Advertisement

- United States

- /

- Software

- /

- NasdaqCM:CLSK

High Growth Tech Stocks in US with Promising Potential

Simply Wall St

Reviewed by Simply Wall St

Over the last 7 days, the United States market has remained flat, yet it is up 8.0% over the past year with earnings forecasted to grow by 14% annually. In this context of steady growth, identifying high growth tech stocks involves looking for companies that demonstrate strong innovation and adaptability in a competitive landscape.

Top 10 High Growth Tech Companies In The United States

| Name | Revenue Growth | Earnings Growth | Growth Rating |

|---|---|---|---|

| Super Micro Computer | 27.47% | 39.60% | ★★★★★★ |

| Ardelyx | 20.57% | 59.97% | ★★★★★★ |

| AVITA Medical | 27.69% | 85.07% | ★★★★★★ |

| Clene | 65.19% | 67.34% | ★★★★★★ |

| Travere Therapeutics | 28.83% | 64.80% | ★★★★★★ |

| TG Therapeutics | 25.99% | 38.42% | ★★★★★★ |

| Alnylam Pharmaceuticals | 23.67% | 61.11% | ★★★★★★ |

| Lumentum Holdings | 21.54% | 110.32% | ★★★★★★ |

| Alkami Technology | 22.46% | 76.67% | ★★★★★★ |

| Ascendis Pharma | 35.16% | 60.26% | ★★★★★★ |

Click here to see the full list of 237 stocks from our US High Growth Tech and AI Stocks screener.

Below we spotlight a couple of our favorites from our exclusive screener.

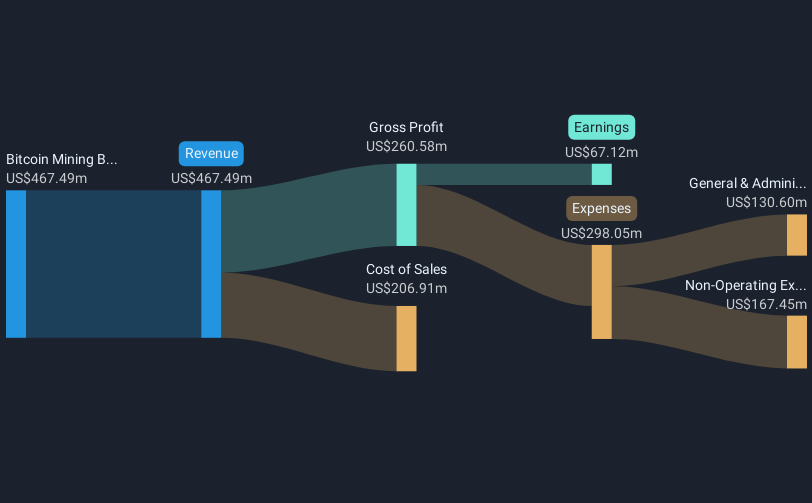

CleanSpark (NasdaqCM:CLSK)

Simply Wall St Growth Rating: ★★★★★☆

Overview: CleanSpark, Inc. is a bitcoin mining company operating in the Americas with a market capitalization of $2.58 billion.

Operations: The company generates revenue primarily through its bitcoin mining operations, which brought in $537.40 million.

CleanSpark, despite its recent earnings volatility with a significant net loss reported in Q2 2025, shows promising growth indicators. The company's revenue is expected to surge by 35.8% annually, outpacing the broader US market's growth of 8.4%. This aggressive expansion is mirrored in their R&D investment strategy which remains robust, underpinning future innovations and potentially lucrative returns as they aim to pivot towards profitability within three years. Moreover, CleanSpark’s strategic maneuvers include expanding their digital asset management capabilities and enhancing their credit facilities, positioning them well within the high-tech financial ecosystem of blockchain and Bitcoin production—a sector ripe with opportunity but also fraught with risk given its inherent market volatility.

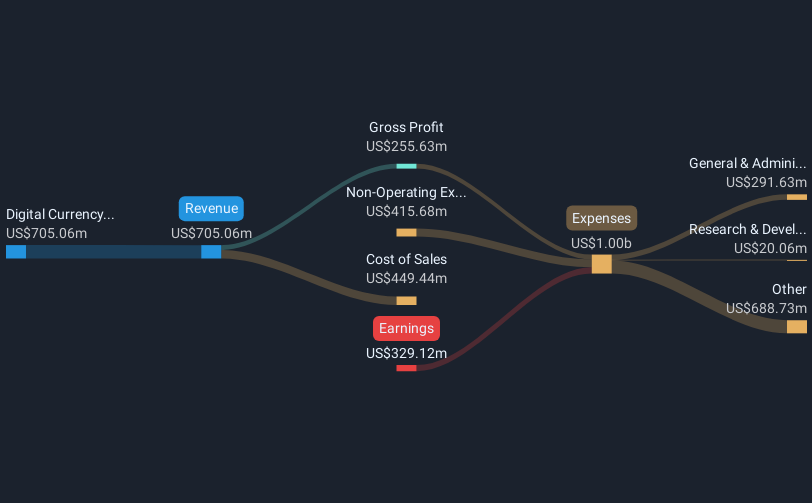

MARA Holdings (NasdaqCM:MARA)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: MARA Holdings, Inc. is a digital asset technology company based in the United States with a market capitalization of $5.55 billion.

Operations: MARA Holdings generates revenue primarily from its digital currency blockchain segment, which amounts to $705.06 million.

Amidst a challenging quarter, MARA Holdings reported a significant shift from a net income of USD 337.17 million to a net loss of USD 533.2 million year-over-year, despite an increase in sales to USD 213.88 million from USD 165.2 million. This volatility is mirrored in their Bitcoin production, which decreased from 829 BTC in March to 705 BTC in April, reflecting the inherent risks and opportunities within the cryptocurrency sector. The company's aggressive revenue growth forecast at an annual rate of 15.2% positions it favorably against the broader market's growth expectation of 8.4%. However, its current unprofitability and shareholder dilution over the past year highlight critical areas needing strategic focus as MARA aims for profitability within three years amidst market uncertainties.

- Take a closer look at MARA Holdings' potential here in our health report.

Assess MARA Holdings' past performance with our detailed historical performance reports.

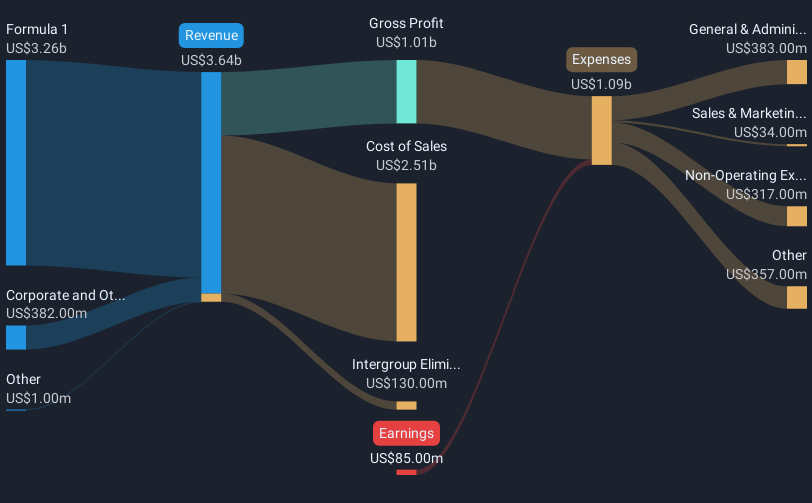

Formula One Group (NasdaqGS:FWON.K)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Formula One Group, along with its subsidiaries, operates in the motorsports industry primarily in the United States and the United Kingdom, with a market capitalization of approximately $23.54 billion.

Operations: Formula One Group generates revenue primarily from its Formula 1 segment, which accounts for $3.26 billion. The company operates in the motorsports industry across the United States and the United Kingdom.

Formula One Group's recent financial performance reveals a challenging landscape with Q1 sales dropping to $400 million from $550 million year-over-year, alongside a decrease in net income to $22 million from $77 million. Despite these setbacks, the company is expected to pivot towards profitability with an impressive forecasted annual earnings growth of 42.45%. This potential turnaround is underpinned by a solid revenue growth rate of 8.5% annually, slightly outpacing the broader U.S. market's growth rate of 8.4%. Moreover, Formula One Group maintains a positive free cash flow status, providing it with essential liquidity to navigate future uncertainties and invest in strategic areas that could enhance its competitive edge in the entertainment sector.

Next Steps

- Embark on your investment journey to our 237 US High Growth Tech and AI Stocks selection here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqCM:CLSK

High growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|4.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|32.5% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|21.9% undervalued

BL

Community Contributor