Advertisement

- United States

- /

- Software

- /

- NasdaqGS:EVCM

EverCommerce (EVCM): Revisiting Valuation After AI-Focused Shift, Asset Sales, Acquisitions and Capital Allocation Moves

EverCommerce (EVCM) is back in the spotlight after doubling down on AI powered vertical SaaS, selling noncore assets, buying focused platforms like ZyraTalk, and extending its share buyback plan alongside a fresh debt refinancing.

See our latest analysis for EverCommerce.

The market seems to be warming back up to that sharper AI powered SaaS focus, with EverCommerce’s 42.96% 1 month share price return pushing the stock near recent highs. However, the 1 year total shareholder return is still slightly negative, which suggests momentum is rebuilding after a tougher stretch.

If EverCommerce’s rebound has your attention, this could be a good moment to explore similar opportunities in high growth tech and AI stocks and see what else is starting to move.

Yet with the share price already near analyst targets and only a modest implied intrinsic discount, the key question is whether EverCommerce is still trading below its true AI powered potential, or if the market is already pricing in the next leg of growth.

Most Popular Narrative: 2.5% Undervalued

With the narrative fair value slightly above the last close of $12.08, the story hinges on profitability inflecting even as revenues edge lower.

The divestiture of the lower-growth Marketing Technology segment and subsequent focus on core verticals (EverPro, EverHealth, EverWell) has increased operational clarity and reduced seasonality, setting the stage for improved profitability and more predictable, linear revenue patterns. Strong free cash flow generation, expanding gross margins through payments mix shift, and active share repurchases ($20.6M in Q2) improve balance sheet flexibility and EPS outlook, increasing the likelihood of rerating as secular tailwinds persist.

Want to see how shrinking top line, rising margins, and a future earnings multiple usually reserved for sector leaders all fit together? The narrative leans on aggressive profit expansion, disciplined buybacks, and a bold view on where recurring SaaS cash flows can take this platform. Curious which specific profitability leap and valuation multiple are doing the heavy lifting behind that fair value?

Result: Fair Value of $12.39 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on EverCommerce successfully sustaining payments-led margin gains while avoiding underinvestment in innovation that could invite faster-moving competitors.

Find out about the key risks to this EverCommerce narrative.

Another Lens on Value

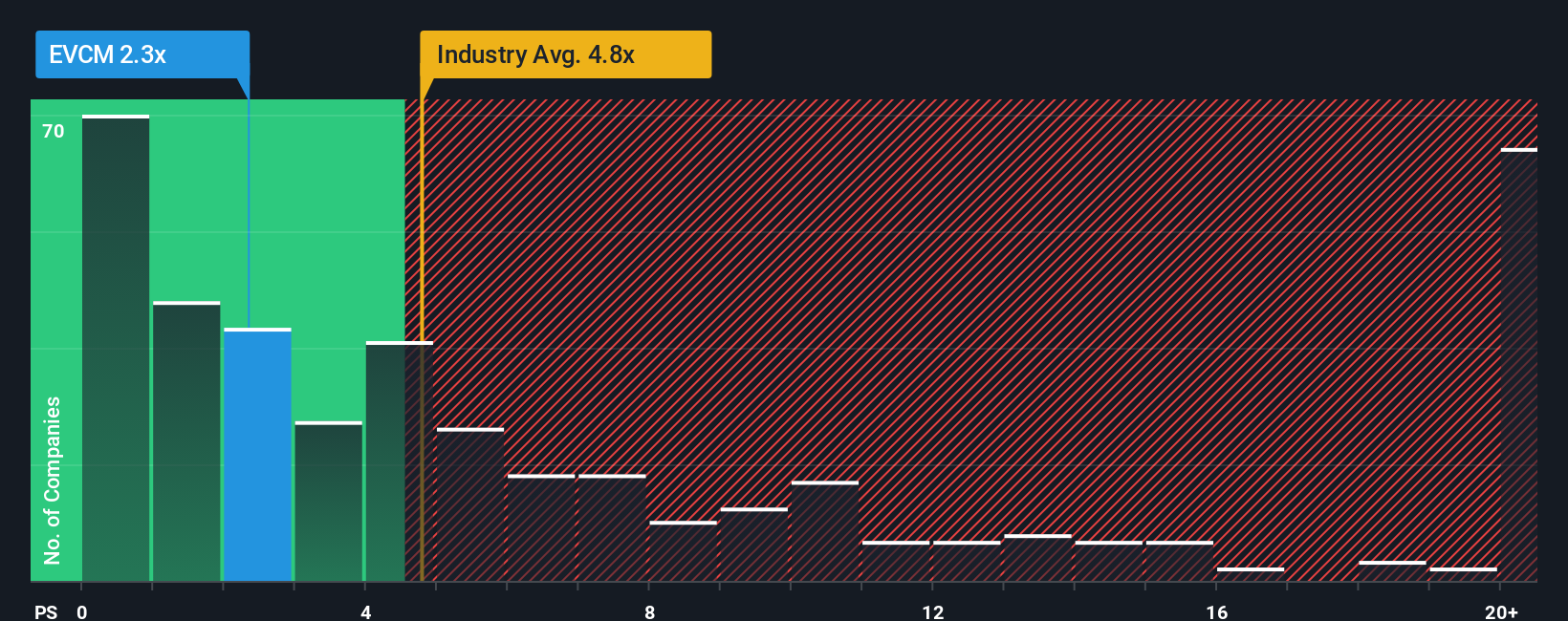

Look past the AI story and the picture shifts. On a price to sales of 3x, EverCommerce screens cheaper than US software peers at 4.9x, yet still richer than its 2.6x fair ratio, which hints at upside if momentum lasts, but also downside if growth wobbles.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own EverCommerce Narrative

If you see the story differently or want to stress test the numbers yourself, you can build a custom view in just a few minutes: Do it your way.

A great starting point for your EverCommerce research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Ready for more high conviction ideas?

Before momentum shifts again, use the Simply Wall St Screener to uncover focused opportunities that match your strategy, instead of waiting for the next headline.

- Capitalize on early stage growth by targeting these 3614 penny stocks with strong financials that already show balance sheet strength and improving fundamentals.

- Ride structural demand for automation and data by zeroing in on these 26 AI penny stocks positioned at the heart of intelligent software adoption.

- Lock in potential mispricings with these 908 undervalued stocks based on cash flows that screen cheap on cash flows before the broader market catches up.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if EverCommerce might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:EVCM

EverCommerce

Provides integrated software-as-a-service solutions for service-based small and medium-sized businesses in the United States and internationally.

Solid track record with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7057.9% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17044.9% undervalued

40 followersusers have followed this narrative

0 commentsusers have commented on this narrative

12 likesusers have liked this narrative

FU

FundamentalFlow on Onto Innovation ·

Onto Innovation: The Advanced Packaging Chokepoint 51.3% undervalued intrinsic discount

Fair Value:US$38033.4% undervalued

26 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7447.4% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

Recently Updated Narratives

FU

FundamentalFlow on Karman Holdings ·

KRMN — Karman Space & Defense: Down 58% from Peak, Is the Market Mispricing a Hypergrowth Defense Compounder?

Fair Value:US$105.653.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

NI

nitram on First Interstate BancSystem ·

Solid, rationally run company will provide consistent results, stable dividend, and moderate growth

Fair Value:US$4011.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BA

Bakullizta on Unilever Indonesia ·

Nilai Wajar di Tengah Pemulihan Kinerja

Fair Value:Rp931.1168.6% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7447.4% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9722.6% undervalued

57 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1933.2% undervalued

48 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

Trending Discussion

SI

Simply Wall St User on Access Holdings ·

It's wonderful. It has greatly helped me take informed decisions.

0

|0

CO

composite32 on Ronesans Gayrimenkul Yatirim ·

Selamlar Teşekkürler.. Radarımda olan bir şirket değil, Halka açıklık oranı %40'ın üzerinde olan şir...

0

|0