- United States

- /

- Semiconductors

- /

- NasdaqGS:QCOM

The Bull Case For QUALCOMM (QCOM) Could Change Following Strong Q3 Results and Share Buyback

Reviewed by Simply Wall St

- Earlier this month, QUALCOMM reported third quarter results showing revenue of US$10.37 billion and net income of US$2.67 billion, both up compared to the previous year, and highlighted significant progress in its automotive and IoT businesses.

- In addition, QUALCOMM completed a major buyback of 34.69 million shares since November 2024 and emphasized ongoing expansion in AI and data center markets, despite challenges related to Apple reducing its reliance on QUALCOMM’s chips.

- We’ll examine how QUALCOMM’s continued growth in automotive and IoT segments impacts the longer-term investment outlook for the company.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 26 best rare earth metal stocks of the very few that mine this essential strategic resource.

QUALCOMM Investment Narrative Recap

Owning QUALCOMM stock requires confidence in its transition from a mobile chip leader to a key supplier for automotive, IoT, and next-generation AI products. The latest quarterly results reinforced strong progress in these diversification efforts, while the short-term catalyst remains execution in the automotive and IoT segments. Near-term, the most significant risk continues to be the reduction in Apple-sourced revenues as the company shifts to in-house chips, but the recent results have not changed this risk profile in a material way.

QUALCOMM's completion of its US$5.3 billion buyback, representing over 3% of outstanding shares since late 2024, stands out as particularly relevant. This move underscores management's commitment to shareholder returns even as the company invests heavily in new growth areas like automotive and AI, both of which remain central to the near-term investment case as catalysts.

However, investors should be aware that even as diversification accelerates, dependency on major OEMs could still pose future headwinds...

Read the full narrative on QUALCOMM (it's free!)

QUALCOMM's narrative projects $46.9 billion in revenue and $12.2 billion in earnings by 2028. This requires 2.7% yearly revenue growth and a $0.6 billion increase in earnings from the current $11.6 billion.

Uncover how QUALCOMM's forecasts yield a $175.46 fair value, a 19% upside to its current price.

Exploring Other Perspectives

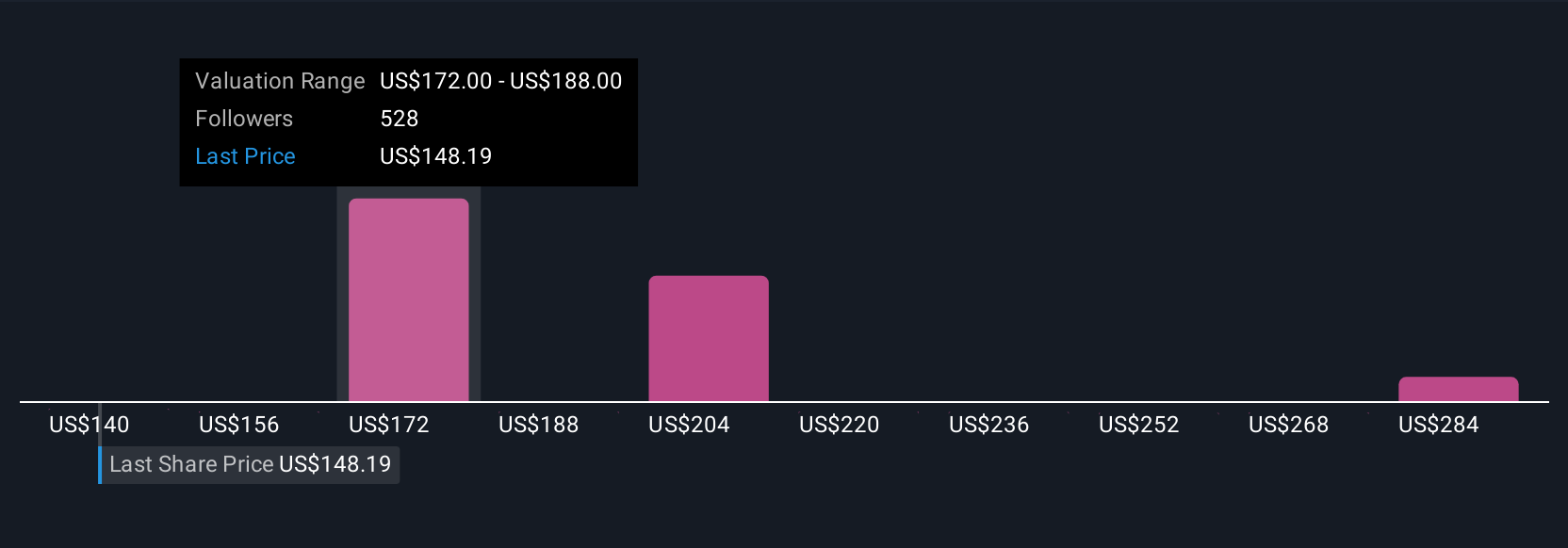

Fair value estimates from 35 Simply Wall St Community members range widely from US$140 to US$300 per share. While many see opportunity in diversification into automotive and IoT, others are focused on competitive risks that could impact QUALCOMM’s momentum and long-term returns, explore these differing views for a fuller picture.

Explore 35 other fair value estimates on QUALCOMM - why the stock might be worth over 2x more than the current price!

Build Your Own QUALCOMM Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your QUALCOMM research is our analysis highlighting 4 key rewards that could impact your investment decision.

- Our free QUALCOMM research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate QUALCOMM's overall financial health at a glance.

Curious About Other Options?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- These 14 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- AI is about to change healthcare. These 24 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The end of cancer? These 26 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if QUALCOMM might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:QCOM

QUALCOMM

Engages in the development and commercialization of foundational technologies for the wireless industry worldwide.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)