Advertisement

- United States

- /

- Interactive Media and Services

- /

- NasdaqGS:VMEO

Exploring Undervalued Small Caps With Insider Buying In US November 2024

Simply Wall St

Reviewed by Simply Wall St

The United States market has experienced a robust performance, with a 5.1% increase over the last week and a remarkable 38% climb in the past year. In this thriving environment, identifying stocks that are potentially undervalued while exhibiting insider buying can offer intriguing opportunities for investors seeking to capitalize on expected earnings growth.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| ChoiceOne Financial Services | 12.7x | 3.6x | 49.66% | ★★★★★☆ |

| Hanover Bancorp | 10.2x | 2.3x | 42.44% | ★★★★★☆ |

| HighPeak Energy | 10.8x | 1.6x | 37.83% | ★★★★★☆ |

| Franklin Financial Services | 10.3x | 2.0x | 32.39% | ★★★★☆☆ |

| German American Bancorp | 16.1x | 5.4x | 40.91% | ★★★☆☆☆ |

| Douglas Dynamics | 10.9x | 1.1x | -18.03% | ★★★☆☆☆ |

| Citizens & Northern | 14.2x | 3.0x | 39.90% | ★★★☆☆☆ |

| Orion Group Holdings | NA | 0.4x | -212.54% | ★★★☆☆☆ |

| Community West Bancshares | 18.7x | 2.9x | 42.25% | ★★★☆☆☆ |

| Delek US Holdings | NA | 0.1x | -60.78% | ★★★☆☆☆ |

Let's dive into some prime choices out of from the screener.

German American Bancorp (NasdaqGS:GABC)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: German American Bancorp is a financial services company providing banking, insurance, and investment services primarily in Indiana and Kentucky, with a market cap of approximately $1.13 billion.

Operations: GABC's revenue has shown a general upward trend from $91.78 million in December 2013 to $247.16 million by September 2024, with a gross profit margin consistently at 100%. Operating expenses have increased over time, with general and administrative expenses being the largest component, rising from $43.64 million in December 2013 to $113.96 million by September 2024. The net income margin has varied, reaching as high as 37.62% in September 2021 and most recently recorded at approximately 33.22% in September 2024.

PE: 16.1x

German American Bancorp's recent earnings report for Q3 2024 shows steady net interest income at US$48.59 million, slightly up from US$47.56 million a year prior, though net income dipped to US$21.05 million from US$21.45 million. The company maintains insider confidence with consistent dividend payouts, declaring a cash dividend of $0.27 per share payable on November 20, 2024. Despite no recent share repurchases, earnings are projected to grow annually by 22.67%, indicating potential for future value appreciation in the market.

- Click to explore a detailed breakdown of our findings in German American Bancorp's valuation report.

Understand German American Bancorp's track record by examining our Past report.

