- United States

- /

- Software

- /

- NasdaqGS:TEAM

Is Atlassian Offering an Opportunity After a 41.5% Share Price Slide?

Reviewed by Bailey Pemberton

- If you are wondering whether Atlassian is a bargain or a value trap at today’s price, you are not alone. This breakdown is designed to help you decide with greater confidence.

- The stock has bounced about 4.3% over the last week and 3.6% in the past month, but it is still down roughly 32.6% year to date and 41.5% over the last year. That combination often signals either deep value or lingering risk.

- Those moves have come as investors weigh Atlassian’s ongoing push to scale its cloud platform and expand its product ecosystem, including collaboration tools that aim to cement it as critical infrastructure for software teams. At the same time, sentiment has been shaped by broader rotation in and out of growth software names, which has amplified every shift in expectations around long term demand for Atlassian’s offerings.

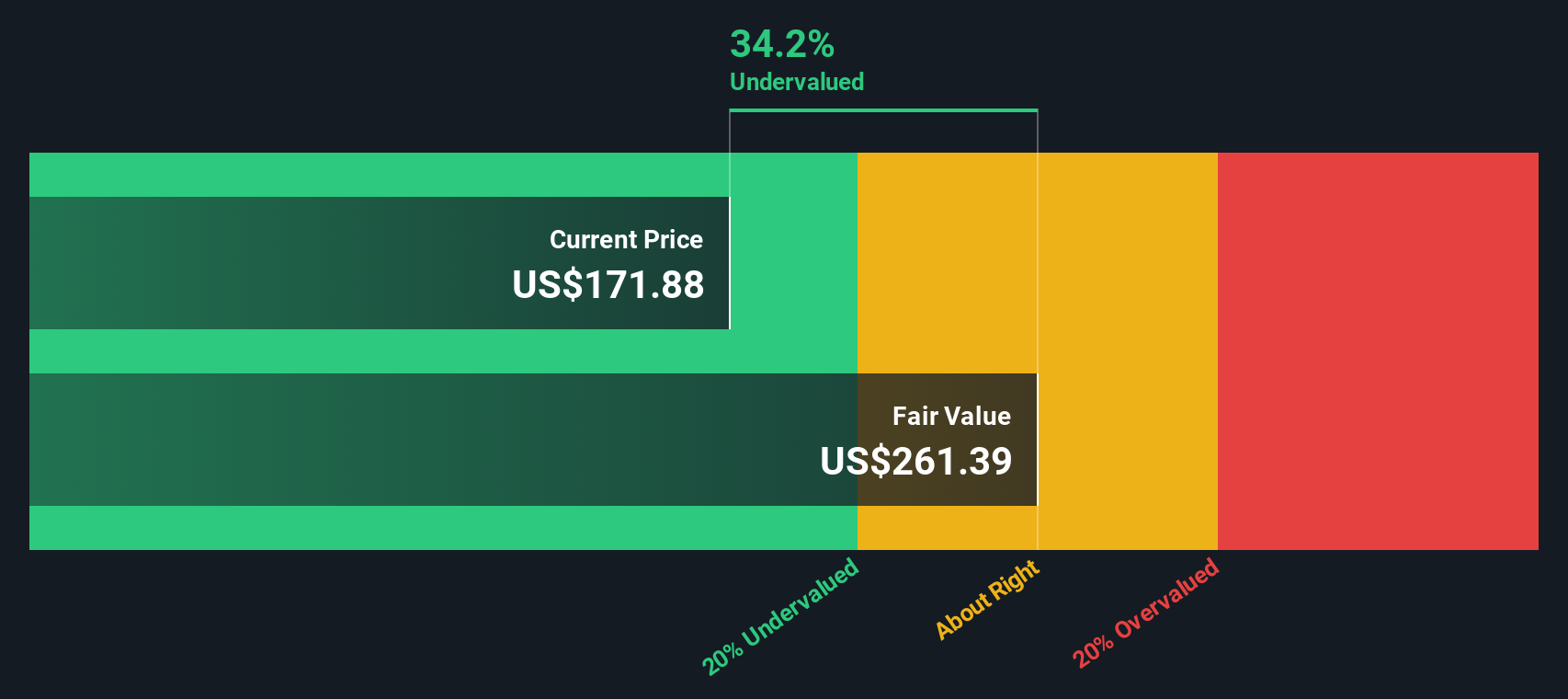

- On our valuation framework, Atlassian currently scores a 4/6 for being undervalued across six separate checks. This is solid but not flawless. Next, we will walk through the key valuation methods behind that score before exploring an even more insightful way to think about what the stock is really worth.

Find out why Atlassian's -41.5% return over the last year is lagging behind its peers.

Approach 1: Atlassian Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business is worth today by projecting the cash it can generate in the future and then discounting those cash flows back to a present value.

For Atlassian, the model starts with current Free Cash Flow of about $1.47 billion and uses analyst forecasts for the next few years, then extrapolates out to 2035. Under this two stage Free Cash Flow to Equity approach, Simply Wall St projects Free Cash Flow could rise to roughly $4.50 billion by 2035. This reflects strong but gradually moderating growth as the business matures.

When all projected cash flows are discounted back, the model arrives at an intrinsic value of roughly $246.37 per share. That implies the stock is trading at about a 33.7% discount to its estimated fair value. This suggests the market is pricing in considerably weaker long term prospects than the cash flow profile supports.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Atlassian is undervalued by 33.7%. Track this in your watchlist or portfolio, or discover 904 more undervalued stocks based on cash flows.

