Is JD.com Now a Bargain After Its Prolonged Share Price Slide?

Reviewed by Bailey Pemberton

- Wondering if JD.com is finally a bargain after years of volatility? In this article we walk through whether the current price really reflects the value of the underlying business.

- Despite a modest pullback of 2.9% over the last week and 1.6% over the past month, the bigger story is the long slide, with the stock down 15.7% year to date and 20.4% over the last year, and far more over 3 and 5 years.

- Recent headlines have focused on JD.com's ongoing push to streamline operations and sharpen its focus on core retail and logistics, alongside broader market debates about the long term prospects of Chinese tech platforms. At the same time, shifts in investor sentiment toward Chinese equities generally have kept risk perceptions elevated, even as JD.com continues to invest in infrastructure and service quality.

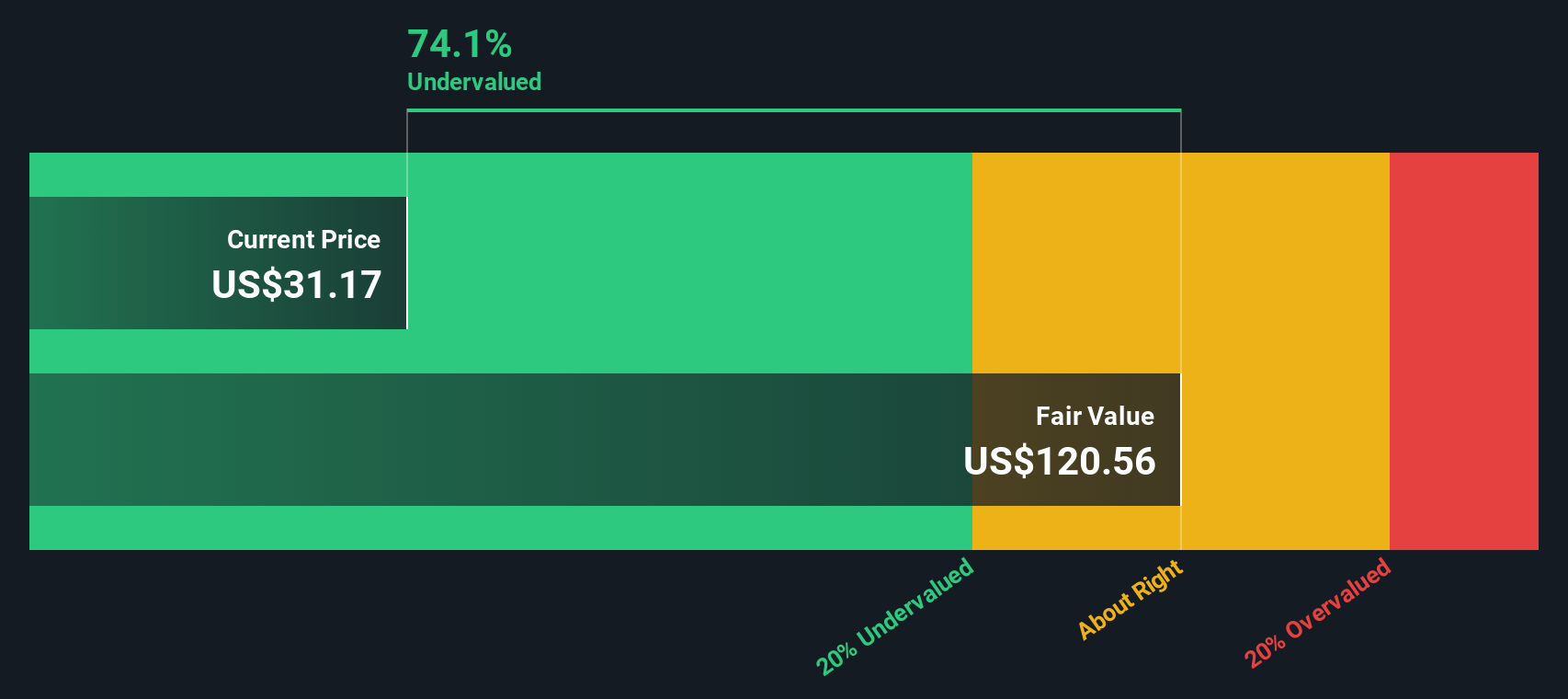

- Based on Simply Wall St's six point valuation framework, JD.com currently scores a 5 out of 6, suggesting it screens as undervalued on most checks. Next we break down what different valuation approaches say about the stock today, and later explore an additional way to think about its worth beyond the numbers alone.

Find out why JD.com's -20.4% return over the last year is lagging behind its peers.

Approach 1: JD.com Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business is worth by projecting the cash it can generate in the future and discounting those cash flows back to today.

For JD.com, the latest twelve month free cash flow is slightly negative at about CN¥0.23 billion, which means the company is currently reinvesting heavily rather than generating surplus cash. Analysts expect this to improve significantly, with Simply Wall St aggregating forecasts and extrapolating them beyond the typical five year window. Under the 2 Stage Free Cash Flow to Equity approach, free cash flow is projected to reach roughly CN¥49.90 billion by 2028, and then grow at more moderate rates over the following years.