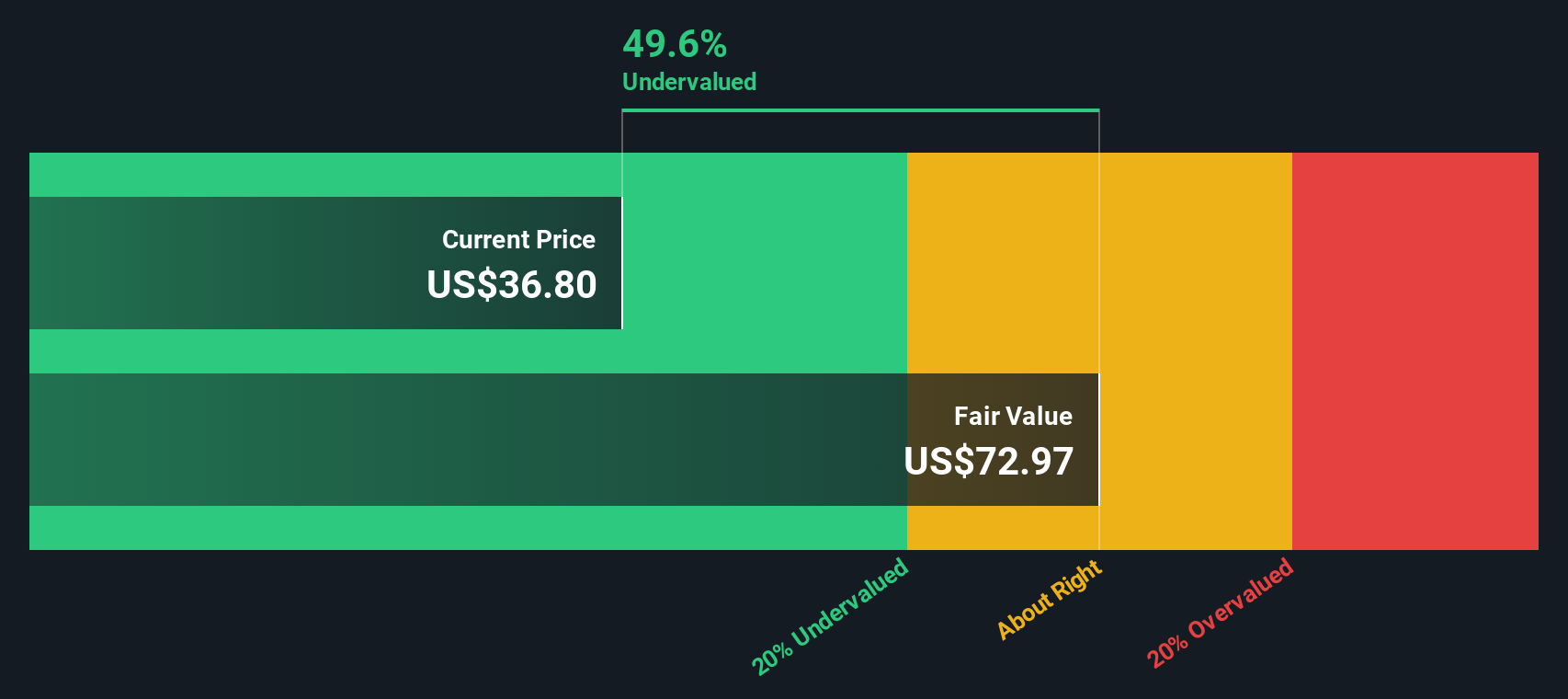

Vimeo (NasdaqGS:VMEO)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Vimeo operates as an internet software and services company, focusing on providing video hosting, sharing, and streaming solutions to businesses and individuals, with a market cap of approximately $1.49 billion.

Operations: Vimeo's revenue primarily comes from its Internet Software & Services segment, totaling $419.39 million. The company has experienced a notable improvement in net income margin, reaching 7.92% by September 2024, alongside a gross profit margin of 78.30%. Operating expenses have been reduced over time to $303.20 million as of the latest period, with significant allocations to sales and marketing at $120.48 million and research and development at $105.52 million.

PE: 35.0x

Vimeo's recent earnings report shows a slight dip in third-quarter sales to US$104.56 million from US$106.25 million the previous year, yet net income rose to US$9.28 million from US$8.46 million, indicating improved profitability. The company's growth strategy includes integrating AI capabilities under new leadership with Bob Petrocelli as Chief Product & Technology Officer and Charlie Ungashick as Chief Marketing Officer since September 2024. Insider confidence is evident through share purchases over the past months, suggesting optimism about Vimeo's future prospects despite its volatile share price and reliance on external borrowing for funding.

- Delve into the full analysis valuation report here for a deeper understanding of Vimeo.

Review our historical performance report to gain insights into Vimeo's's past performance.

Pebblebrook Hotel Trust (NYSE:PEB)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Pebblebrook Hotel Trust is a real estate investment trust focused on the ownership and management of upscale, full-service hotels and resorts, with a market capitalization of approximately $2.12 billion.

Operations: The company generates revenue primarily from its hotel and motel operations, with a recent revenue figure of $1.44 billion. The cost of goods sold (COGS) is significant, amounting to $1.07 billion, impacting the gross profit margin which stands at 25.89%. Operating expenses include depreciation and amortization ($238.82 million) and general & administrative expenses ($47.72 million). Net income has been negative recently, with a net income margin of -9.15%.

PE: -12.1x

Pebblebrook Hotel Trust, a smaller player in the hospitality sector, shows potential for value with its recent financial performance. In Q3 2024, they reported sales of US$262.76 million and a net income of US$43.66 million, reversing last year's losses. Insider confidence is evident as Chairman & CEO Jon Bortz purchased 66,000 shares worth approximately US$790,680 recently. However, the company anticipates a net loss for Q4 and full-year 2024 due to primarily external borrowing risks and dividend declarations remaining modest at $0.01 per common share. Earnings are projected to grow annually by nearly 70%, providing some optimism amidst current challenges.

Taking Advantage

- Click through to start exploring the rest of the 39 Undervalued US Small Caps With Insider Buying now.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:VMEO

Vimeo

Provides video software solutions in the United States and internationally.

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor