Advertisement

- United States

- /

- Software

- /

- NasdaqGS:IDCC

New Forecasts: Here's What Analysts Think The Future Holds For InterDigital, Inc. (NASDAQ:IDCC)

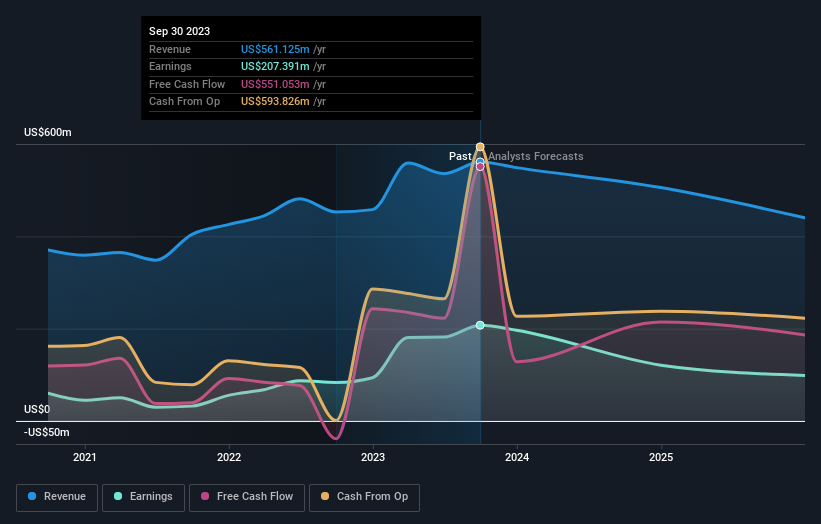

Shareholders in InterDigital, Inc. (NASDAQ:IDCC) may be thrilled to learn that the analysts have just delivered a major upgrade to their near-term forecasts. The revenue forecast for next year has experienced a facelift, with analysts now much more optimistic on its sales pipeline.

After the upgrade, the consensus from InterDigital's five analysts is for revenues of US$506m in 2024, which would reflect a chunky 9.9% decline in sales compared to the last year of performance. Statutory earnings per share are anticipated to plummet 50% to US$4.03 in the same period. Previously, the analysts had been modelling revenues of US$435m and earnings per share (EPS) of US$4.03 in 2024. There's clearly been a surge in bullishness around the company's sales pipeline, even if there's no real change in earnings per share forecasts.

See our latest analysis for InterDigital

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the InterDigital's past performance and to peers in the same industry. These estimates imply that sales are expected to slow, with a forecast annualised revenue decline of 8.0% by the end of 2024. This indicates a significant reduction from annual growth of 12% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 12% per year. It's pretty clear that InterDigital's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The most obvious conclusion from this consensus update is that there's been no major change in the business' prospects in recent times, with analysts holding earnings per share steady, in line with previous estimates. Fortunately, they also upgraded their revenue estimates, and are forecasting revenues to grow slower than the wider market. Given that analysts appear to be expecting substantial improvement in the sales pipeline, now could be the right time to take another look at InterDigital.

Even so, the longer term trajectory of the business is much more important for the value creation of shareholders. At Simply Wall St, we have a full range of analyst estimates for InterDigital going out to 2025, and you can see them free on our platform here..

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:IDCC

InterDigital

Operates as a global research and development company focuses on wireless, visual, artificial intelligence (AI), and related technologies.

Flawless balance sheet with solid track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.4% undervalued

NO

Community Contributor