Advertisement

- United States

- /

- Software

- /

- NasdaqGS:IDCC

Assessing InterDigital (IDCC) Valuation After Major Chinese Licensing Renewal

Why InterDigital’s new licensing deal matters for shareholders

InterDigital (IDCC) has renewed a worldwide, non-exclusive, royalty bearing license with a major Chinese vendor. This five year agreement covers smartphones and other cellular devices under its core cellular, WiFi, and HEVC patents.

See our latest analysis for InterDigital.

The renewed licensing deal comes as InterDigital’s share price sits at US$312.01, with a 1 day share price return of 0.94% and a 7 day share price return of 0.97%. The 30 day and 90 day share price returns of 11.93% and 14.45% declines contrast with very strong 1 year and 5 year total shareholder returns of 77.13% and over 4x respectively. This suggests long term momentum has been strong even as recent share price performance has cooled.

If this licensing update has your attention, it could be a useful time to widen your watchlist with high growth tech and AI stocks that are also exposed to wireless, software and AI themes.

With InterDigital’s shares at US$312.01 after a strong multi year run, recent double digit declines over 30 and 90 days raise a key question: is the stock now trading below its worth, or is the market already pricing in future growth?

Most Popular Narrative: 24.3% Undervalued

Compared with InterDigital’s last close at US$312.01, the most followed narrative points to a higher fair value of about US$412, built on detailed long term forecasts.

The analysts have a consensus price target of $266.5 for InterDigital based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $311.0, and the most bearish reporting a price target of just $220.0.

The narrative leans heavily on projected revenue contraction, lower profit margins, and a higher future P/E multiple. Curious which assumptions have the biggest impact on that US$412 fair value?

Result: Fair Value of $412 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, you also need to weigh the risk that revenue remains dependent on large, sometimes lumpy licensing deals, and that newer streaming and IoT opportunities take longer to play out.

Find out about the key risks to this InterDigital narrative.

