- United States

- /

- Semiconductors

- /

- NasdaqGS:MCHP

3 US Stocks Estimated To Trade Up To 48.2% Below Intrinsic Value

Reviewed by Simply Wall St

As the U.S. stock market experiences a boost from the anticipated Santa Claus Rally, with major indices like the Nasdaq Composite and S&P 500 showing gains, investors are keenly observing opportunities that may be undervalued amidst this positive momentum. In such a climate, identifying stocks trading below their intrinsic value can offer potential for growth, making them attractive considerations for those looking to capitalize on market inefficiencies.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Clear Secure (NYSE:YOU) | $27.29 | $53.16 | 48.7% |

| Argan (NYSE:AGX) | $143.57 | $279.09 | 48.6% |

| Western Alliance Bancorporation (NYSE:WAL) | $84.75 | $165.15 | 48.7% |

| Lamb Weston Holdings (NYSE:LW) | $63.69 | $125.18 | 49.1% |

| HealthEquity (NasdaqGS:HQY) | $95.68 | $189.22 | 49.4% |

| LifeMD (NasdaqGM:LFMD) | $4.91 | $9.75 | 49.6% |

| Progress Software (NasdaqGS:PRGS) | $66.26 | $129.49 | 48.8% |

| Freshpet (NasdaqGM:FRPT) | $145.17 | $283.12 | 48.7% |

| WEX (NYSE:WEX) | $171.67 | $332.99 | 48.4% |

| South Atlantic Bancshares (OTCPK:SABK) | $15.45 | $29.97 | 48.4% |

Let's take a closer look at a couple of our picks from the screened companies.

