JD.com (NasdaqGS:JD) Reports Revenue Rise to ¥301 Billion and Net Income Growth

Reviewed by Simply Wall St

JD.com (NasdaqGS:JD) recently reported substantial year-over-year growth in its Q1 2025 earnings, with revenue increasing to CNY 301,082 million and net income rising to CNY 10,890 million, alongside a rise in both basic and diluted EPS. These positive earnings results contributed weight to JD.com's 9% price increase over the past week, in line with market trends which saw a 4% rise. Such financial performance reflects positively on investor sentiment, underpinning the company's upward price movement and aligning with broader positive market conditions.

Buy, Hold or Sell JD.com? View our complete analysis and fair value estimate and you decide.

The recent earnings report for JD.com and its price hike highlight the company's resilience and ability to capitalize on favorable market conditions. Over the last year, JD.com’s total return was 14.92%, reflecting a robust performance even as it aligned with broader industry trends. Within the past year, JD.com outperformed the US Multiline Retail industry but marginally lagged the US market, showcasing its competitive position amidst industry challenges.

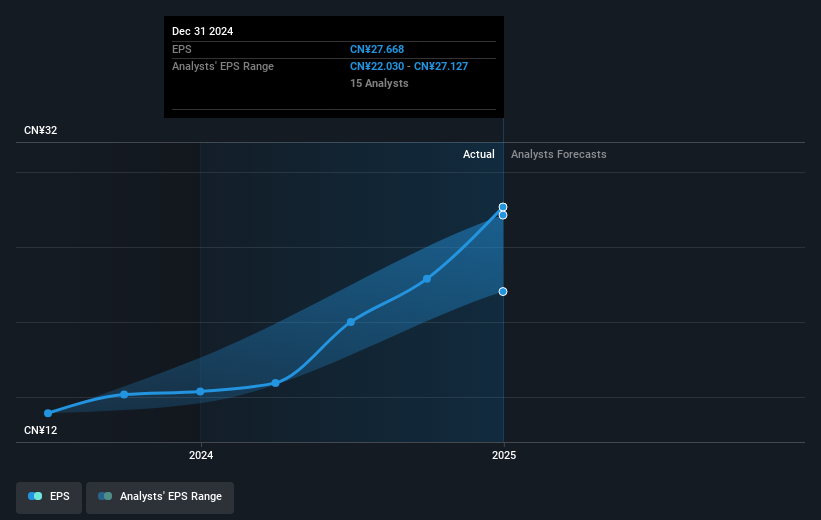

The substantial revenue and net income growth reported in Q1 2025 suggest positive implications for future revenue and earnings forecasts. Enhanced supply chain efficiency and strategic involvement in AI and robotics could further bolster JD.com's market position, aligning with their growth ambitions in the electronics and home appliances sectors. These developments may spurn revenue growth beyond current forecasts, which anticipate a gradual increase at 6.4% annually over the next three years.

Current analyst consensus sets JD.com's price target at $54.47, significantly higher than its present share price of $34.06. Such a gap underscores the positive sentiment around the company's earnings trajectory. To bridge this gap, JD.com must sustain its growth momentum and enhance profit margins through expected supply chain optimizations and market expansions, potentially leading to a revaluation of shares closer to the target price. Investors should weigh these factors against current and future market conditions to assess potential impacts on their holdings.

Assess JD.com's future earnings estimates with our detailed growth reports.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:JD

JD.com

Operates as a supply chain-based technology and service provider in the People’s Republic of China.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Salesforce Stock: AI-Fueled Growth Is Real — But Can Margins Stay This Strong?

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)