- United States

- /

- IT

- /

- NasdaqGS:OKTA

Okta (NasdaqGS:OKTA) Stock Surges 33% Over The Last Quarter With Fourth-Quarter Revenue Reaching US$682M

Reviewed by Simply Wall St

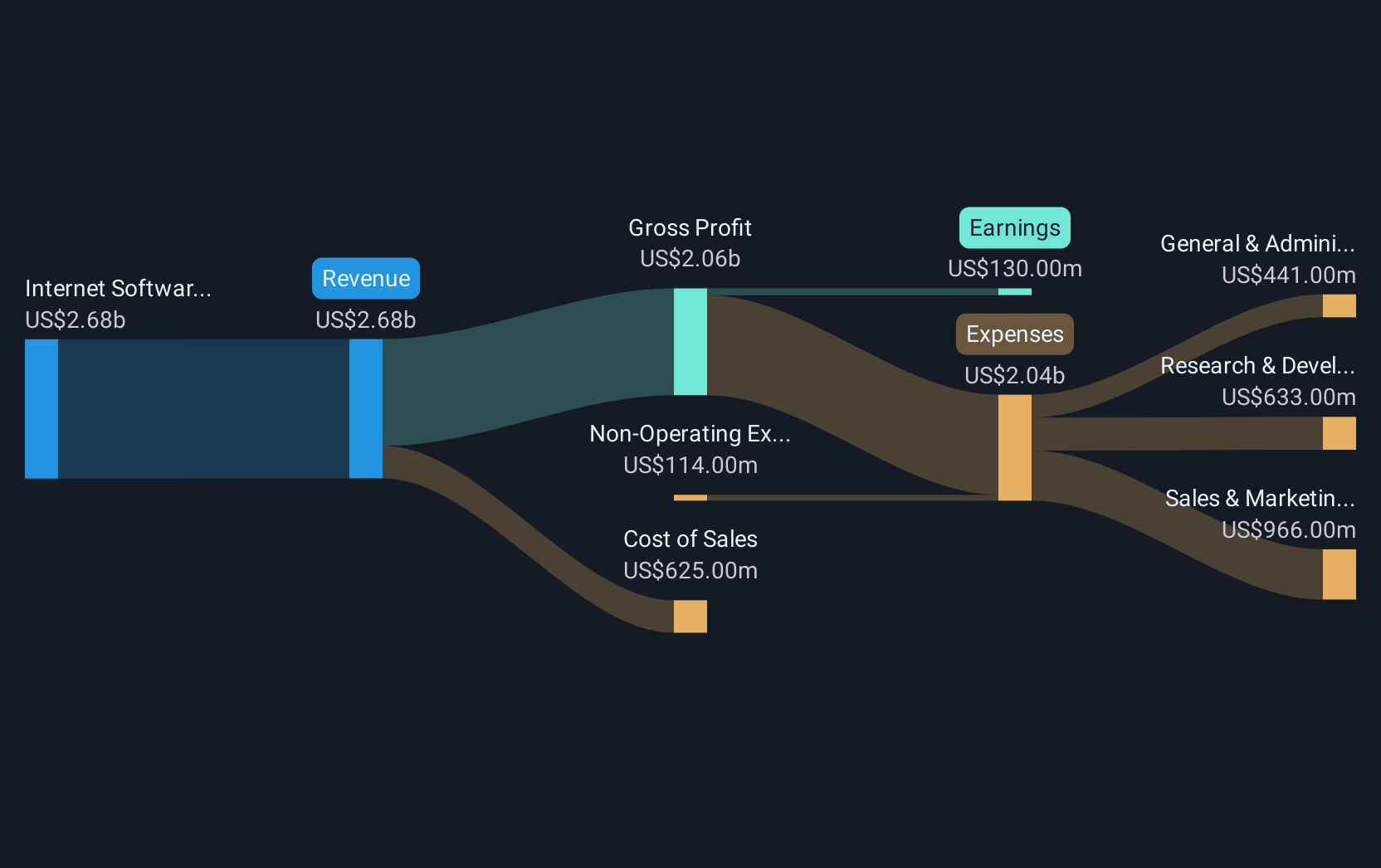

Okta (NasdaqGS:OKTA) recently reported a robust financial performance, with fourth-quarter revenue rising to $682 million and a net income of $23 million, marking a significant shift from previous losses. This financial upturn, combined with optimistic revenue forecasts for fiscal 2026 and plans for strategic technology acquisitions, has likely supported the company's stock price surge of 33% over the last quarter. Okta's partnerships, notably with Incode Technologies, alongside recent executive changes, complement their positive growth narrative. This rise occurred despite broader market volatility and uncertainty surrounding potential new tariffs and economic concerns.

Buy, Hold or Sell Okta? View our complete analysis and fair value estimate and you decide.

Over the past year, Okta's total shareholder return was limited to 2.00%. Despite this, the company's performance lagged behind both the broader US market and the US IT industry, which saw returns of 7.5% and 7.9%, respectively. Several factors influenced this performance. Okta's full-year results showed revenue growth to US$2.61 billion and a shift from a net loss to a net income of US$28 million. The company also pursued strategic partnerships, notably with Zscaler and Jamf in late 2024, enhancing its digital and security offerings.

Mid-2024 saw significant corporate developments, including the introduction of bylaw amendments to align with SEC regulations. Additionally, Okta's M&A strategies revealed intentions for tech tuck-ins to further its roadmap. Despite these efforts, the stock's valuation and broader market challenges might have contributed to its underperformance relative to peers. However, expected earnings growth and revenue projections could bode well for future returns beyond the past year.

Get an in-depth perspective on Okta's performance by reading our balance sheet health report here.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:OKTA

Okta

Operates as an identity partner in the United States and internationally.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Community Narratives