- United States

- /

- Consumer Durables

- /

- NYSE:SDHC

Three Top Undervalued Small Caps In US With Insider Buying

Reviewed by Simply Wall St

Over the last 7 days, the United States market has risen by 3.8%, contributing to a 24% climb over the past year, with earnings expected to grow by 15% annually. In such a dynamic environment, identifying stocks that are potentially undervalued and have insider buying can be key indicators of promising opportunities for investors seeking growth in small-cap companies.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Plymouth Industrial REIT | 923.3x | 3.9x | 46.76% | ★★★★★☆ |

| German American Bancorp | 14.4x | 4.8x | 49.07% | ★★★★☆☆ |

| Quanex Building Products | 34.4x | 0.9x | 36.87% | ★★★★☆☆ |

| First United | 13.2x | 3.0x | 46.41% | ★★★★☆☆ |

| Franklin Financial Services | 10.4x | 2.0x | 34.40% | ★★★★☆☆ |

| McEwen Mining | 4.3x | 2.2x | 44.01% | ★★★★☆☆ |

| Innovex International | 9.4x | 2.2x | 45.55% | ★★★★☆☆ |

| ProPetro Holding | NA | 0.8x | 9.13% | ★★★☆☆☆ |

| Delek US Holdings | NA | 0.1x | -84.31% | ★★★☆☆☆ |

| Sabre | NA | 0.4x | -65.37% | ★★★☆☆☆ |

Let's explore several standout options from the results in the screener.

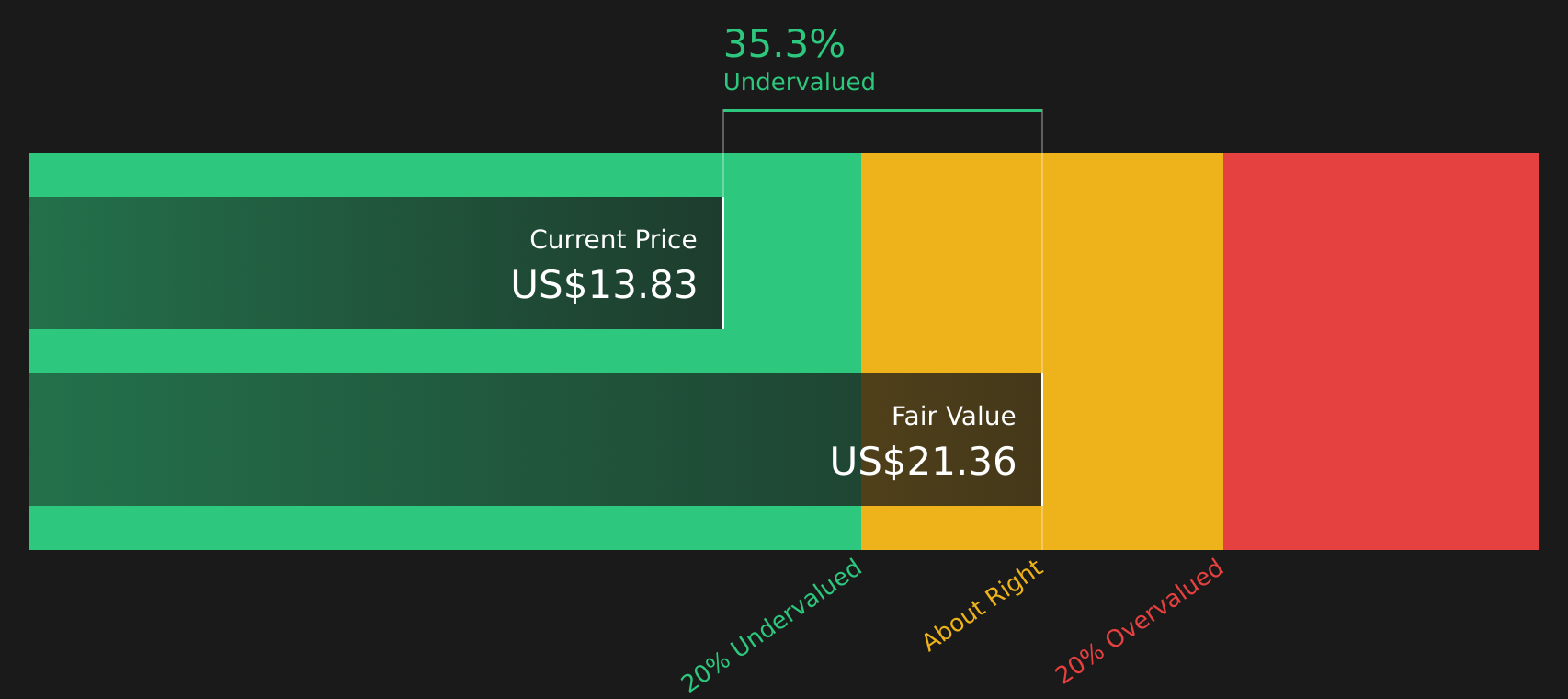

Maravai LifeSciences Holdings (NasdaqGS:MRVI)

