- United States

- /

- IT

- /

- NasdaqGS:WIX

Three High Growth Tech Stocks To Watch In The United States

Reviewed by Simply Wall St

Over the last 7 days, the United States market has dropped 1.2%, yet it remains up by 23% over the past year with earnings forecasted to grow by 15% annually. In this dynamic environment, identifying high growth tech stocks involves looking for companies that demonstrate strong innovation and adaptability to capitalize on these promising growth prospects.

Top 10 High Growth Tech Companies In The United States

| Name | Revenue Growth | Earnings Growth | Growth Rating |

|---|---|---|---|

| Super Micro Computer | 24.13% | 24.28% | ★★★★★★ |

| Ardelyx | 22.86% | 54.70% | ★★★★★★ |

| AVITA Medical | 33.33% | 51.81% | ★★★★★★ |

| Alkami Technology | 21.99% | 102.65% | ★★★★★★ |

| Alnylam Pharmaceuticals | 21.39% | 56.40% | ★★★★★★ |

| TG Therapeutics | 30.33% | 44.07% | ★★★★★★ |

| Bitdeer Technologies Group | 50.82% | 122.48% | ★★★★★★ |

| Clene | 61.16% | 59.11% | ★★★★★★ |

| Blueprint Medicines | 22.66% | 55.14% | ★★★★★★ |

| Travere Therapeutics | 29.92% | 61.97% | ★★★★★★ |

Click here to see the full list of 228 stocks from our US High Growth Tech and AI Stocks screener.

Below we spotlight a couple of our favorites from our exclusive screener.

Wix.com (NasdaqGS:WIX)

Simply Wall St Growth Rating: ★★★★★☆

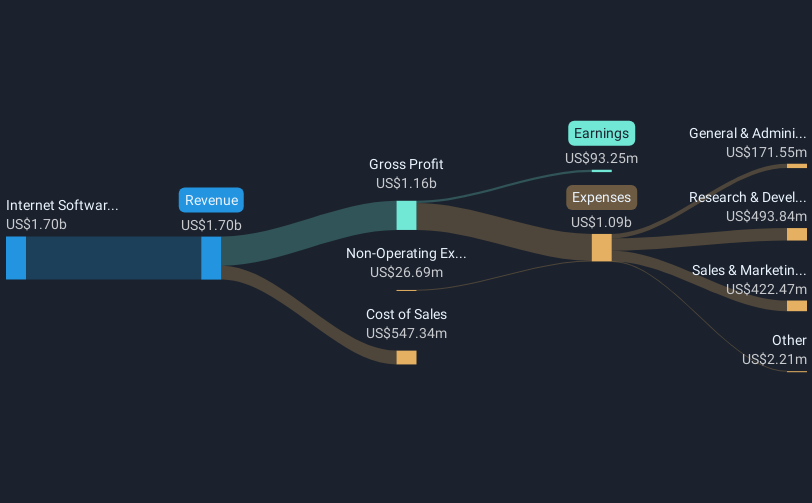

Overview: Wix.com Ltd. operates as a cloud-based web development platform for registered users and creators worldwide, with a market capitalization of approximately $13.23 billion.

Operations: The company generates revenue primarily through its Internet Software & Services segment, amounting to $1.70 billion. It operates as a cloud-based platform catering to web development needs for users globally.

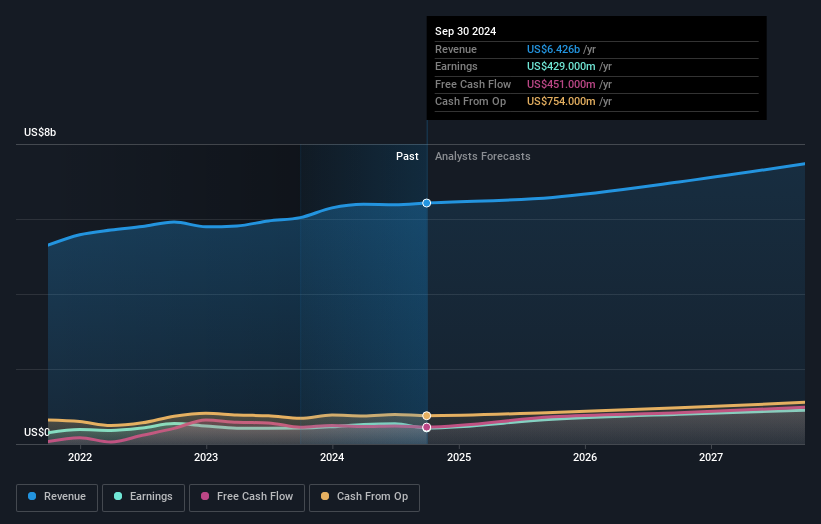

Wix.com has demonstrated a robust trajectory in its tech offerings, notably with the recent launch of AI Site-Chat and strategic alliance with Pantone. These initiatives not only enhance user engagement through 24/7 customer interaction but also place Wix at the forefront of web design innovation by integrating trending colors into user platforms. Financially, Wix reported a significant uplift in quarterly revenue to $444.67 million and net income to $26.78 million, reflecting strong operational execution and market adoption of its advanced features. With an expected annual revenue growth rate of 11.9% and earnings growth forecast at 32.1%, Wix is positioning itself as a dynamic player in the high-growth tech sector, leveraging continuous product innovation and strategic partnerships to expand its market influence.

- Unlock comprehensive insights into our analysis of Wix.com stock in this health report.

Explore historical data to track Wix.com's performance over time in our Past section.

Warner Music Group (NasdaqGS:WMG)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Warner Music Group Corp. is a music entertainment company operating in the United States, the United Kingdom, Germany, and internationally with a market cap of approximately $15.33 billion.

Operations: WMG generates revenue primarily through its Recorded Music segment, which accounts for $5.22 billion, and its Music Publishing segment, contributing $1.21 billion.

Warner Music Group's recent financial performance showcases a steady upward trajectory, with annual sales rising to $6.43 billion, marking a growth from the previous year's $6.04 billion. This aligns with an earnings increase to $435 million, up slightly from $430 million, reflecting resilient operational strength despite industry challenges. The firm also announced a share repurchase program valued at up to $100 million, underscoring its commitment to shareholder value amidst strategic global expansions like its significant investments in India’s diverse music market. These moves illustrate Warner’s proactive approach in both market consolidation and tapping into emerging markets, poised for broader global influence in the music industry.

- Click here to discover the nuances of Warner Music Group with our detailed analytical health report.

Sea (NYSE:SE)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Sea Limited operates in digital entertainment, e-commerce, and digital financial services across Southeast Asia, Latin America, the rest of Asia, and internationally with a market capitalization of approximately $63.43 billion.

Operations: Sea Limited generates revenue through three primary segments: digital entertainment, e-commerce, and digital financial services. The company operates across various regions including Southeast Asia and Latin America.

Despite a challenging year with a significant one-off loss of $196.9 million, Sea Limited has demonstrated resilience and potential for robust growth. With an impressive turnaround from a net loss to a net income this fiscal year, the company reported earnings of $153.32 million in Q3 2024, up from a loss the previous year. This recovery is underscored by an annual revenue growth forecast of 14.4%, outpacing the US market average of 8.9%. Additionally, Sea's commitment to innovation and market adaptation is evident in its R&D expenses aimed at enhancing technological capabilities and expanding its market reach, positioning it well for future scalability in the tech sector. The firm's strategic focus on R&D has not only fueled its recovery but also sets the stage for sustained growth with earnings expected to surge by 37.77% annually over the next three years. This investment in innovation is crucial as it navigates through competitive landscapes and evolving industry demands, ensuring that Sea remains at the forefront of technological advancements while continuing to enhance shareholder value through strategic financial management and operational efficiencies.

- Take a closer look at Sea's potential here in our health report.

Gain insights into Sea's historical performance by reviewing our past performance report.

Taking Advantage

- Get an in-depth perspective on all 228 US High Growth Tech and AI Stocks by using our screener here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade Wix.com, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Wix.com might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:WIX

Wix.com

Operates a cloud-based web development platform for registered users and creators worldwide.

High growth potential with solid track record.

Similar Companies

Market Insights

Community Narratives