- United States

- /

- Specialty Stores

- /

- NasdaqGS:ROST

Ross Stores (NasdaqGS:ROST) Increases Dividend 10 Percent As Revenue Sees US$5,912 Million And Earnings Guidance

Reviewed by Simply Wall St

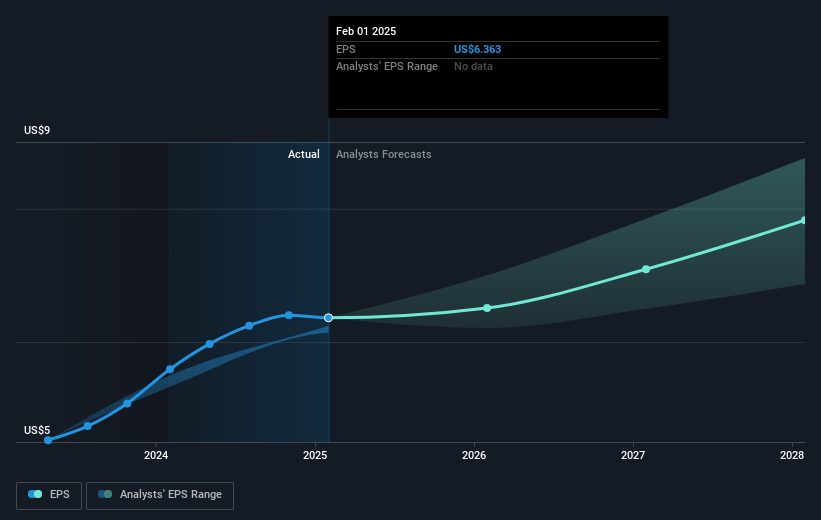

Ross Stores (NasdaqGS:ROST) saw a slight dip in its share price, moving -0.35% over the last week despite a 10% dividend increase to $0.405 per share announced on March 4, 2025. This adjustment might not have significantly boosted investor sentiment, as the company simultaneously reported mixed earnings for the fourth quarter, with net income and EPS both marginally down from the previous year. Furthermore, Ross Stores provided a cautionary corporate guidance for the upcoming fiscal periods, suggesting potential headwinds with a projected sales decline of up to 3%. Against a backdrop of overall market volatility, where major stock indexes were oscillating between gains and losses due to tariff discussions and mixed economic signals, the modest decline in ROST’s stock performance aligns with broader market movements. Over the same period, the market registered a 3.1% drop, illustrating the pressure on retail stocks amidst tariff-related uncertainties and economic data reactions.

Unlock comprehensive insights into our analysis of Ross Stores stock here.

Over the past three years, Ross Stores (NasdaqGS:ROST) delivered a total return of 64.00%, buoyed by a consistent upward trend in both earnings and dividends. Notably, the company's earnings grew at an impressive rate, climbing by 16.5% per year over this period. This robust performance was supported by a remarkable return on equity, which remains outstanding at 40.2%, indicating efficient use of shareholders' equity in generating profits.

Throughout this period, ROST's performance stood out compared to its industry, particularly as its earnings growth surpassed the Specialty Retail industry's decline of 8.6%. Additionally, Ross Stores made strategic decisions such as regular dividend affirmations and increases, providing further returns to shareholders and building investor confidence. However, despite these positive outcomes over three years, ROST underperformed the market in the past year, where the overall market gained 13.1%, likely due to more recent mixed earnings reports and cautious future guidance.

- Get the full picture of Ross Stores' valuation metrics and investment prospects—click to explore.

- Assess the potential risks impacting Ross Stores' growth trajectory—explore our risk evaluation report.

- Is Ross Stores part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ROST

Ross Stores

Operates off-price retail apparel and home fashion stores under the Ross Dress for Less and dd’s DISCOUNTS brand names in the United States.

Outstanding track record with excellent balance sheet.