Simply Wall St Value Rating: ★★★★★☆

Overview: Maravai LifeSciences Holdings specializes in providing nucleic acid production and biologics safety testing services, with a market capitalization of approximately $2.02 billion.

Operations: Nucleic Acid Production and Biologics Safety Testing are the primary revenue streams. The company has seen fluctuations in its gross profit margin, reaching a peak of 83.35% in early 2022 and declining to 46.36% by late 2024. Operating expenses have consistently been significant, with General & Administrative Expenses being a major component.

PE: -3.3x

Maravai LifeSciences Holdings, a player in the biotech industry, has seen insider confidence with recent share purchases over the past few months. Despite reporting a net loss of US$99 million for Q3 2024 and facing goodwill impairment charges of US$154.24 million, its revenue guidance for 2024 is set between US$255 million to US$265 million. Leadership changes include Trey Martin assuming direct responsibility for Nucleic Acid Production following Andrew Burch's departure. The company’s reliance on external borrowing adds risk but also potential growth opportunities in its niche market space.

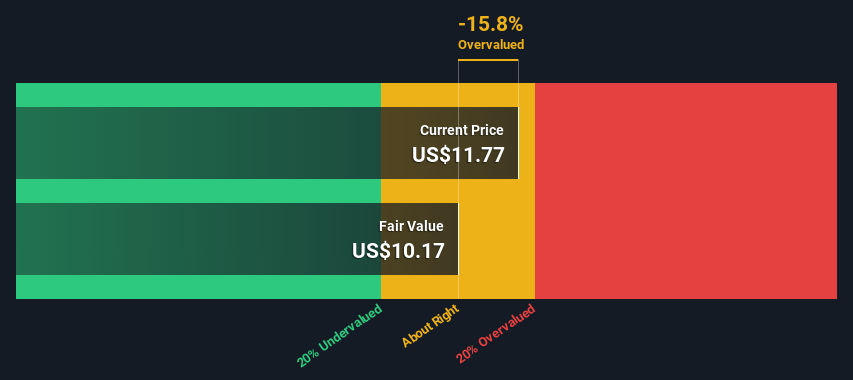

Manitowoc Company (NYSE:MTW)

Simply Wall St Value Rating: ★★★★★☆

Overview: Manitowoc Company is a leading global manufacturer of cranes and lifting solutions, with operations spanning the Americas, Europe and Africa, and the Middle East and Asia Pacific regions, boasting a market capitalization of $0.68 billion.

Operations: The company generates revenue primarily from three geographical segments: Americas, Europe and Africa (EURAF), and Middle East and Asia Pacific (MEAP). It has experienced fluctuations in its gross profit margin, with recent figures showing a gross profit margin of 19.04% as of December 2023. Operating expenses have been a significant component of the cost structure, consistently impacting net income across different periods.

PE: -38.1x

Manitowoc, a small company in the U.S., recently reported third-quarter sales of US$524.8 million, slightly up from the previous year, but faced a net loss of US$7 million compared to last year's profit. Despite these challenges, insiders have shown confidence by purchasing shares within the past year. The firm's earnings are projected to grow 68.5% annually, though it relies on riskier external borrowing for funding and has less than one year's cash runway available.

- Navigate through the intricacies of Manitowoc Company with our comprehensive valuation report here.

Explore historical data to track Manitowoc Company's performance over time in our Past section.

