PE depends on how fast earnings are expected to grow and how risky those earnings are. Higher growth and stronger competitive positions usually justify a higher multiple, while more cyclical or uncertain businesses tend to trade on lower ratios. Salesforce currently trades on about 34.3x earnings, a premium to the broader Software industry average of roughly 31.9x, but at a discount to its peer group, which averages around 56.2x.

Simply Wall St’s Fair Ratio of 40.7x is a proprietary estimate of what PE Salesforce should trade on, given its earnings growth outlook, profitability, industry, size and risk profile. This tailored benchmark is more informative than a simple industry or peer comparison because it adjusts for Salesforce’s specific strengths and risks rather than assuming one size fits all. With the shares on 34.3x compared with a Fair Ratio of 40.7x, the stock appears attractively priced on an earnings basis.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1446 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Salesforce Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple framework on Simply Wall St’s Community page where you connect your view of Salesforce’s story to concrete assumptions about its future revenue, earnings and margins, turn those into a Fair Value, and then compare that Fair Value with today’s share price to decide whether to buy, hold or sell.

In practice, a Narrative is your own scenario for how the business evolves. The platform translates that story into a full financial forecast that automatically updates as fresh news, earnings and guidance come in, so your Fair Value is always anchored to the latest information rather than a static model.

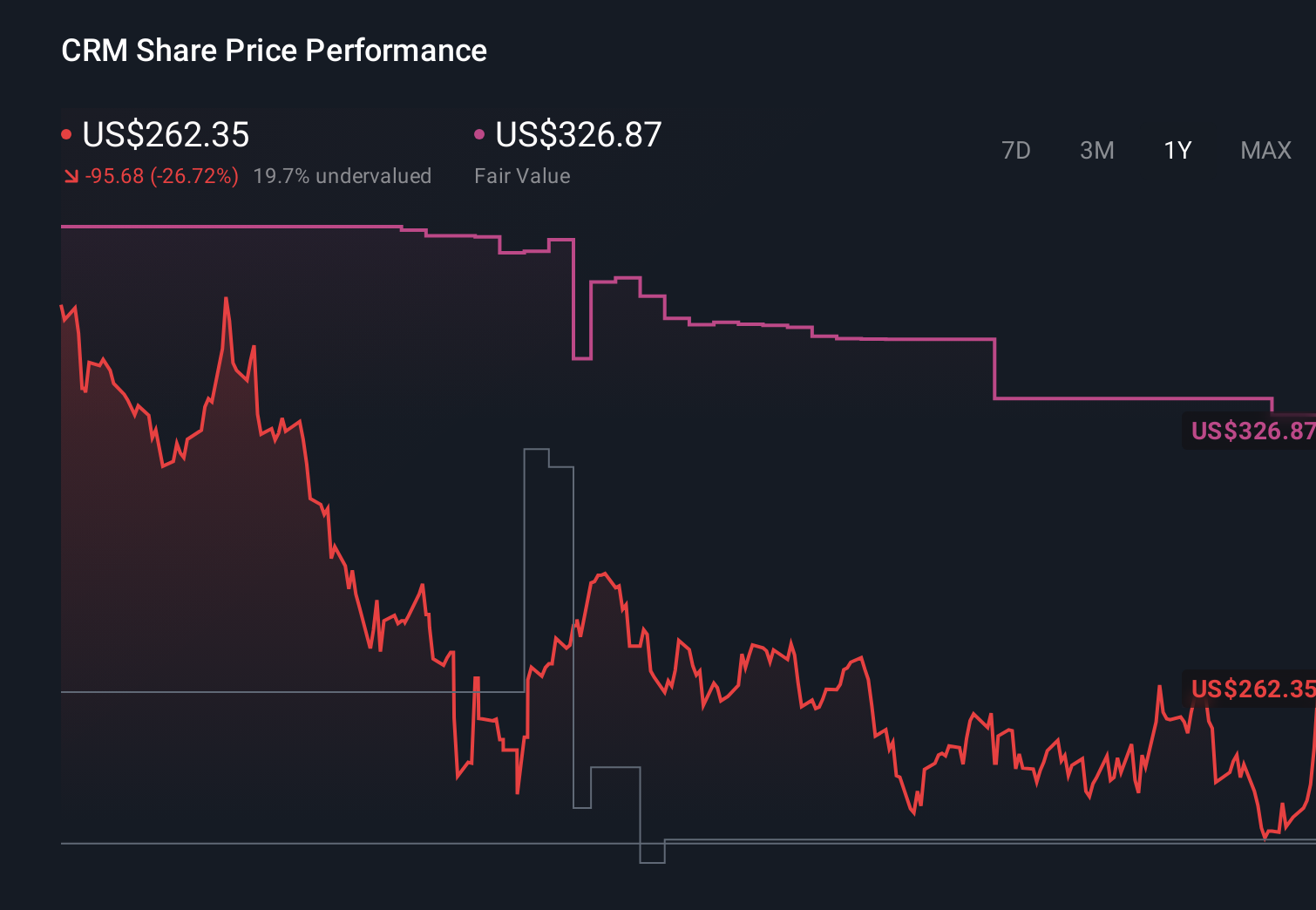

For example, one Salesforce Narrative on Simply Wall St might assume strong AI adoption, margin expansion and a Fair Value around $327 per share. A more cautious Narrative might assume slower growth, some competitive pressure and a Fair Value closer to $224 or even $201. This illustrates how two investors can look at the same company, plug in different but reasonable expectations, and arrive at very different conclusions about whether the current price offers enough upside.

For Salesforce, however, we will make it really easy for you with previews of two leading Salesforce Narratives:

Fair value: $326.87 per share

Implied undervaluation vs current price: 19.2%

Revenue growth assumption: 9.65%

- AI driven automation, Data Cloud adoption and agent based tools deepen customer lock in and support structurally higher revenue and margin growth over time.

- Expanding success with mid market and SMB customers, combined with disciplined capital returns and buybacks, is expected to drive scalable profitability per share.

- While competition, regulation and M and A integration pose risks, the narrative assumes Salesforce can manage these headwinds and still compound earnings meaningfully.

Fair value: $223.99 per share

Implied overvaluation vs current price: 18.0%

Revenue growth assumption: 13.0%

- Salesforce is seen as a strong enterprise leader, but the narrative argues the market is overestimating long run growth and free cash flow potential relative to a maturing, competitive CRM landscape.

- High dependence on large enterprise customers, renewed acquisition spending, and eventual pressure on pricing and margins from specialized CRMs and broadly available AI are key concerns.

- Even assuming solid revenue growth and 20% net margins by 2029, the analyst applies a lower 21x earnings multiple, concluding the current share price bakes in too much optimism.

Do you think there's more to the story for Salesforce? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CRM

Salesforce

Provides customer relationship management technology that connects companies and customers together worldwide.

Good value with adequate balance sheet.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Unicycive Therapeutics (Nasdaq: UNCY) – Preparing for a Second Shot at Bringing a New Kidney Treatment to Market (TEST)

Rocket Lab USA Will Ignite a 30% Revenue Growth Journey

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Trending Discussion