Advertisement

- United States

- /

- Software

- /

- NasdaqGS:GTLB

Does GitLab’s Latest AI Partnership Signal a New Growth Trajectory for 2025?

Reviewed by Bailey Pemberton

If you’re staring at your portfolio and wondering what to do with your shares of GitLab, you’re not alone. The stock has been an interesting mix lately. In just the last week it climbed 2.4%, and over the past month it managed a quiet 0.9% lift. Zoom out, though, and you see a tougher picture: GitLab is down 18.1% for the year to date and has slipped 7.6% over the past twelve months. If you’ve held on since the company’s public debut, the returns have been mildly negative over the three-year stretch.

What’s driving these moves? In the backdrop, we’ve seen the broader tech landscape re-rate risk and reward, especially as digital transformation continues to shake up priorities for developers and enterprises. Investors are weighing whether platforms like GitLab can keep capturing growth as competition and macro pressures mount.

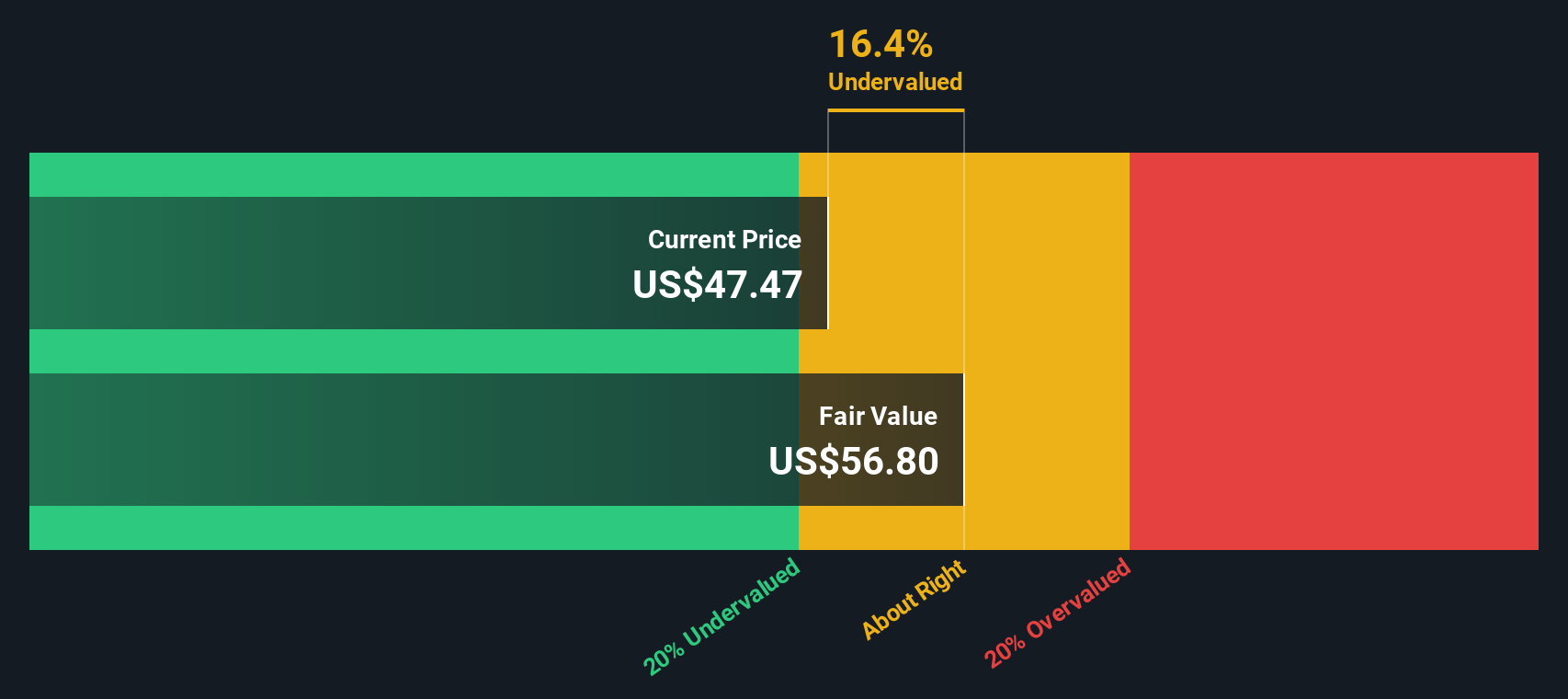

But as with any tech stock, the big question isn’t just about past performance; it’s about what the stock is actually worth right now. By our scorecard, GitLab is undervalued in 3 out of 6 valuation checks, giving it a valuation score of 3. That is not a slam dunk, but it does mean there is a case to be made for further investigation.