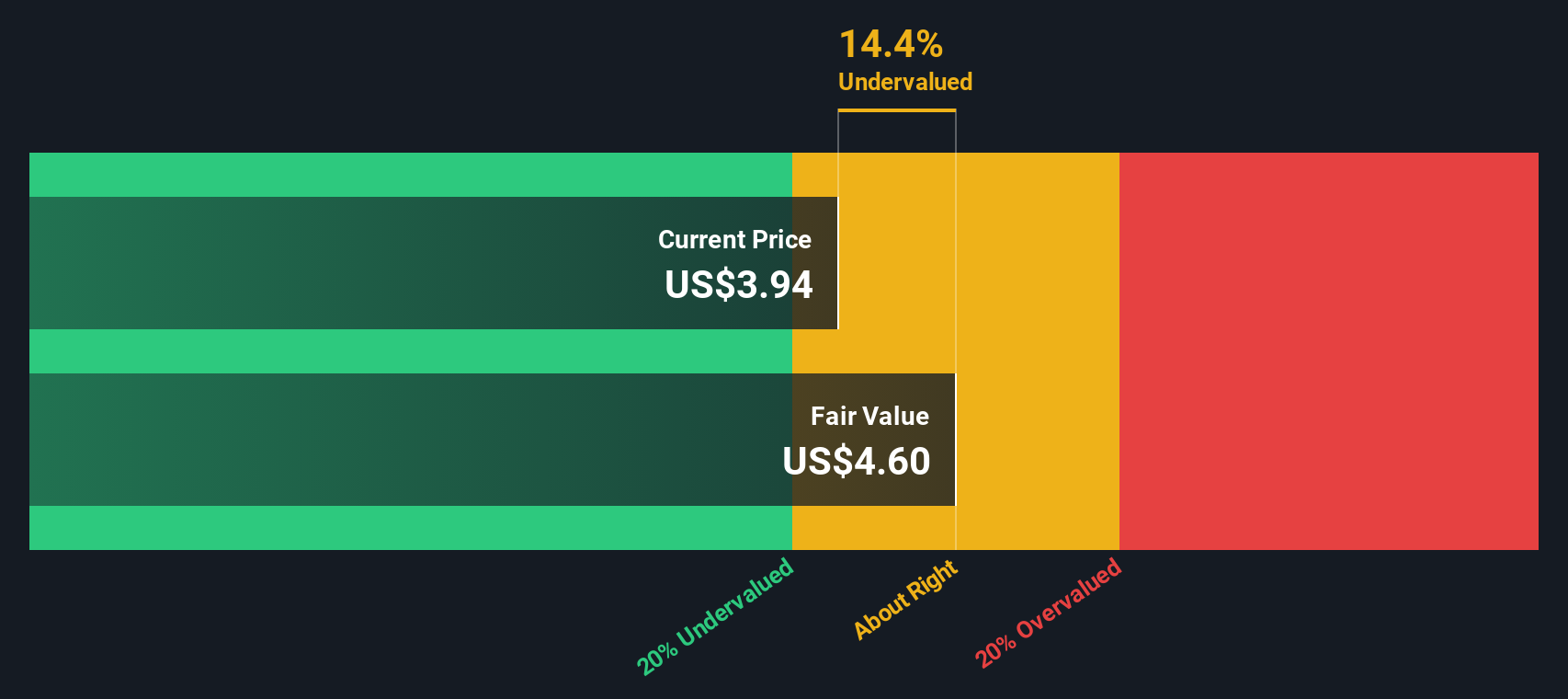

Smith Douglas Homes (NYSE:SDHC)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Smith Douglas Homes operates in the homebuilding business, focusing on constructing residential properties, with a market capitalization of $1.2 billion.

Operations: The homebuilding business generates revenue primarily from sales, with costs of goods sold (COGS) significantly impacting gross profit. Over recent periods, the gross profit margin has shown a declining trend from 29.49% to 26.54%. Operating expenses have increased over time, with notable growth in general and administrative expenses contributing to this rise.

PE: 5.3x

Smith Douglas Homes, a smaller U.S. company, is capturing attention with its recent strategic moves and insider confidence. Lead Independent Director Jeffrey Jackson's acquisition of 8,605 shares for US$256,182 underscores this confidence in the company's prospects. Despite a drop in net profit margin from 17.5% to 4.6%, revenue grew significantly to US$277.84 million in Q3 2024 from US$197.64 million the previous year. The newly launched Ridgeland Mortgage joint venture aims to enhance growth by leveraging Smith Douglas' home-building expertise alongside loanDepot's financial platform across key markets like Atlanta and Houston.

Next Steps

- Investigate our full lineup of 44 Undervalued US Small Caps With Insider Buying right here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:SDHC

Smith Douglas Homes

Designs, constructs, and sale of single-family homes in the southeastern United States.

Excellent balance sheet and slightly overvalued.

Market Insights

Community Narratives