- United States

- /

- Retail REITs

- /

- NYSE:SPG

Why Simon Property Group, Inc.'s (NYSE:SPG) CEO Pay Matters To You

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

In 1995 David Simon was appointed CEO of Simon Property Group, Inc. (NYSE:SPG). First, this article will compare CEO compensation with compensation at other large companies. After that, we will consider the growth in the business. And finally - as a second measure of performance - we will look at the returns shareholders have received over the last few years. This method should give us information to assess how appropriately the company pays the CEO.

Check out our latest analysis for Simon Property Group

How Does David Simon's Compensation Compare With Similar Sized Companies?

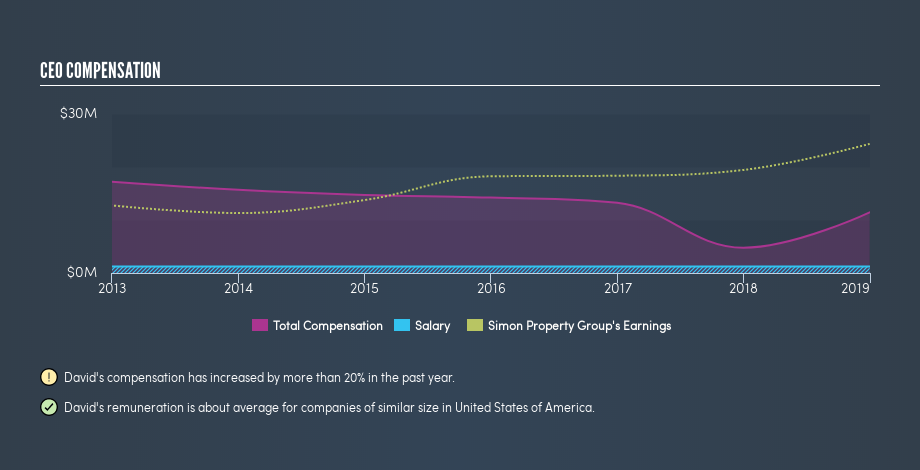

Our data indicates that Simon Property Group, Inc. is worth US$64b, and total annual CEO compensation is US$11m. (This number is for the twelve months until December 2018). That's a notable increase of 140% on last year. While we always look at total compensation first, we note that the salary component is less, at US$1.3m. We looked at a group of companies with market capitalizations over US$8.0b and the median CEO total compensation was US$11m. There aren't very many mega-cap companies, so we had to take a wide range to get a meaningful comparison figure.

So David Simon receives a similar amount to the median CEO pay, amongst the companies we looked at. While this data point isn't particularly informative alone, it gains more meaning when considered with business performance.

The graphic below shows how CEO compensation at Simon Property Group has changed from year to year.

Is Simon Property Group, Inc. Growing?

On average over the last three years, Simon Property Group, Inc. has grown earnings per share (EPS) by 10% each year (using a line of best fit). It achieved revenue growth of 1.8% over the last year.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. It's also good to see modest revenue growth, suggesting the underlying business is healthy. It could be important to check this free visual depiction of what analysts expect for the future.

Has Simon Property Group, Inc. Been A Good Investment?

With a three year total loss of 2.4%, Simon Property Group, Inc. would certainly have some dissatisfied shareholders. This suggests it would be unwise for the company to pay the CEO too generously.

In Summary...

David Simon is paid around what is normal the leaders of larger companies.

We think that the EPS growth is very pleasing, but we cannot say the same about the lacklustre shareholder returns (over the last three years). Considering the the positives we don't think the CEO pays is too high, but it's certainly hard to argue it is too low. So you may want to check if insiders are buying Simon Property Group shares with their own money (free access).

If you want to buy a stock that is better than Simon Property Group, this freelist of high return, low debt companies is a great place to look.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About NYSE:SPG

Simon Property Group

Simon Property Group, Inc. (NYSE:SPG) is a self-administered and self-managed real estate investment trust (“REIT”).

Undervalued established dividend payer.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Hitit Bilgisayar Hizmetleri will achieve a 19.7% revenue boost in the next five years

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)