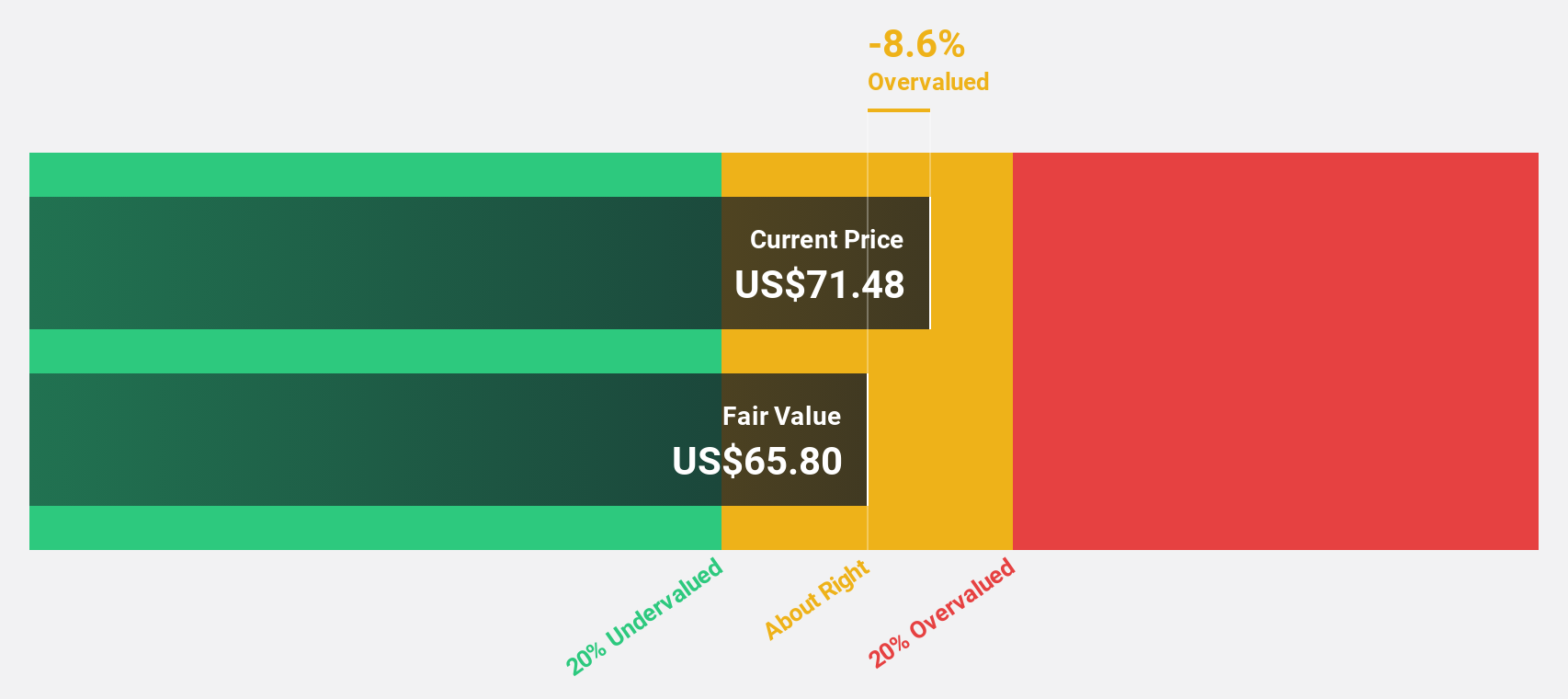

Microchip Technology (NasdaqGS:MCHP)

Overview: Microchip Technology Incorporated develops, manufactures, and sells smart, connected, and secure embedded control solutions across the Americas, Europe, and Asia with a market cap of approximately $31.45 billion.

Operations: The company's revenue segments include Technology Licensing, generating $103.90 million, and Semiconductor Products, contributing $5.39 billion.

Estimated Discount To Fair Value: 48.2%

Microchip Technology's stock is trading at US$58.56, significantly below its estimated fair value of US$113.09, suggesting potential undervaluation based on discounted cash flow analysis. Despite high debt levels and declining profit margins from 28.1% to 14.2%, earnings are expected to grow substantially at 31.6% annually, outpacing the broader U.S. market's growth forecast of 15.3%. Recent product innovations in touch controllers and FPGA solutions highlight strategic advancements in key technological areas.

- Our earnings growth report unveils the potential for significant increases in Microchip Technology's future results.

- Get an in-depth perspective on Microchip Technology's balance sheet by reading our health report here.

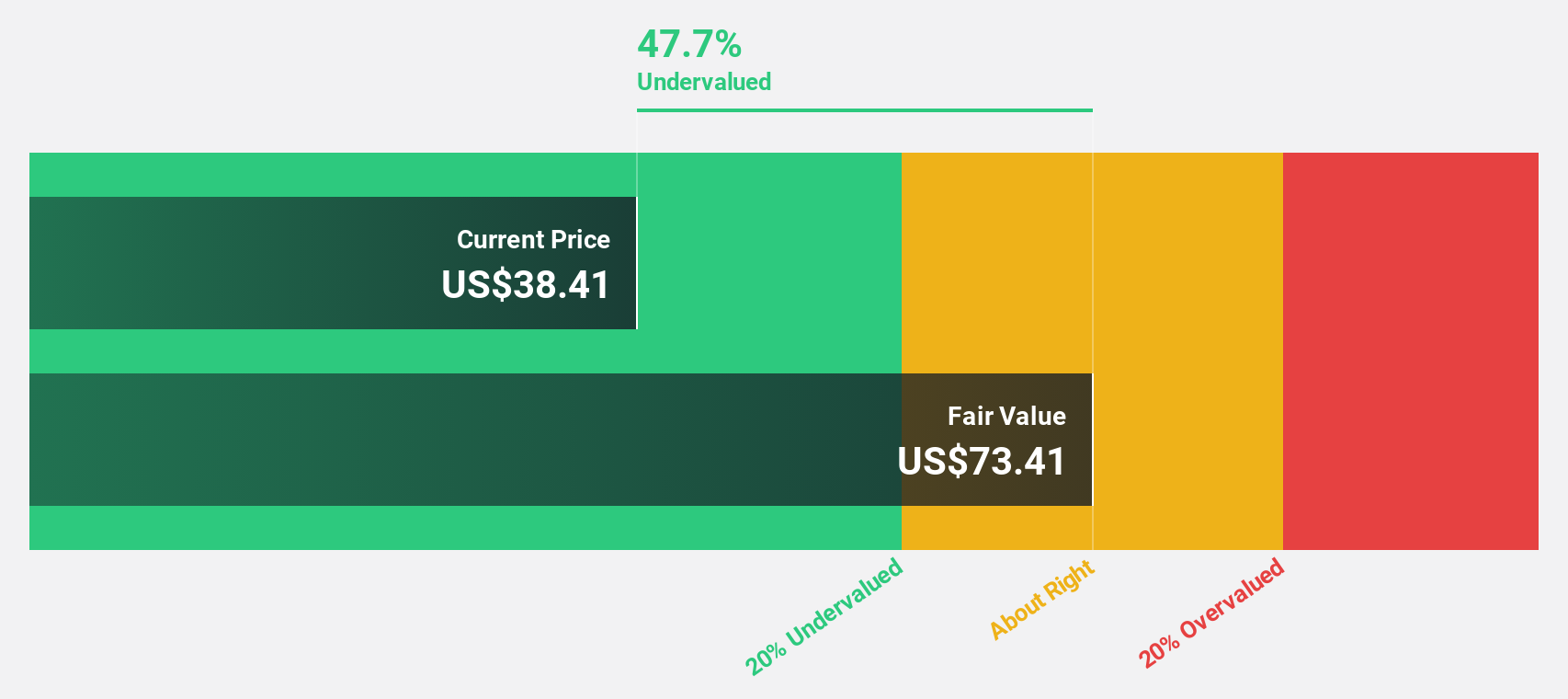

Hess Midstream (NYSE:HESM)

Overview: Hess Midstream LP owns, develops, operates, and acquires midstream assets to provide fee-based services to Hess and third-party customers in the United States, with a market cap of $8.07 billion.

Operations: The company's revenue segments consist of Gathering at $780.40 million, Processing and Storage at $555 million, and Terminaling and Export at $120.70 million.

Estimated Discount To Fair Value: 31.6%

Hess Midstream is trading at US$37.30, significantly below its estimated fair value of US$54.50, highlighting potential undervaluation based on discounted cash flow analysis. Despite a high debt level and dividends not fully covered by earnings or free cash flows, earnings are expected to grow substantially at 60.4% annually, surpassing the U.S. market's growth forecast of 15.2%. The company remains focused on strategic bolt-on acquisitions to enhance its position in the basin.

- Upon reviewing our latest growth report, Hess Midstream's projected financial performance appears quite optimistic.

- Delve into the full analysis health report here for a deeper understanding of Hess Midstream.