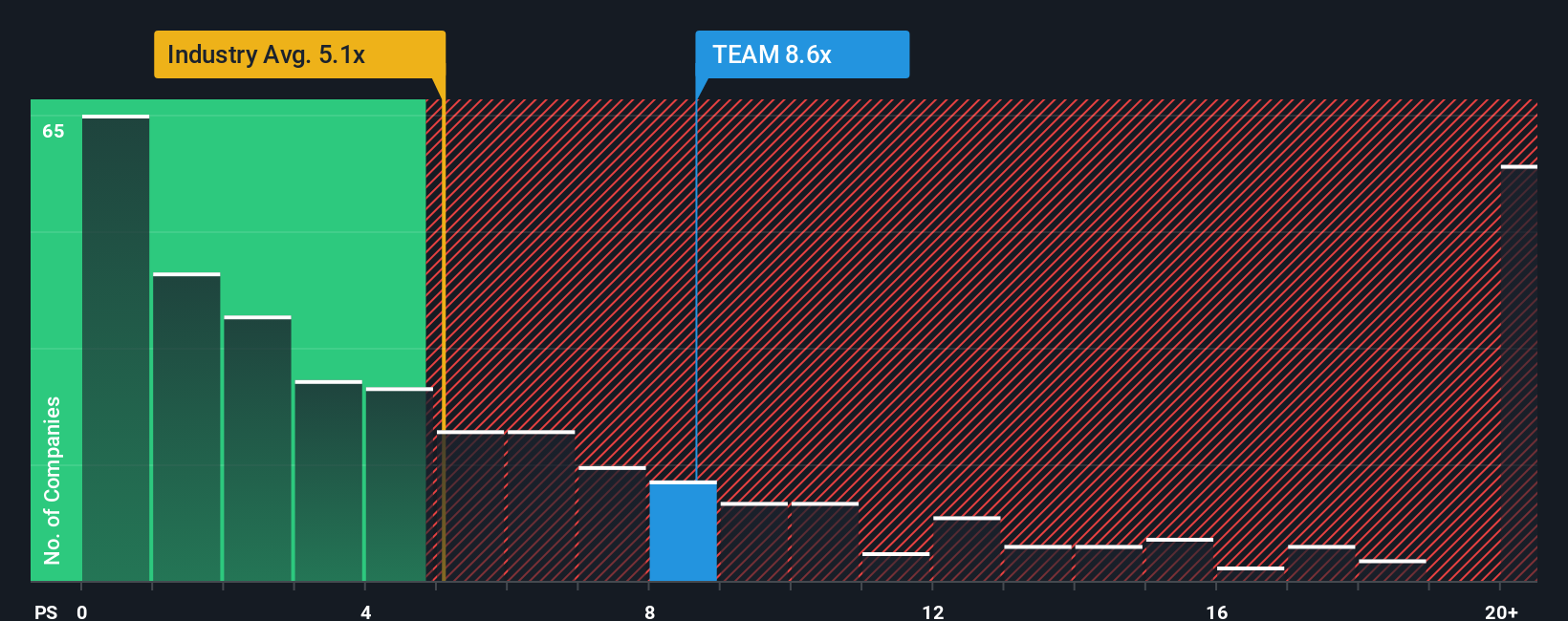

Approach 2: Atlassian Price vs Sales

For growing software businesses that are still prioritizing reinvestment over near term profits, the Price to Sales ratio is often the most practical way to compare valuations, because revenue is less affected by accounting choices than earnings.

In general, higher growth and lower risk justify a higher sales multiple, while slower or more uncertain growth should trade closer to, or below, the industry norm. Atlassian currently trades on a Price to Sales ratio of about 7.87x, which is above the broader Software industry average of roughly 5.07x, but below the peer group average of around 12.68x. To refine that picture, Simply Wall St uses a proprietary “Fair Ratio”, which estimates what a reasonable Price to Sales multiple should be after accounting for Atlassian’s growth profile, margins, risk characteristics, industry and size. For Atlassian, that Fair Ratio is 12.52x, which implies the stock trades meaningfully below the level suggested by those fundamentals and risks.

On this basis, Atlassian appears to be attractively valued on revenue compared to what its business quality and growth would typically warrant.

Result: UNDERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1447 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Atlassian Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to connect your view of Atlassian’s story with a set of numbers like future revenue, earnings, margins and a fair value estimate.

A Narrative is your structured storyline for a company, where you spell out what you think will drive the business, translate that into a financial forecast, and then into a fair value that can be compared against the current market price.

On Simply Wall St, Narratives are easy to use and live on the Community page used by millions of investors. They can help you decide how to act by clearly showing whether your Fair Value sits above or below today’s Price and then keeping that picture fresh as new news, earnings and guidance are released.

For example, one Atlassian Narrative might assume strong AI adoption, enterprise wins and margin expansion that point to fair value around $320 per share. A more cautious Narrative, focused on competition and slower cloud migration, might land closer to about $196. You can then quickly see which story you believe and what that implies for your next move.

Do you think there's more to the story for Atlassian? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:TEAM

Atlassian

Provides a collaboration software that enables organizations to connect all teams through a system of work that unlocks productivity at scale worldwide.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Unicycive Therapeutics (Nasdaq: UNCY) – Preparing for a Second Shot at Bringing a New Kidney Treatment to Market (TEST)

Rocket Lab USA Will Ignite a 30% Revenue Growth Journey

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026