- United States

- /

- Semiconductors

- /

- NasdaqGS:LSCC

Does Lattice Semiconductor (NASDAQ:LSCC) Deserve A Spot On Your Watchlist?

For beginners, it can seem like a good idea (and an exciting prospect) to buy a company that tells a good story to investors, even if it currently lacks a track record of revenue and profit. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses. A loss-making company is yet to prove itself with profit, and eventually the inflow of external capital may dry up.

So if this idea of high risk and high reward doesn't suit, you might be more interested in profitable, growing companies, like Lattice Semiconductor (NASDAQ:LSCC). While this doesn't necessarily speak to whether it's undervalued, the profitability of the business is enough to warrant some appreciation - especially if its growing.

See our latest analysis for Lattice Semiconductor

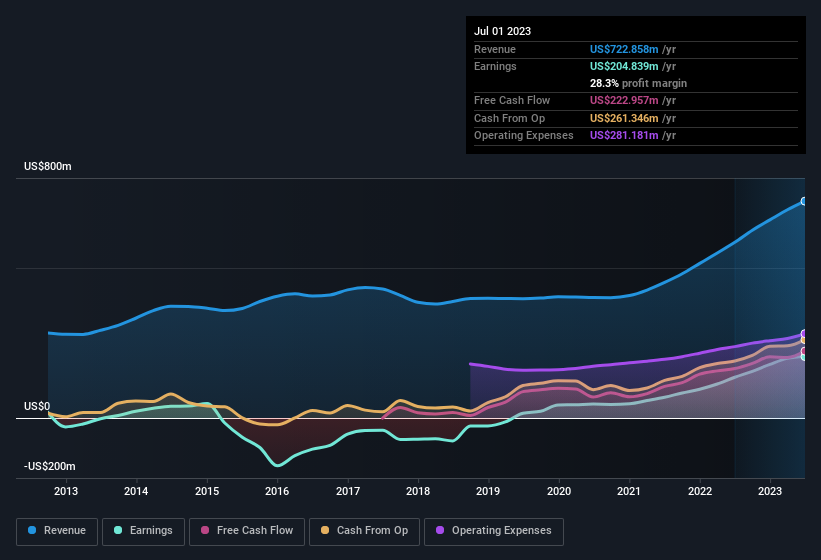

Lattice Semiconductor's Improving Profits

In the last three years Lattice Semiconductor's earnings per share took off; so much so that it's a bit disingenuous to use these figures to try and deduce long term estimates. As a result, we'll zoom in on growth over the last year, instead. Lattice Semiconductor's EPS skyrocketed from US$0.99 to US$1.49, in just one year; a result that's bound to bring a smile to shareholders. That's a fantastic gain of 50%.

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. Lattice Semiconductor shareholders can take confidence from the fact that EBIT margins are up from 25% to 30%, and revenue is growing. Both of which are great metrics to check off for potential growth.

The chart below shows how the company's bottom and top lines have progressed over time. To see the actual numbers, click on the chart.

In investing, as in life, the future matters more than the past. So why not check out this free interactive visualization of Lattice Semiconductor's forecast profits?

Are Lattice Semiconductor Insiders Aligned With All Shareholders?

We would not expect to see insiders owning a large percentage of a US$12b company like Lattice Semiconductor. But we are reassured by the fact they have invested in the company. Indeed, they have a considerable amount of wealth invested in it, currently valued at US$163m. This suggests that leadership will be very mindful of shareholders' interests when making decisions!

Is Lattice Semiconductor Worth Keeping An Eye On?

If you believe that share price follows earnings per share you should definitely be delving further into Lattice Semiconductor's strong EPS growth. Further, the high level of insider ownership is impressive and suggests that the management appreciates the EPS growth and has faith in Lattice Semiconductor's continuing strength. Fast growth and confident insiders should be enough to warrant further research, so it would seem that it's a good stock to follow. Another important measure of business quality not discussed here, is return on equity (ROE). Click on this link to see how Lattice Semiconductor shapes up to industry peers, when it comes to ROE.

There's always the possibility of doing well buying stocks that are not growing earnings and do not have insiders buying shares. But for those who consider these important metrics, we encourage you to check out companies that do have those features. You can access a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

If you're looking to trade Lattice Semiconductor, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:LSCC

Lattice Semiconductor

Develops and sells semiconductor products in Asia, Europe, and the Americas.

Flawless balance sheet with high growth potential.