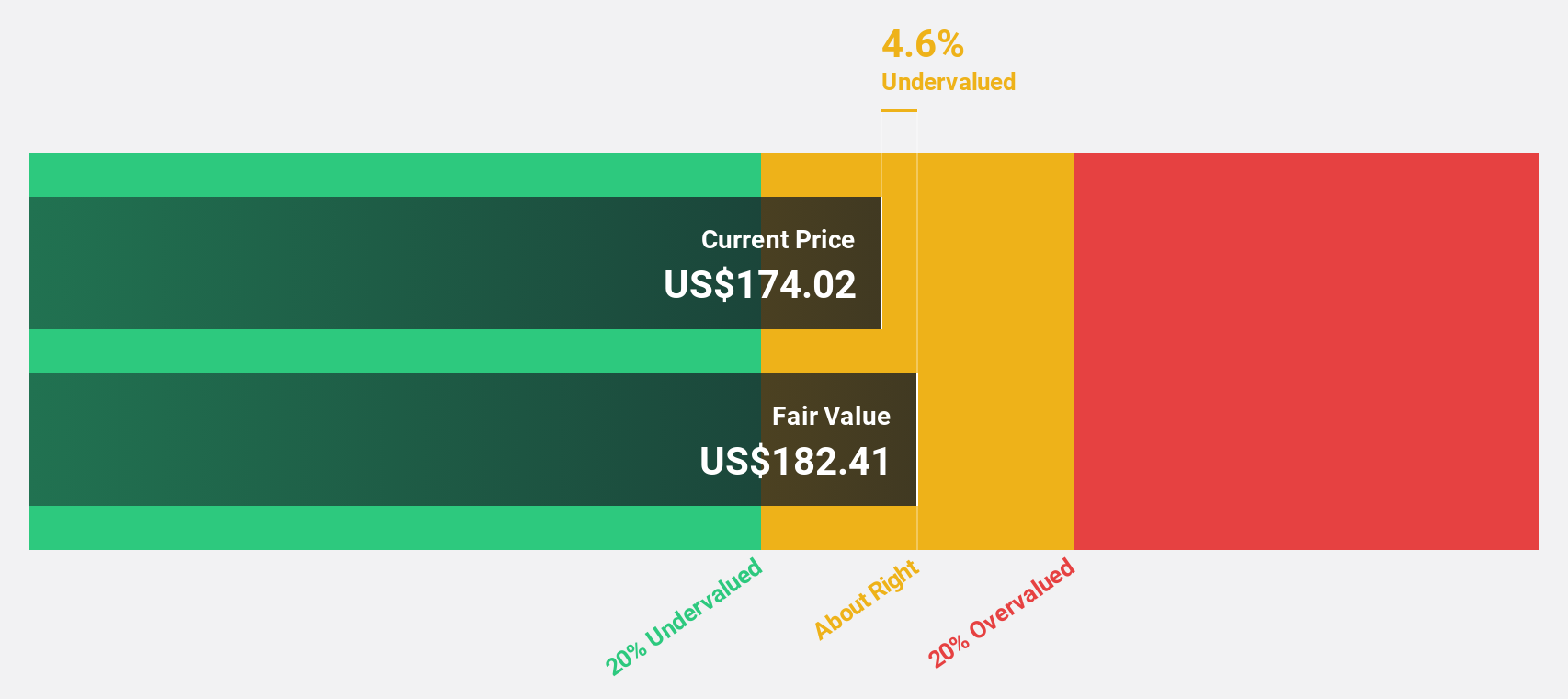

Oracle (NYSE:ORCL)

Overview: Oracle Corporation provides products and services for enterprise information technology environments globally, with a market cap of approximately $479.43 billion.

Operations: The company's revenue segments include Cloud and License at $46.68 billion, Services at $5.27 billion, and Hardware at $2.98 billion.

Estimated Discount To Fair Value: 38.3%

Oracle is trading at US$171.41, significantly below its estimated fair value of US$277.94, suggesting potential undervaluation based on cash flow analysis. Recent client wins in healthcare and public sector applications may enhance future cash flows. Despite high debt levels, Oracle's earnings are forecast to grow at 16.6% annually, outpacing the U.S. market's growth rate of 15.3%. The company's strategic focus includes expanding cloud services and leveraging AI capabilities across various sectors.

- In light of our recent growth report, it seems possible that Oracle's financial performance will exceed current levels.

- Click here and access our complete balance sheet health report to understand the dynamics of Oracle.

Next Steps

- Discover the full array of 174 Undervalued US Stocks Based On Cash Flows right here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:MCHP

Microchip Technology

Engages in the development, manufacture, and sale of smart, connected, and secure embedded control solutions in the Americas, Europe, and Asia.

High growth potential average dividend payer.