- United States

- /

- General Merchandise and Department Stores

- /

- NasdaqGS:AMZN

Results: Amazon.com, Inc. Beat Earnings Expectations And Analysts Now Have New Forecasts

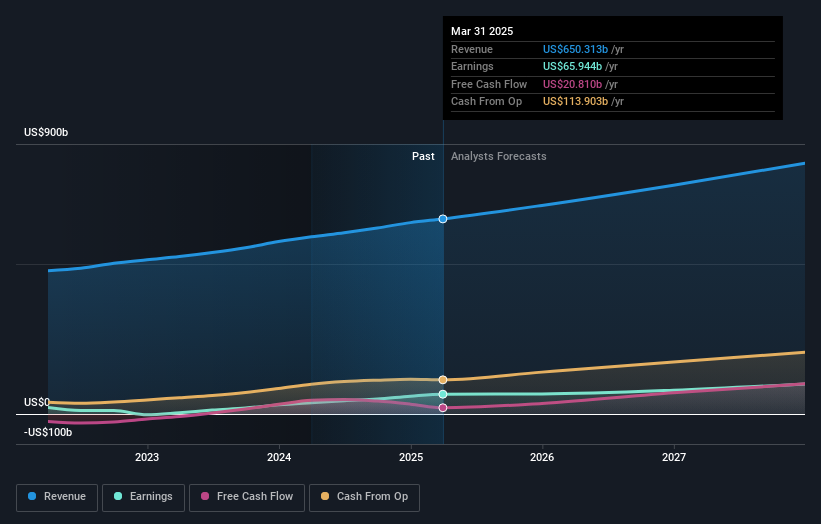

As you might know, Amazon.com, Inc. (NASDAQ:AMZN) recently reported its first-quarter numbers. Revenues were US$156b, approximately in line with expectations, although statutory earnings per share (EPS) performed substantially better. EPS of US$1.59 were also better than expected, beating analyst predictions by 16%. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

We check all companies for important risks. See what we found for Amazon.com in our free report.

Taking into account the latest results, the current consensus from Amazon.com's 65 analysts is for revenues of US$695.3b in 2025. This would reflect a credible 6.9% increase on its revenue over the past 12 months. Statutory per share are forecast to be US$6.18, approximately in line with the last 12 months. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$694.9b and earnings per share (EPS) of US$6.23 in 2025. The consensus analysts don't seem to have seen anything in these results that would have changed their view on the business, given there's been no major change to their estimates.

See our latest analysis for Amazon.com

There were no changes to revenue or earnings estimates or the price target of US$240, suggesting that the company has met expectations in its recent result. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. The most optimistic Amazon.com analyst has a price target of US$288 per share, while the most pessimistic values it at US$195. As you can see, analysts are not all in agreement on the stock's future, but the range of estimates is still reasonably narrow, which could suggest that the outcome is not totally unpredictable.

Of course, another way to look at these forecasts is to place them into context against the industry itself. We would highlight that Amazon.com's revenue growth is expected to slow, with the forecast 9.3% annualised growth rate until the end of 2025 being well below the historical 13% p.a. growth over the last five years. Juxtapose this against the other companies in the industry with analyst coverage, which are forecast to grow their revenues (in aggregate) 8.9% annually. So it's pretty clear that, while Amazon.com's revenue growth is expected to slow, it's expected to grow roughly in line with the industry.

The Bottom Line

The most important thing to take away is that there's been no major change in sentiment, with the analysts reconfirming that the business is performing in line with their previous earnings per share estimates. They also reconfirmed their revenue estimates, with the company predicted to grow at about the same rate as the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. We have estimates - from multiple Amazon.com analysts - going out to 2027, and you can see them free on our platform here.

You can also see our analysis of Amazon.com's Board and CEO remuneration and experience, and whether company insiders have been buying stock.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:AMZN

Amazon.com

Engages in the retail sale of consumer products, advertising, and subscriptions service through online and physical stores in North America and internationally.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion