Advertisement

- United States

- /

- Software

- /

- NasdaqGS:IDCC

Should InterDigital’s 6G ISAC Advances and New IoT Licensing Deal Require Action From IDCC Investors?

Reviewed by Sasha Jovanovic

- InterDigital recently showcased its integrated sensing and communication (ISAC) innovations at the IEEE International Conference on Communications in Glasgow, while also highlighting architectural enhancements for 6G ISAC and a first-of-its-kind collaborative cellular and Wi‑Fi sensing implementation.

- Separately, InterDigital announced a new IoT patent license agreement with a fintech payments company, extending its cellular and Wi‑Fi patent coverage to point‑of‑sale devices and underlining the company’s role in monetizing connectivity across everyday payment infrastructure.

- Next, we’ll examine how InterDigital’s new IoT patent license agreement could influence its investment narrative and future licensing mix.

We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

InterDigital Investment Narrative Recap

To own InterDigital, you generally need to believe its patent portfolio can keep converting wireless and consumer device standards into recurring, high‑margin licensing cash flows. The biggest near term catalyst remains execution on new and renewed licenses beyond smartphones, while a key risk is pressure on margins if earnings continue to soften. The new IoT point of sale license is directionally positive but not large enough by itself to materially change those near term drivers.

The IoT patent license with the fintech payments company looks most relevant here, because it extends InterDigital’s reach into everyday payment terminals that rely on cellular and Wi‑Fi standards. If deals like this gradually scale, they could support the shift toward a more diversified, less smartphone‑dependent royalty base that analysts see as important for smoothing revenue and earnings over time.

But while licensing wins can look reassuring, investors should also be aware of the risk that...

Read the full narrative on InterDigital (it's free!)

