Advertisement

- United States

- /

- Interactive Media and Services

- /

- NasdaqGS:WB

Earnings Update: Weibo Corporation (NASDAQ:WB) Just Reported Its First-Quarter Results And Analysts Are Updating Their Forecasts

Last week, you might have seen that Weibo Corporation (NASDAQ:WB) released its first-quarter result to the market. The early response was not positive, with shares down 9.2% to US$8.77 in the past week. Overall the results were a little better than the analysts were expecting, with revenues beating forecasts by 2.1%to hit US$395m. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

Check out our latest analysis for Weibo

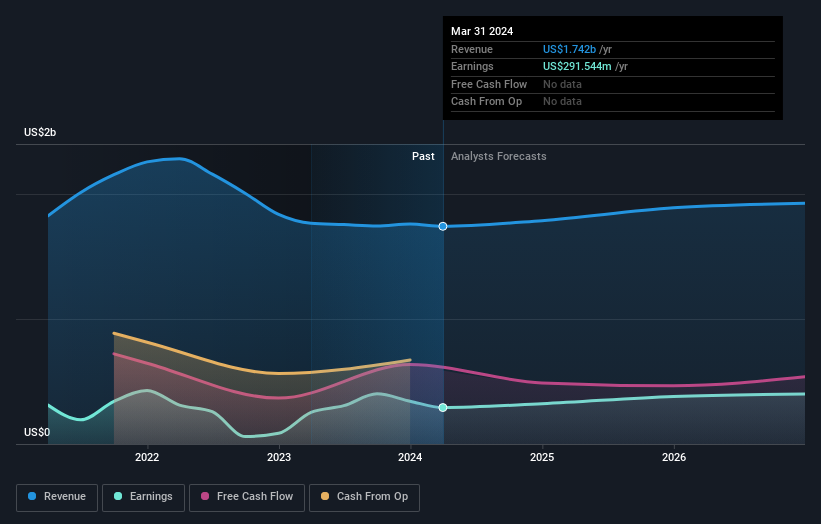

Following the latest results, Weibo's 24 analysts are now forecasting revenues of US$1.79b in 2024. This would be a modest 2.6% improvement in revenue compared to the last 12 months. Statutory earnings per share are predicted to increase 9.4% to US$1.31. Before this earnings report, the analysts had been forecasting revenues of US$1.79b and earnings per share (EPS) of US$1.39 in 2024. The analysts seem to have become a little more negative on the business after the latest results, given the small dip in their earnings per share numbers for next year.

The consensus price target held steady at US$12.14, with the analysts seemingly voting that their lower forecast earnings are not expected to lead to a lower stock price in the foreseeable future. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. The most optimistic Weibo analyst has a price target of US$18.80 per share, while the most pessimistic values it at US$8.60. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. It's clear from the latest estimates that Weibo's rate of growth is expected to accelerate meaningfully, with the forecast 3.5% annualised revenue growth to the end of 2024 noticeably faster than its historical growth of 1.3% p.a. over the past five years. Compare this with other companies in the same industry, which are forecast to see revenue growth of 10% annually. It seems obvious that, while the future growth outlook is brighter than the recent past, Weibo is expected to grow slower than the wider industry.

The Bottom Line

The most important thing to take away is that the analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. On the plus side, there were no major changes to revenue estimates; although forecasts imply they will perform worse than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have estimates - from multiple Weibo analysts - going out to 2026, and you can see them free on our platform here.

You should always think about risks though. Case in point, we've spotted 1 warning sign for Weibo you should be aware of.

Valuation is complex, but we're here to simplify it.

Discover if Weibo might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:WB

Through its subsidiaries, operates as a social media platform for people to create, discover, and distribute content in the People’s Republic of China.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor