- United States

- /

- Software

- /

- NYSE:BOX

Box (BOX) Unveils AI Innovations With Box Automate And Box Shield Pro

Reviewed by Simply Wall St

Box (BOX) recently introduced innovative AI-driven products, enhancing its market offerings such as Box Extract and Box Automate. These product releases highlight the company's commitment to improving data handling and workflow automation for enterprise clients. Over the past month, the company's stock noted a 5% rise, aligning well with the broader market trends, which saw indices hitting record highs amid optimism over potential interest rate cuts. These announcements added momentum to Box's performance, complementing the positive market sentiment driven by stable consumer inflation expectations and macroeconomic data.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

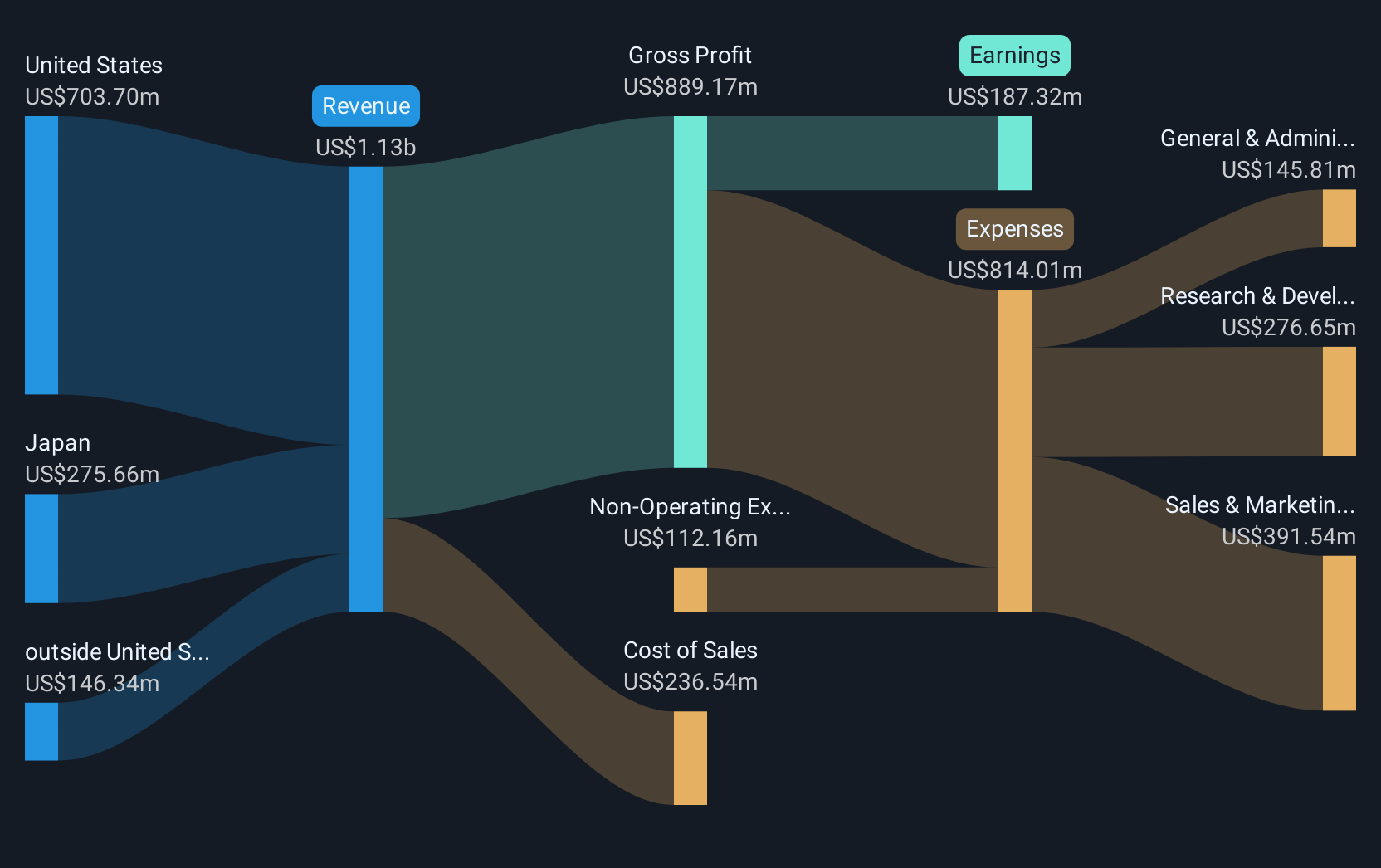

The recent introduction of AI-driven products, such as Box Extract and Box Automate, aligns well with Box’s push for innovation in AI-powered content management, potentially enhancing revenue growth by increasing customer adoption and premium pricing capability. This strategic move is set to strengthen Box's market position by addressing growing digital transformation and compliance demands. However, the company's stock performance over the longer term has been mixed. While Box shares have risen by 81.16% over the past five years, they underperformed the US Software industry, which returned 27.3% over the past year.

Despite this, analysts are optimistic, with consensus price targets suggesting a potential upside in Box’s valuation. The current share price of $32.70 remains below the consensus price target of $37.50, indicating a 14.68% discount. The impact of these recent product launches could contribute to attaining these targets by enhancing future revenue and earnings forecasts. However, as Box navigates challenges such as regulatory demands and competitive pricing pressures, its ability to meet these expectations will be crucial in realizing sustained total shareholder returns in the future. As always, investors should assess these forecasts against their own insights and assumptions about Box's market trajectory.

Examine Box's earnings growth report to understand how analysts expect it to perform.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Box might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BOX

Box

Provides a cloud content management platform that enables organizations of various sizes to manage and share their content from anywhere on any device in the United States and Japan.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Hitit Bilgisayar Hizmetleri will achieve a 19.7% revenue boost in the next five years

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)