When all these future cash flows are discounted back to today in CN¥ terms, the model implies an intrinsic value of about $54.62 per share. Compared with the current share price, this suggests JD.com is trading at roughly a 47.2% discount.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests JD.com is undervalued by 47.2%. Track this in your watchlist or portfolio, or discover 910 more undervalued stocks based on cash flows.

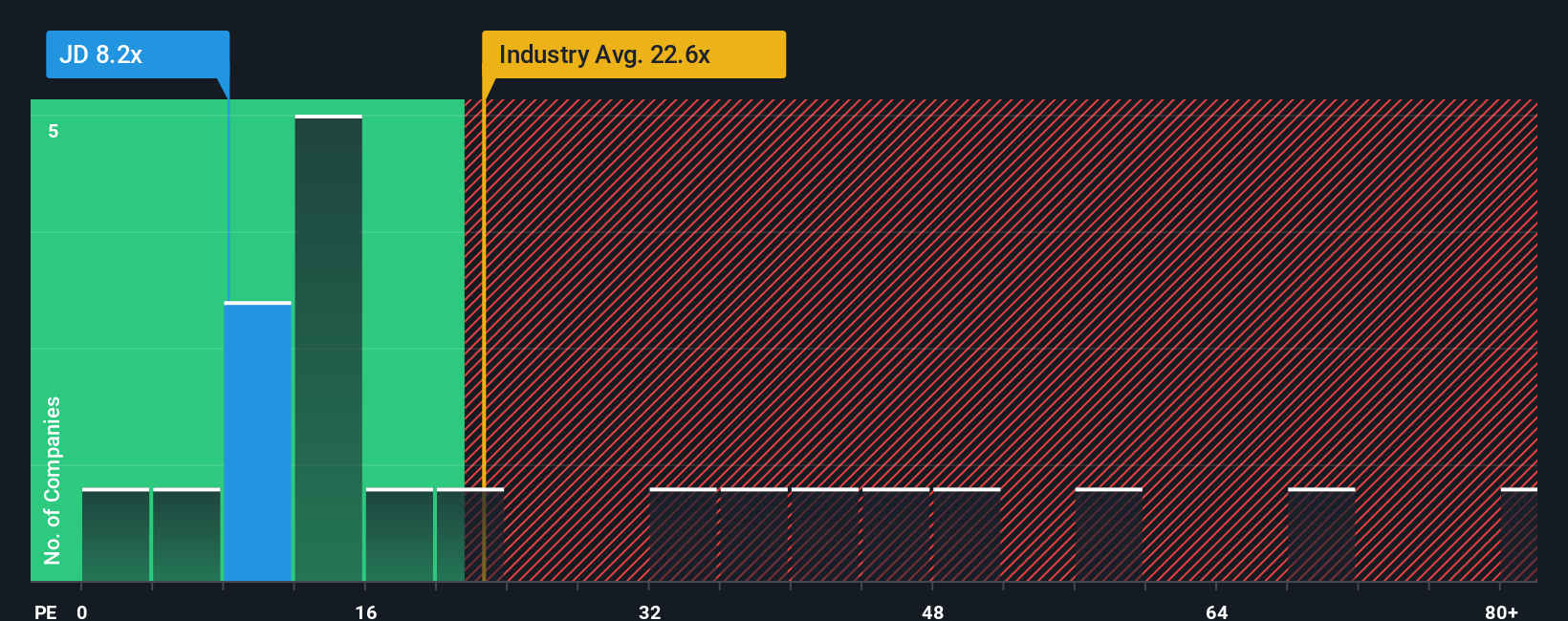

Approach 2: JD.com Price vs Earnings

For profitable businesses like JD.com, the price to earnings, or PE, ratio is a useful way to gauge how much investors are paying for each dollar of current earnings. In general, companies with stronger growth prospects or lower perceived risk can justify a higher PE, while slower growth or higher uncertainty usually calls for a lower, more conservative multiple.

JD.com currently trades on a PE of about 9.0x, which is well below both the Multiline Retail industry average of roughly 19.7x and the broader peer group average of about 56.2x. Simply Wall St also calculates a Fair Ratio of around 24.1x for JD.com, a proprietary estimate of what its PE should be given its earnings growth profile, industry, profit margins, market cap and specific risk factors. Compared with simple peer or sector comparisons, this Fair Ratio is more tailored to JD.com’s fundamentals and risk reward mix, rather than assuming it should look like the average company.

With JD.com’s actual PE of 9.0x sitting significantly below the estimated Fair Ratio of 24.1x, the shares appear materially undervalued on this earnings based view.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1457 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your JD.com Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple tool on Simply Wall St’s Community page that lets you turn your view of JD.com into a structured story. It does this by linking your assumptions about its future revenue, earnings and margins to a forecast and a fair value, then comparing that fair value to today’s price. The platform dynamically updates those Narratives as new news or earnings arrive. For example, one investor might build a bullish JD.com Narrative around strong user growth, logistics advantages and international expansion that supports a fair value closer to the upper analyst target of about $60 per share. Another might focus on competition, rising costs and geopolitical risk and land near the lower end, closer to $28. This gives you a clear side by side view of how different stories lead to different numbers and helps you choose the one that best matches your own conviction.

Do you think there's more to the story for JD.com? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:JD

JD.com

Operates as a supply chain-based technology and service provider in the People’s Republic of China.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)