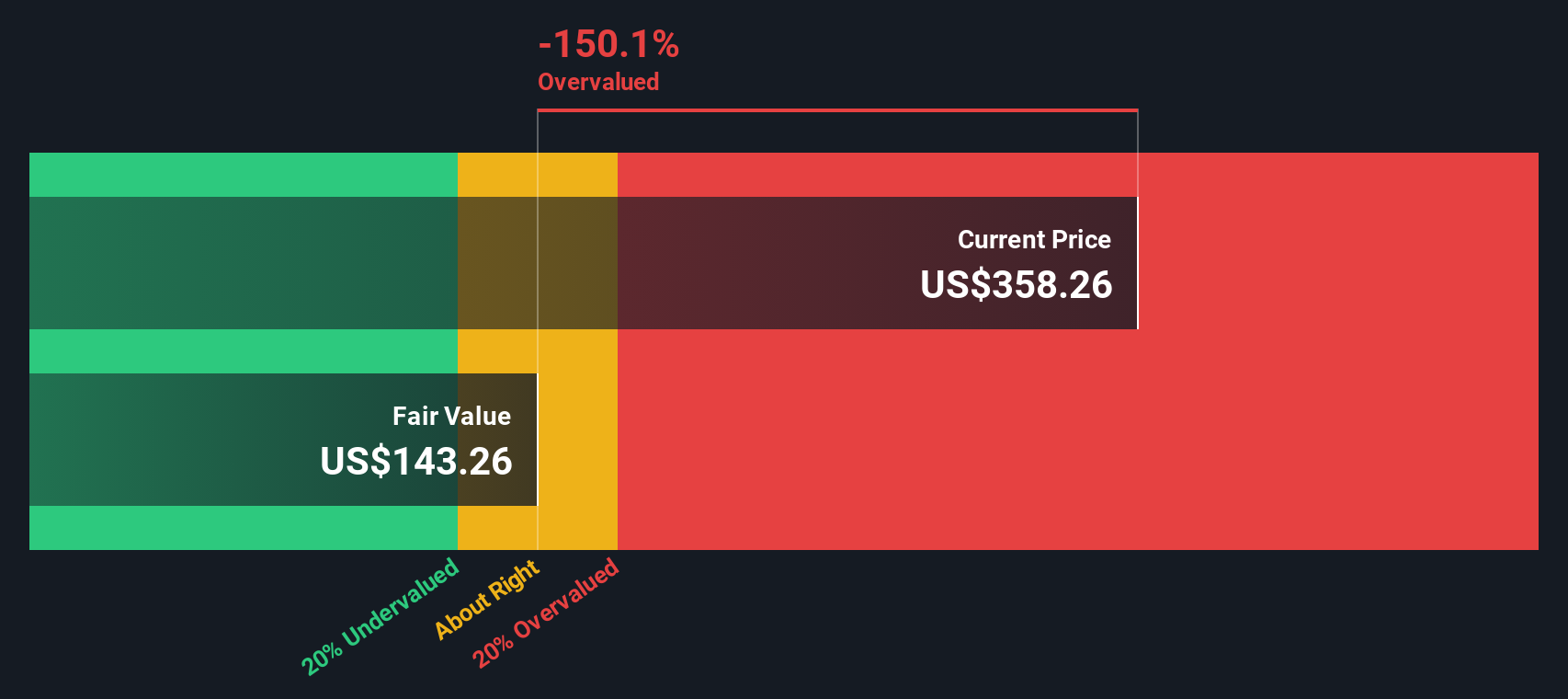

Another View on InterDigital’s Valuation

Our SWS DCF model paints a very different picture for InterDigital. At a share price of US$312.01, the stock sits well above our DCF based fair value estimate of about US$70.70. This screens as expensive rather than undervalued. So which story do you think fits the business better today?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out InterDigital for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 883 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own InterDigital Narrative

If you are not convinced by these views or simply prefer to dig into the numbers yourself, you can build a tailored thesis in minutes: Do it your way.

A great starting point for your InterDigital research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If InterDigital has sharpened your interest in licensing and wireless themes, it is worth broadening your watchlist with targeted stock ideas picked from curated screeners.

- Spot under-the-radar growth potential by checking out these 3537 penny stocks with strong financials that pair smaller market caps with stronger financial profiles.

- Zero in on next generation tech by scanning these 25 AI penny stocks that focus on artificial intelligence and related digital infrastructure.

- Focus on value by reviewing these 883 undervalued stocks based on cash flows based on cash flows before prices move away from your preferred range.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:IDCC

InterDigital

Operates as a global research and development company focuses on wireless, visual, artificial intelligence (AI), and related technologies.

Flawless balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

JO

Jolt_Communications on ZenaTech ·

ZenaTech: A big bet on the rise of AI drones and drones-as-a-service

Fair Value:US$6.8563.6% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CL

Clive_Thompson on Hermès International Société en commandite par actions ·

Hermès - Expensive bags, and expensive stock. And the story of €14 billion of bearer shares gone missing.

Fair Value:€1.51k9.6% overvalued

23 followersusers have followed this narrative

1 commentusers have commented on this narrative

23 likesusers have liked this narrative

TR

tripledub on Intuit ·

A Wonderful Business at a Not-So-Wonderful Price

Fair Value:US$5008.6% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FA

FA_Trader on A1 A.K. Koh Group Berhad ·

A1 A.K. Koh Group Berhad: A simple local food story that could ride on Visit Malaysia 2026

Fair Value:RM 0.3345.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Recently Updated Narratives

VE

Vestra on McDonald's ·

McDonald’s (MCD): The "Digital Golden Arches" and the Pivot to Value

Fair Value:US$343.2810.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Lam Research ·

Lam Research (LRCX): The "AI Foundry" Backbone and the Memory Supercycle

Fair Value:US$274.915.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on SolarEdge Technologies ·

SolarEdge Technologies (SEDG): The "Solar Resurrection" and the AI Pivot

Fair Value:US$3437.4% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.377.2% undervalued

56 followersusers have followed this narrative

3 commentsusers have commented on this narrative

30 likesusers have liked this narrative

YA

Yang_ on SoFi Technologies ·

SoFi Technologies: The Apex Aggregator and the Infrastructure of the Modern Financial System

Fair Value:US$22.9825.4% undervalued

48 followersusers have followed this narrative

0 commentsusers have commented on this narrative

36 likesusers have liked this narrative

PD

pdixit1 on Vertiv Holdings Co ·

The Infrastructure AI Cannot Be Built Without

Fair Value:US$408.6437.4% undervalued

39 followersusers have followed this narrative

3 commentsusers have commented on this narrative

18 likesusers have liked this narrative

Trending Discussion

OD

Oddlott on lululemon athletica ·

Thankyou for the interesting comments. So what is the world wide including USA growth rate?

0

|0