Stock Analysis

Examining 3 US Growth Companies With High Insider Ownership And A Minimum 18% Revenue Growth

Reviewed by Simply Wall St

As the U.S. stock market experiences mixed signals with the S&P 500 and Nasdaq Composite inching higher amid Federal Reserve rate cut expectations, investors are keenly observing various sectors for growth opportunities. In this environment, companies with high insider ownership and significant revenue growth can be particularly compelling, as these attributes may signal strong confidence from those closest to the company's operations.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| GigaCloud Technology (NasdaqGM:GCT) | 25.9% | 21.3% |

| PDD Holdings (NasdaqGS:PDD) | 32.1% | 23.3% |

| Atour Lifestyle Holdings (NasdaqGS:ATAT) | 26% | 22.1% |

| Super Micro Computer (NasdaqGS:SMCI) | 14.3% | 40.2% |

| Bridge Investment Group Holdings (NYSE:BRDG) | 11.6% | 98.2% |

| Duolingo (NasdaqGS:DUOL) | 15% | 48.1% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 14.7% | 60.9% |

| Carlyle Group (NasdaqGS:CG) | 29.2% | 23.6% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 74.3% |

| BBB Foods (NYSE:TBBB) | 22.9% | 94.7% |

Let's uncover some gems from our specialized screener.

Intuitive Machines (NasdaqGM:LUNR)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Intuitive Machines, Inc. operates in the United States, focusing on the design, manufacture, and operation of space products and services with a market capitalization of approximately $442.94 million.

Operations: The company generates its revenue primarily from the aerospace and defense sector, totaling approximately $134.35 million.

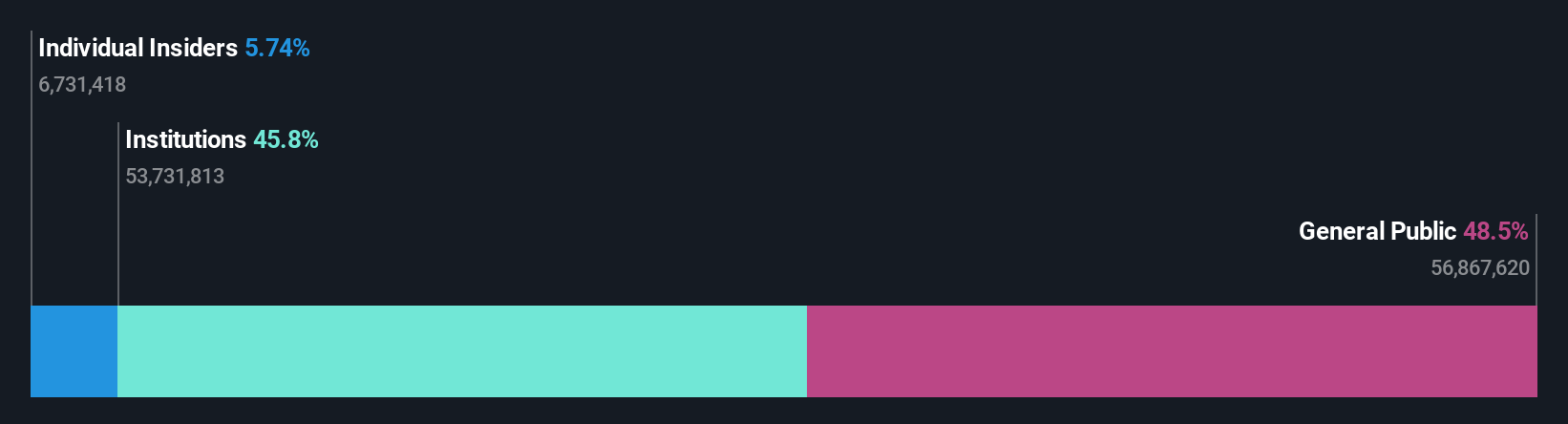

Insider Ownership: 12.8%

Revenue Growth Forecast: 32.6% p.a.

Intuitive Machines, recently added to multiple Russell indexes, reported a significant increase in Q1 sales to US$73.07 million from US$18.24 million year-over-year, despite a widened net loss of US$121.63 million. With high insider ownership and recent substantial insider purchases, the company forecasts 2024 revenues between US$200 - US$240 million, indicating potential strong future growth. Analysts expect the stock price to rise significantly and project earnings growth of 64.65% per annum over the next few years.

- Navigate through the intricacies of Intuitive Machines with our comprehensive analyst estimates report here.

- Our expertly prepared valuation report Intuitive Machines implies its share price may be lower than expected.

New Oriental Education & Technology Group (NYSE:EDU)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: New Oriental Education & Technology Group, with a market cap of approximately $13.17 billion, is a provider of private educational services in China.

Operations: The company generates its revenue from providing private educational services in China.

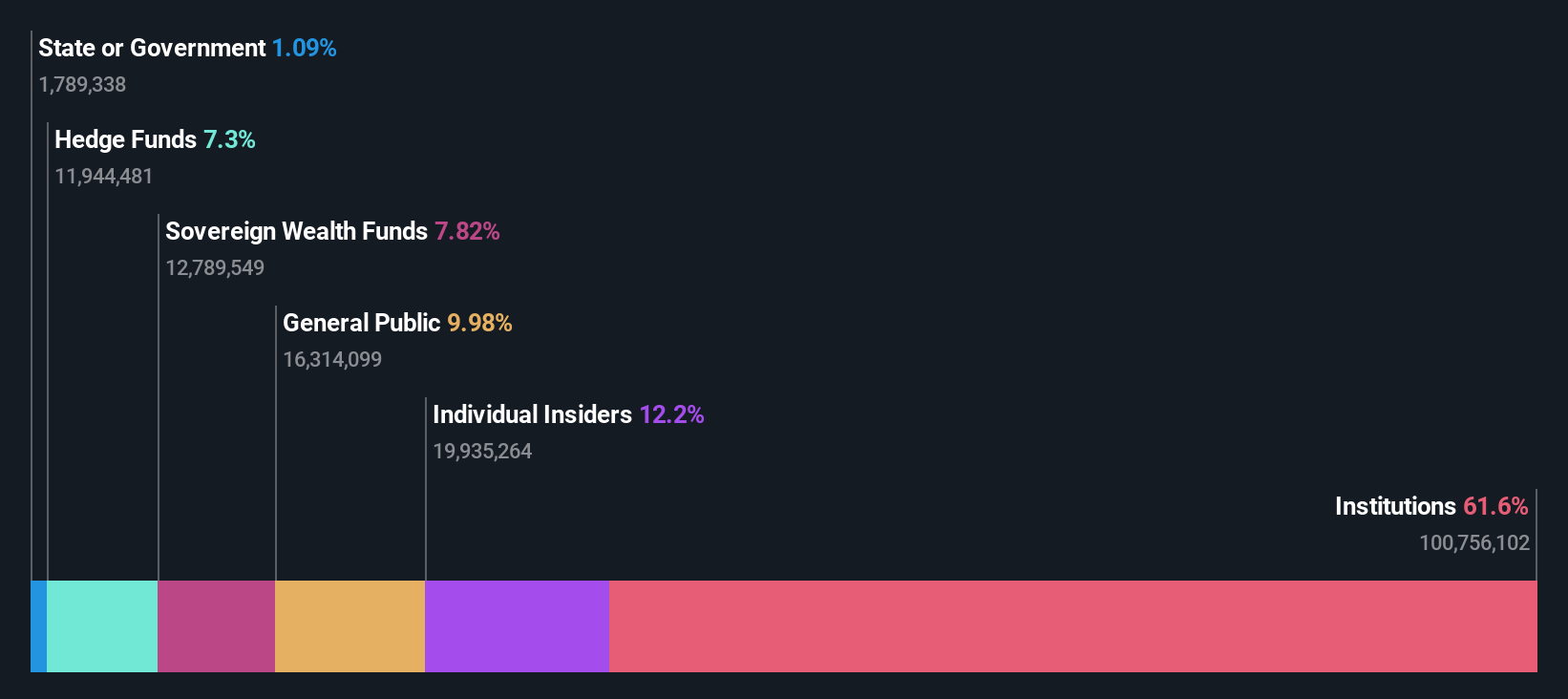

Insider Ownership: 12%

Revenue Growth Forecast: 18.3% p.a.

New Oriental Education & Technology Group, demonstrating robust financial health, reported a substantial increase in quarterly sales to US$1.21 billion and net income to US$87.17 million. The company's revenue is expected to grow by 18.3% annually, outpacing the US market's 8.7%. Despite a low forecasted Return on Equity of 14%, EDU's earnings are projected to surge by 27.7% annually, supported by an extended buyback plan till May 2025, signaling strong future prospects amidst high insider ownership.

- Take a closer look at New Oriental Education & Technology Group's potential here in our earnings growth report.

- Insights from our recent valuation report point to the potential undervaluation of New Oriental Education & Technology Group shares in the market.

MediaAlpha (NYSE:MAX)

Simply Wall St Growth Rating: ★★★★★★

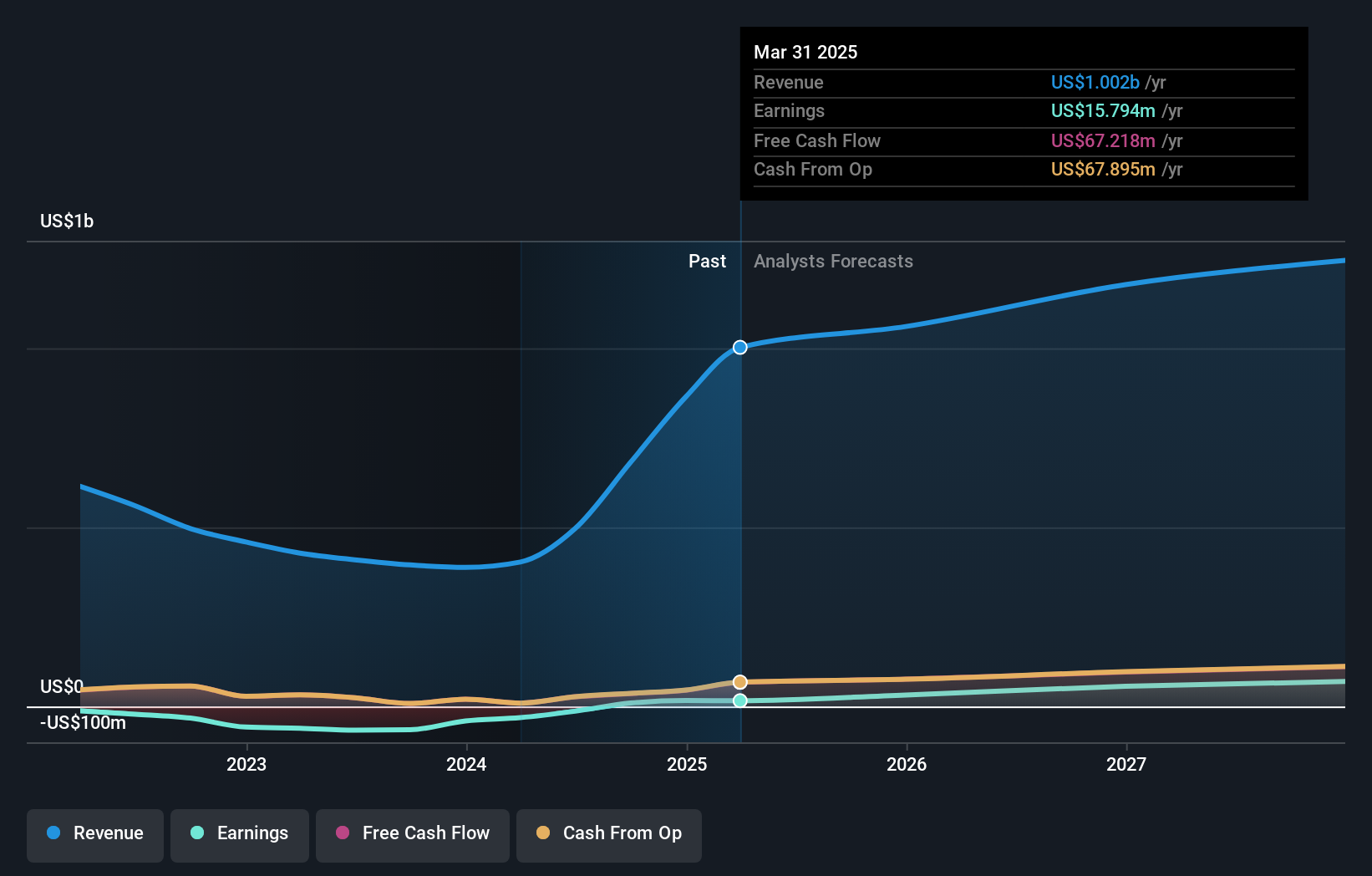

Overview: MediaAlpha, Inc. operates a platform in the United States for acquiring insurance customers and has a market capitalization of approximately $823.70 million.

Operations: The company generates its revenue primarily from the Internet Information Providers segment, amounting to $403.17 million.

Insider Ownership: 13.5%

Revenue Growth Forecast: 20.3% p.a.

MediaAlpha, despite recent exclusions from multiple Russell indexes, shows potential in the growth sector with an expected revenue increase of 20.3% annually, outpacing the US market's 8.7%. The company is projected to turn profitable within three years with a significant forecasted Return on Equity of 114%. However, it currently trades at 53.7% below its estimated fair value and has experienced a net loss reduction from US$10.27 million to US$1.11 million year-over-year as of Q1 2024.

- Click to explore a detailed breakdown of our findings in MediaAlpha's earnings growth report.

- Our expertly prepared valuation report MediaAlpha implies its share price may be too high.

Next Steps

- Unlock our comprehensive list of 181 Fast Growing US Companies With High Insider Ownership by clicking here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MAX

MediaAlpha

Through its subsidiaries, operates an insurance customer acquisition platform in the United States.

High growth potential and slightly overvalued.