So, how does GitLab stack up using common valuation yardsticks? Let’s dig into those methods. Stick around, because at the end of this analysis, I’ll share the most insightful way to gauge what this company’s really worth.

Why GitLab is lagging behind its peers

Approach 1: GitLab Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model is one of the most widely used methods for valuing a company. In simple terms, it estimates the intrinsic value of a stock by projecting the company's future cash flows and then discounting them back to the present day to reflect today's value.

For GitLab, the current Free Cash Flow stands at $33.5 million. Analysts forecast robust cash flow growth over the next several years, with projections reaching $526.7 million by 2030. Notably, analyst consensus provides estimates for the first five years. Simply Wall St extrapolates further into the future based on historical and industry trends.

Applying the 2 Stage Free Cash Flow to Equity model, GitLab's estimated fair value using DCF analysis comes out to $57 per share. According to this assessment, GitLab trades at a 19.0% discount to its intrinsic value, which suggests the stock is currently undervalued.

In summary, the DCF analysis signals a meaningful margin of safety for investors considering GitLab at its current price.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests GitLab is undervalued by 19.0%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

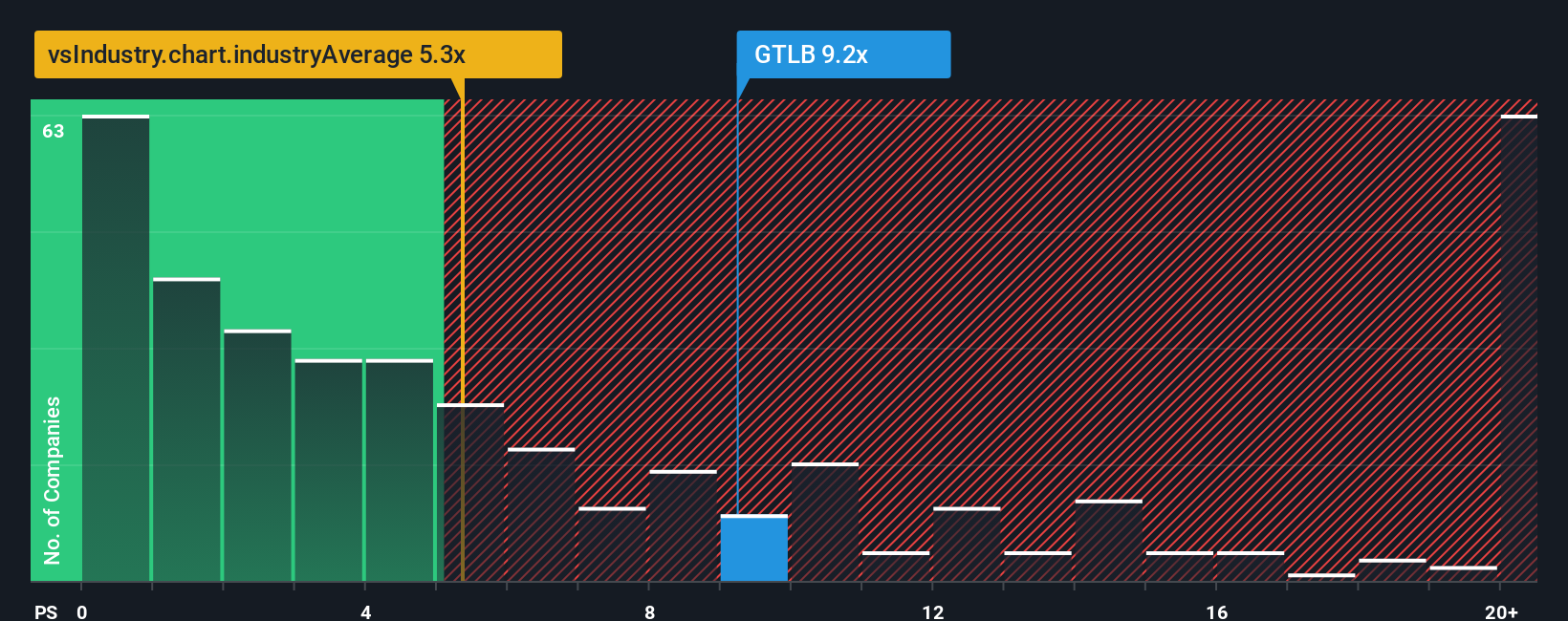

Approach 2: GitLab Price vs Sales (P/S)

The Price-to-Sales (P/S) ratio is a popular way to value software companies like GitLab, particularly when profitability is further down the road but sales growth remains strong. Unlike Price-to-Earnings, which can swing widely for companies investing heavily in future growth, P/S offers a clearer look at how the market values each dollar of revenue. For high-growth businesses in competitive industries, investors often accept higher P/S multiples if they believe future sales will translate into profits.

GitLab currently trades at a P/S ratio of 8.97x. For context, the industry average P/S sits at 5.29x, while direct peers average around 6.78x. On the surface, this places GitLab at a significant premium relative to its software sector, suggesting high expectations for future growth and margin expansion.

However, to get a more accurate read, we can turn to Simply Wall St’s proprietary Fair Ratio, a calculation that sets a “just right” multiple by factoring in specifics like GitLab’s earnings growth outlook, margins, industry dynamics, market cap, and company-specific risks. This method goes a step beyond blunt peer or industry comparisons and offers a perspective tailored to GitLab’s actual business trajectory.

According to this model, GitLab’s fair P/S ratio is 10.02x. This is actually higher than both its current ratio and the sector benchmarks. Because GitLab’s market multiple (8.97x) falls notably below the fair value estimate, the stock appears undervalued on this metric. This suggests the market may not fully appreciate its growth runway and competitive position.

Result: UNDERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your GitLab Narrative

Earlier, we mentioned that there is an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is your chance to create and share a story behind a company’s numbers, linking your personal perspective and expectations for GitLab’s future to a detailed financial forecast and fair value estimate.

Instead of just crunching numbers, Narratives encourage you to think about what really drives the business, then translate those beliefs into concrete projections for revenue, margins, and growth. The Narrative tool, available to everyone within Simply Wall St’s Community page, is designed for all investors. It makes it easy to connect your investment thesis directly with fair value calculations and see how those stack up against the current market price.

Narratives help you make smarter buy or sell decisions by comparing the Fair Value output from your assumptions to the latest Price. As new information emerges, like news or earnings releases, Narratives update automatically so your view stays current and relevant.