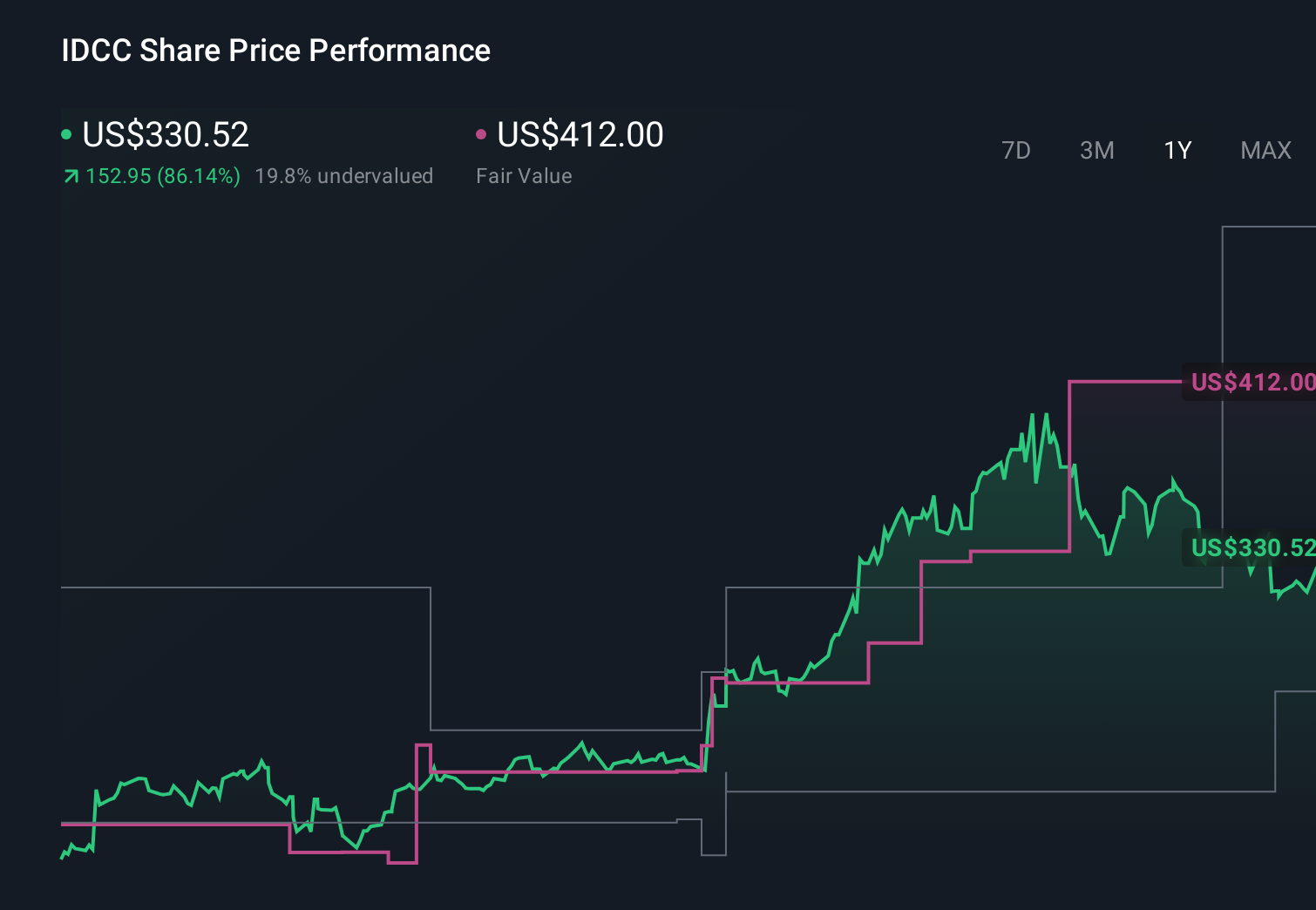

InterDigital's narrative projects $824.6 million revenue and $350.8 million earnings by 2029.

Uncover how InterDigital's forecasts yield a $462.67 fair value, a 76% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already modeling about US$1.0 billion of revenue and US$487.6 million of earnings by 2029, yet this latest IoT and 6G sensing news could either reinforce that upbeat view or highlight how much those expectations depend on your comfort with long term patent and standards risk.

Explore 6 other fair value estimates on InterDigital - why the stock might be worth as much as 76% more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your InterDigital research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free InterDigital research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate InterDigital's overall financial health at a glance.

Interested In Other Possibilities?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Explore 29 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 28 companies in the world exploring or producing it. Find the list for free.

- The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:IDCC

InterDigital

Operates as a global research and development company focuses on wireless, visual, artificial intelligence (AI), and related technologies.

Flawless balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RI

Rick_Orford on Upside Gold ·

This Gold Stock Could Triple if Its Gold Resource Grows

Fair Value:CA$466.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9720.3% undervalued

26 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1927.6% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

BJ

Bjergby on PagSeguro Digital ·

PagSeguro: A Cheap Bet on a Bank Hiding Inside a Payments Company, Priced for Failure

Fair Value:US$23.861.3% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

HU

Hunter_Z on Hektar Real Estate Investment Trust ·

Hektar REIT: Deep Value, Attractive Yield, and a Portfolio Transformation Story in the Making

Fair Value:RM 156.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kapirey on CSG ·

CSG represents a high-quality industrial compounder operating in a structurally growing and geopolitically reinforced market,

Fair Value:€3037.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AR

artoflosing on BlackBerry ·

Accidental transformation from Phones to Physical AI.

Fair Value:CA$16.2228.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.8% undervalued

116 followersusers have followed this narrative

2 commentsusers have commented on this narrative

33 likesusers have liked this narrative

TR

tripledub on lululemon athletica ·

Lululemon Got Boring Right About the Time It Got Cheap. That's Usually the Point

Fair Value:US$22042.1% undervalued

27 followersusers have followed this narrative

6 commentsusers have commented on this narrative

32 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$268.6120.0% undervalued

1192 followersusers have followed this narrative

7 commentsusers have commented on this narrative

35 likesusers have liked this narrative