- United States

- /

- Interactive Media and Services

- /

- NasdaqGM:RUM

Revenues Tell The Story For Rumble Inc. (NASDAQ:RUM) As Its Stock Soars 34%

The Rumble Inc. (NASDAQ:RUM) share price has done very well over the last month, posting an excellent gain of 34%. Not all shareholders will be feeling jubilant, since the share price is still down a very disappointing 35% in the last twelve months.

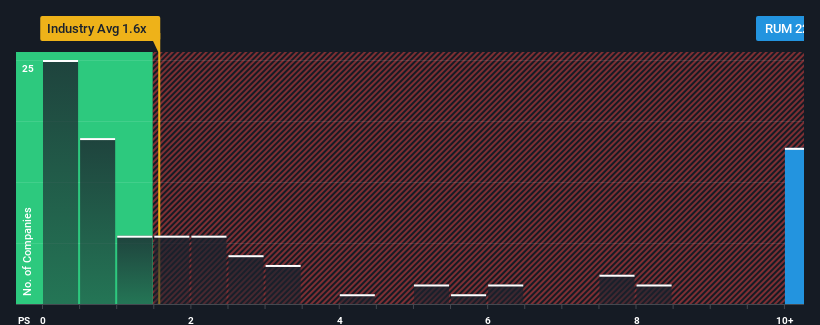

After such a large jump in price, given around half the companies in the United States' Interactive Media and Services industry have price-to-sales ratios (or "P/S") below 1.6x, you may consider Rumble as a stock to avoid entirely with its 22.6x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

View our latest analysis for Rumble

How Rumble Has Been Performing

Recent times have been advantageous for Rumble as its revenues have been rising faster than most other companies. It seems the market expects this form will continue into the future, hence the elevated P/S ratio. However, if this isn't the case, investors might get caught out paying too much for the stock.

Want the full picture on analyst estimates for the company? Then our free report on Rumble will help you uncover what's on the horizon.What Are Revenue Growth Metrics Telling Us About The High P/S?

Rumble's P/S ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the industry.

Retrospectively, the last year delivered an explosive gain to the company's top line. The latest three year period has also seen an incredible overall rise in revenue, aided by its incredible short-term performance. So we can start by confirming that the company has done a tremendous job of growing revenue over that time.

Shifting to the future, estimates from the lone analyst covering the company suggest revenue should grow by 60% each year over the next three years. Meanwhile, the rest of the industry is forecast to only expand by 11% each year, which is noticeably less attractive.

With this information, we can see why Rumble is trading at such a high P/S compared to the industry. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

What We Can Learn From Rumble's P/S?

The strong share price surge has lead to Rumble's P/S soaring as well. Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of Rumble's analyst forecasts revealed that its superior revenue outlook is contributing to its high P/S. It appears that shareholders are confident in the company's future revenues, which is propping up the P/S. It's hard to see the share price falling strongly in the near future under these circumstances.

Before you settle on your opinion, we've discovered 3 warning signs for Rumble (1 makes us a bit uncomfortable!) that you should be aware of.

If these risks are making you reconsider your opinion on Rumble, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:RUM

Rumble

Operates video sharing platforms in the United States, Canada, and internationally.

Flawless balance sheet low.