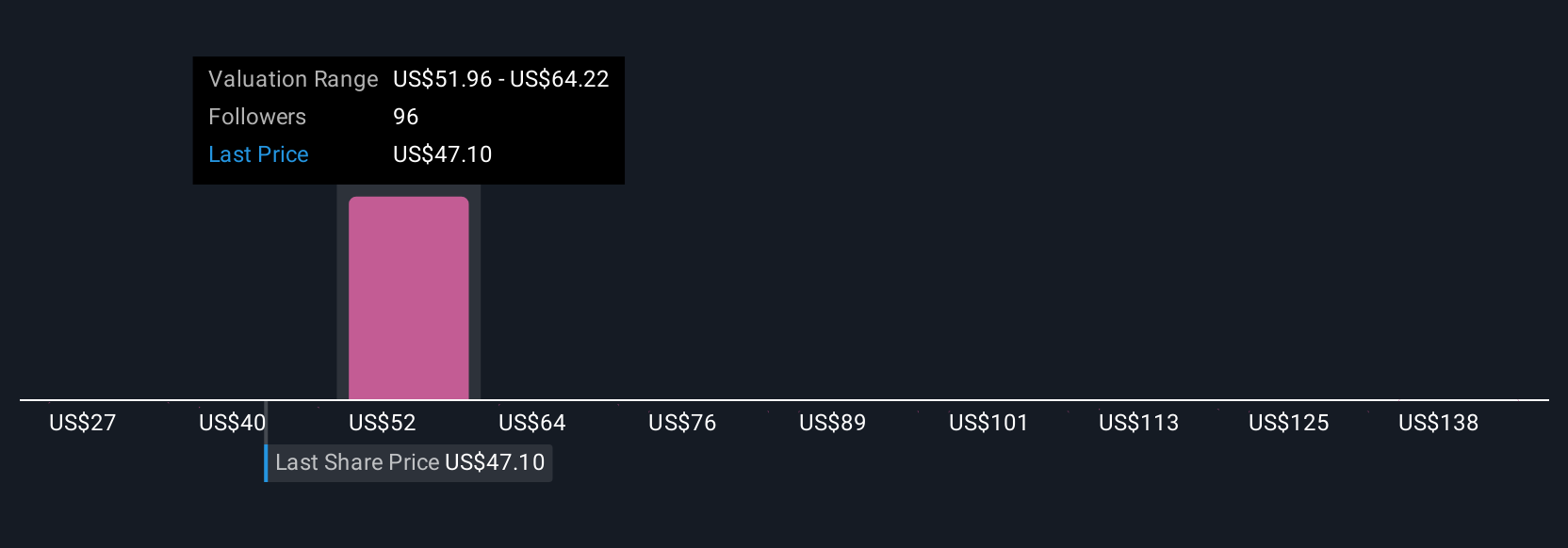

For example, with GitLab, some investors are bullish and see opportunities from deeper AI integrations and new partnerships, leading them to estimate a fair value as high as $85 per share. Others, who are more cautious about competitive risks and growth durability, peg fair value closer to $46 per share.

Do you think there's more to the story for GitLab? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:GTLB

GitLab

Develops software for the software development lifecycle in the United States, Europe, and the Asia Pacific.

Flawless balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2552.0% undervalued

129 followersusers have followed this narrative

0 commentsusers have commented on this narrative

25 likesusers have liked this narrative

BL

BlackGoat on IREN ·

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value:US$71.4848.5% undervalued

227 followersusers have followed this narrative

9 commentsusers have commented on this narrative

33 likesusers have liked this narrative

HE

HedgeY on Arm Holdings ·

The Architecture Layer of AI Computing - But Priced Like the Future Already Arrived?

Fair Value:US$43044.3% undervalued

27 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

HI

Hidden_Rock_Capital on Fiserv ·

Temporary "perfect storm" leads to opportunity to buy financial services leader for less than 5x long-term earnings

Fair Value:US$119.9955.0% undervalued

36 followersusers have followed this narrative

1 commentusers have commented on this narrative

10 likesusers have liked this narrative

Recently Updated Narratives

CH

ChuckN on XPLR Infrastructure ·

Investor Thesis: Why XPLR Infrastructure Could Be Deeply Undervalued in an AI Power Cycle

Fair Value:US$209.0294.3% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

andre_santos on Netflix ·

Netflix - A Fundamental Valuation

Fair Value:US$98.7127.4% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

John_Eric on Reddit ·

Reddit's Discount Is Big Enough to Make Me Suspicious. Here's What I Found When I Went Looking for the Reason.

Fair Value:US$423.6866.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28028.3% undervalued

227 followersusers have followed this narrative

9 commentsusers have commented on this narrative

15 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9110.7% overvalued

108 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23054.8% overvalued

121 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative

Trending Discussion

GR

greg_xasak on Fiserv ·

As someone who has dealt directly with them as a CTO for a credit union, I have 8 years of horror stories about doing business with them. If there was any other competitor than could deliver 80% of Fiserv services, there would be a mad rush to migrate to them. They should thank their lucky stars they are a near monopoly. this industry is so ripe for a well funded competitor. Their integration of technology is awful, their ability to fix their own implementation screwups is sadly tragic. Sometimes they just silently kill support tickets without resolution and you never find out until you do a follow up inquiry. Why, because sometimes no one you are dealing with knows how to fix it and knows no one to ask for help. They can not meet their own implementation deadlines and sometimes there is no one on a technical team dealing with you that has any banking or credit union experience. The is an industry insider phrase when you meet other Fiserv customers called being "Fiserved". It means telling others of your worst stories of dealing with them. Ask around, all CTO's have some doozies.

1

|0