Dillard's (DDS) Valuation Check After 20% Monthly Surge and 70% One-Year Total Return

Reviewed by Simply Wall St

Dillard's (DDS) shares have quietly powered higher this year, and the latest leg of the rally has investors asking whether a traditional department store can really justify this kind of premium valuation.

See our latest analysis for Dillard's.

With the share price now around $730.73 after a 1 month share price return of nearly 20 percent and a 1 year total shareholder return close to 70 percent, momentum looks firmly intact as investors reassess the risks around a legacy retailer that keeps defying expectations.

If Dillard's surge has you rethinking what qualifies as a compelling opportunity, it is worth exploring other retail names and beyond using fast growing stocks with high insider ownership.

Yet with revenue barely growing, earnings slipping, and the share price now well above Wall Street targets, investors face a dilemma: does Dillard's still offer upside from here, or is the market already banking on years of future growth?

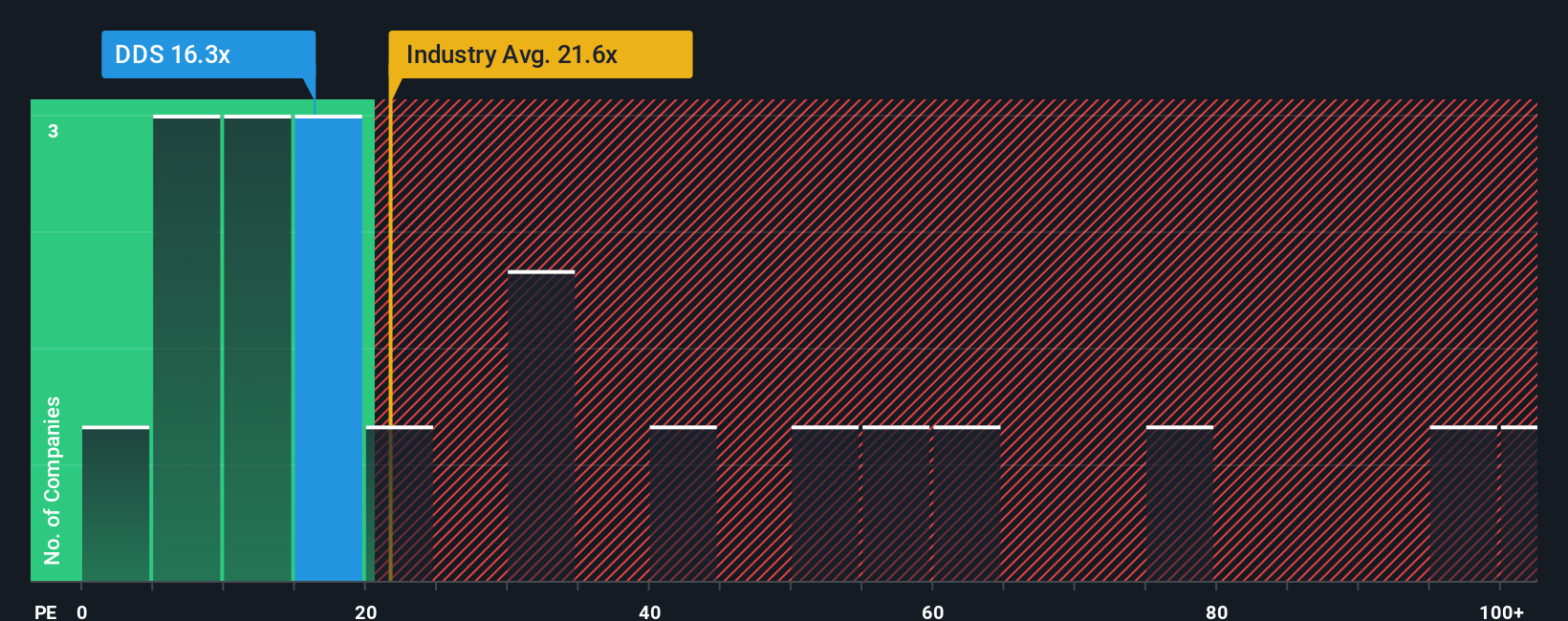

Price-to-Earnings of 19.6x: Is it justified?

Dillard's is trading on a price-to-earnings ratio of 19.6 times, a level that looks stretched against both its own fundamentals and its estimated fair valuation.

The price to earnings multiple compares what investors are paying today for each dollar of current earnings. It is a core lens for mature, profitable retailers like Dillard's. With earnings forecast to decline by an average of 2.7 percent per year over the next three years, a rich multiple suggests the market is paying up for stability, capital returns and brand resilience rather than growth, and that optimism has already pushed the shares well above both analyst targets and our DCF fair value of 519.86 dollars.

Against this backdrop, Dillard's 19.6 times earnings looks expensive when set beside its own fair price to earnings estimate of 14 times. Our fair ratio work implies the market could ultimately gravitate toward this level. Yet versus the broader Global Multiline Retail industry average of 19.9 times and a peer group average of 20.9 times, Dillard's trades at a slight discount, suggesting investors are pricing its earnings more conservatively than many rivals even after the rally.

Explore the SWS fair ratio for Dillard's

Result: Price-to-Earnings of 19.6x (OVERVALUED)

However, investors still face key risks, including slowing earnings and the stock trading well above analyst and intrinsic value estimates, which leaves sentiment vulnerable.

Find out about the key risks to this Dillard's narrative.

Another View on Value

While the current price to earnings ratio looks rich versus Dillard's fair ratio of 14 times, it still sits slightly below the Global Multiline Retail average of 19.9 times and peers at 20.9 times, suggesting less extreme optimism than the headline premium might imply.

See what the numbers say about this price — find out in our valuation breakdown.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Dillard's for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 907 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Dillard's Narrative

If you would rather dig into the numbers yourself and challenge these conclusions, you can shape a personalised view in just a few minutes, Do it your way.

A great starting point for your Dillard's research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Ready for your next investing move?

If you stop at Dillard's, you could miss compelling opportunities elsewhere. Use the Simply Wall Street Screener to uncover targeted ideas aligned with your strategy.

- Capture potential long term compounding by focusing on these 12 dividend stocks with yields > 3%, which may steadily boost your income as payouts grow over time.

- Explore innovation at the edge of medicine with these 30 healthcare AI stocks, where advances in diagnostics and treatment might offer differentiated exposure to the healthcare sector.

- Position yourself in the evolving digital landscape through these 81 cryptocurrency and blockchain stocks, targeting businesses building real world applications on blockchain and decentralized finance.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:DDS

Dillard's

Operates retail department stores in the southeastern, southwestern, and midwestern areas of the United States.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Deep Value Multi Bagger Opportunity

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Unicycive Therapeutics (Nasdaq: UNCY) – Preparing for a Second Shot at Bringing a New Kidney Treatment to Market (TEST)

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026