Advertisement

- United States

- /

- Biotech

- /

- NasdaqGM:LUMO

We're A Little Worried About Lumos Pharma's (NASDAQ:LUMO) Cash Burn Rate

There's no doubt that money can be made by owning shares of unprofitable businesses. For example, although Amazon.com made losses for many years after listing, if you had bought and held the shares since 1999, you would have made a fortune. Nonetheless, only a fool would ignore the risk that a loss making company burns through its cash too quickly.

So, the natural question for Lumos Pharma (NASDAQ:LUMO) shareholders is whether they should be concerned by its rate of cash burn. For the purposes of this article, cash burn is the annual rate at which an unprofitable company spends cash to fund its growth; its negative free cash flow. First, we'll determine its cash runway by comparing its cash burn with its cash reserves.

See our latest analysis for Lumos Pharma

When Might Lumos Pharma Run Out Of Money?

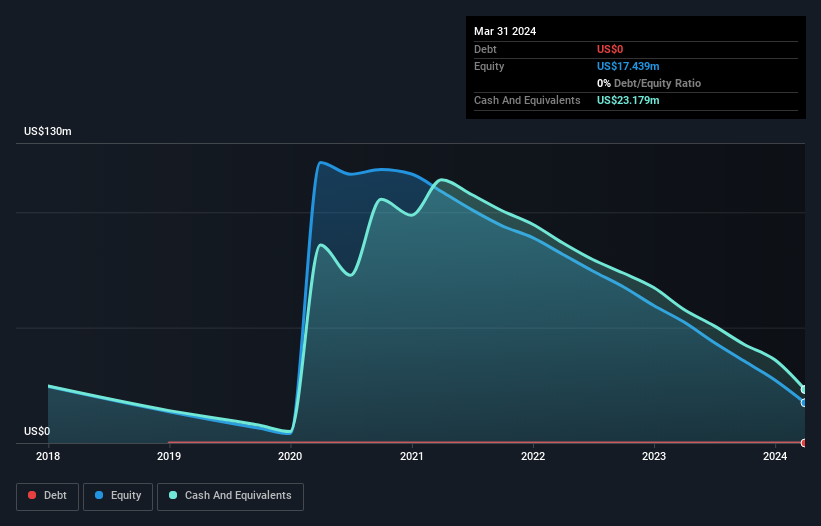

A company's cash runway is the amount of time it would take to burn through its cash reserves at its current cash burn rate. In March 2024, Lumos Pharma had US$23m in cash, and was debt-free. Importantly, its cash burn was US$31m over the trailing twelve months. That means it had a cash runway of around 9 months as of March 2024. To be frank, this kind of short runway puts us on edge, as it indicates the company must reduce its cash burn significantly, or else raise cash imminently. The image below shows how its cash balance has been changing over the last few years.

How Well Is Lumos Pharma Growing?

Some investors might find it troubling that Lumos Pharma is actually increasing its cash burn, which is up 12% in the last year. Also concerning, operating revenue was actually down by 27% in that time. Considering both these metrics, we're a little concerned about how the company is developing. While the past is always worth studying, it is the future that matters most of all. So you might want to take a peek at how much the company is expected to grow in the next few years.

How Easily Can Lumos Pharma Raise Cash?

Lumos Pharma revenue is declining and its cash burn is increasing, so many may be considering its need to raise more cash in the future. Companies can raise capital through either debt or equity. One of the main advantages held by publicly listed companies is that they can sell shares to investors to raise cash and fund growth. We can compare a company's cash burn to its market capitalisation to get a sense for how many new shares a company would have to issue to fund one year's operations.

Lumos Pharma's cash burn of US$31m is about 152% of its US$20m market capitalisation. That suggests the company may have some funding difficulties, and we'd be very wary of the stock.

How Risky Is Lumos Pharma's Cash Burn Situation?

As you can probably tell by now, we're rather concerned about Lumos Pharma's cash burn. In particular, we think its cash burn relative to its market cap suggests it isn't in a good position to keep funding growth. And although we accept its increasing cash burn wasn't as worrying as its cash burn relative to its market cap, it was still a real negative; as indeed were all the factors we considered in this article. Once we consider the metrics mentioned in this article together, we're left with very little confidence in the company's ability to manage its cash burn, and we think it will probably need more money. On another note, we conducted an in-depth investigation of the company, and identified 4 warning signs for Lumos Pharma (1 doesn't sit too well with us!) that you should be aware of before investing here.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies with significant insider holdings, and this list of stocks growth stocks (according to analyst forecasts)

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:LUMO

Lumos Pharma

A clinical-stage biopharmaceutical company, focuses on the identification, acquisition, development, and commercialization of products and therapies for people with rare diseases.

Medium-low with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.8% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor