Advertisement

- United States

- /

- Software

- /

- NasdaqGS:WDAY

How Workday’s (WDAY) Raised Guidance and New Integrations Are Shaping Its Investment Narrative

Simply Wall St

Reviewed by Simply Wall St

- In the past week, Workday reported second-quarter results with revenue of US$2.35 billion and net income of US$228 million, announced new wellness-focused partnerships with Benepass and New York Life Group Benefit Solutions, and revealed deeper integration with Zuora for financial management automation.

- These developments highlight Workday's momentum in expanding its client ecosystem and leveraging AI-enabled integrations to enhance administrative efficiency and customer value across HR and finance workflows.

- We'll examine how Workday's raised revenue guidance and major partner integrations shape its long-term investment narrative.

We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Workday Investment Narrative Recap

To be a Workday shareholder, you need to believe that accelerating enterprise adoption of cloud-native and AI-driven HR and finance platforms will sustain Workday's market position, drive steady subscription revenue, and increase product stickiness, despite new disruptive entrants or shifting customer preferences. This week's expanded partnerships and raised revenue guidance reinforce execution on these themes, but do not materially alter the biggest near-term risk: intensifying competition from both AI startups and larger software incumbents in the core international and SME markets.

Among the latest developments, the expanded partnership and integration between Workday and Zuora stands out. This collaboration directly addresses Workday's ongoing catalyst around broader adoption of its financial management platform by offering automation and unified processes for complex B2C billing and revenue management needs, thus making Workday more attractive to enterprise clients looking to modernize financial operations.

However, it is worth noting that, despite expanding integrations, ongoing pressure on pricing power from new AI-powered SaaS entrants remains a concern that investors should be aware of if...

Read the full narrative on Workday (it's free!)

Workday's outlook anticipates $12.9 billion in revenue and $2.0 billion in earnings by 2028. This is based on a 13.0% annual revenue growth rate and a substantial increase in earnings of $1.4 billion from today's $583.0 million.

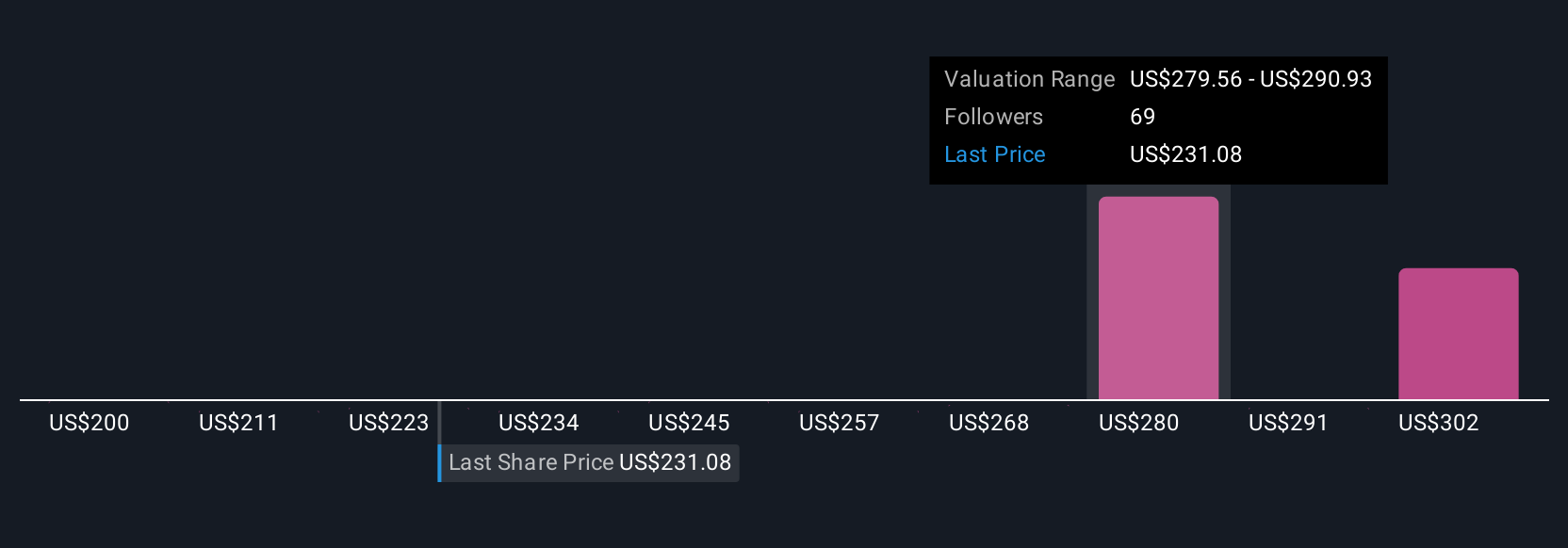

Uncover how Workday's forecasts yield a $280.19 fair value, a 22% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members provided 12 fair value estimates for Workday, ranging from US$200 to over US$311 per share. While opinions vary, many participants will be weighing Workday’s future success in capturing the growing demand for AI-enabled enterprise platforms, inviting you to consider the different views on where the opportunity and risks may lead.

Explore 12 other fair value estimates on Workday - why the stock might be worth as much as 36% more than the current price!

Build Your Own Workday Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Workday research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Workday research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Workday's overall financial health at a glance.

Ready For A Different Approach?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- AI is about to change healthcare. These 29 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 24 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Workday might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:WDAY

Workday

Provides enterprise cloud applications in the United States and internationally.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|75.8% undervalued

JO

Community Contributor

PayPal's Future Growth Through Venmo and Merchant Solutions

Fair Value US$105.25|34.2% undervalued

ZW

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$26.54|9.7% overvalued

BL

Community Contributor