- United States

- /

- Packaging

- /

- NYSE:SON

Don't Buy Sonoco Products Company (NYSE:SON) For Its Next Dividend Without Doing These Checks

Sonoco Products Company (NYSE:SON) is about to trade ex-dividend in the next three days. The ex-dividend date is one business day before the record date, which is the cut-off date for shareholders to be present on the company's books to be eligible for a dividend payment. The ex-dividend date is important because any transaction on a stock needs to have been settled before the record date in order to be eligible for a dividend. Accordingly, Sonoco Products investors that purchase the stock on or after the 8th of August will not receive the dividend, which will be paid on the 10th of September.

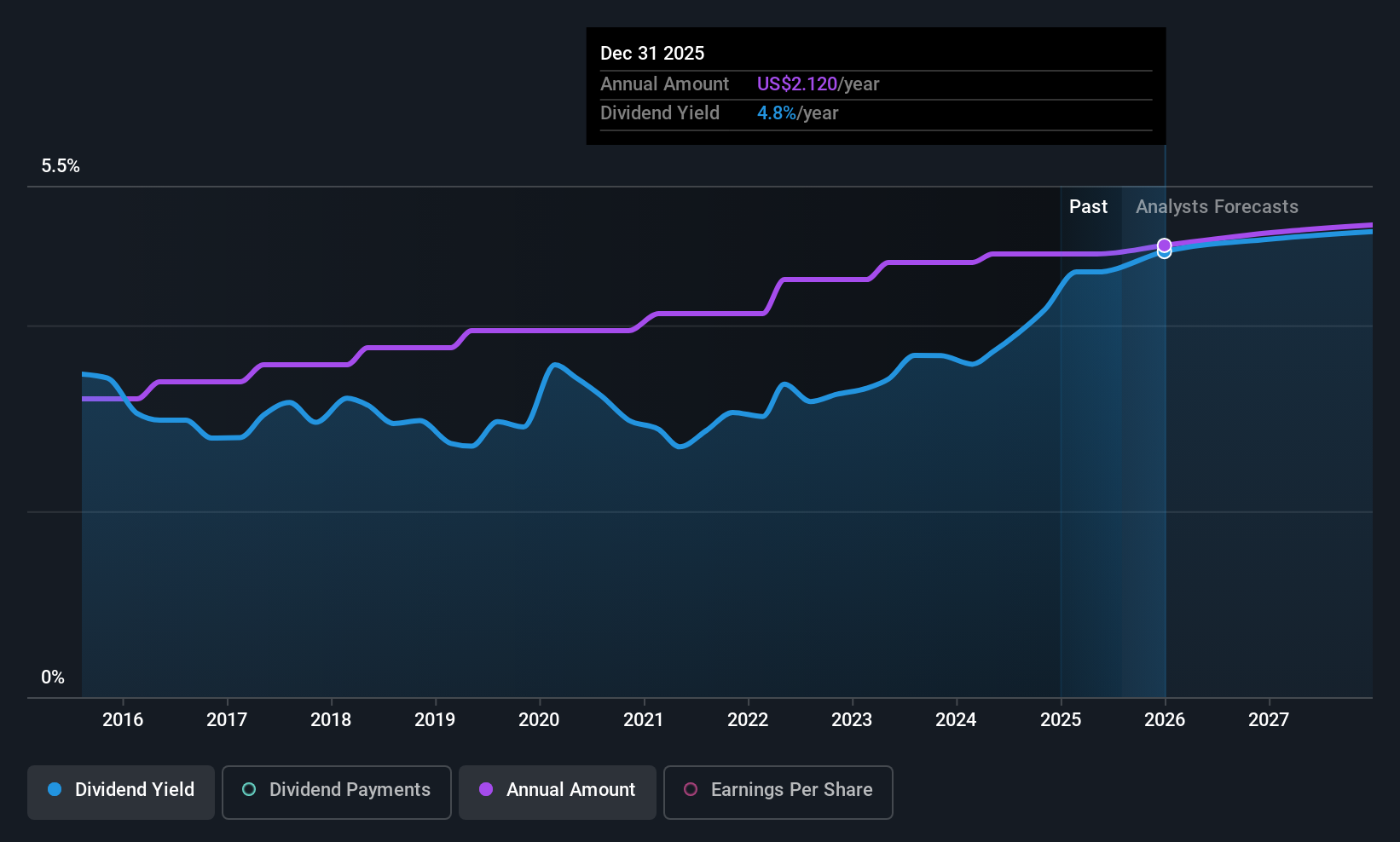

The company's upcoming dividend is US$0.53 a share, following on from the last 12 months, when the company distributed a total of US$2.12 per share to shareholders. Last year's total dividend payments show that Sonoco Products has a trailing yield of 4.8% on the current share price of US$44.24. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. We need to see whether the dividend is covered by earnings and if it's growing.

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. An unusually high payout ratio of 222% of its profit suggests something is happening other than the usual distribution of profits to shareholders. Yet cash flows are even more important than profits for assessing a dividend, so we need to see if the company generated enough cash to pay its distribution. Over the past year it paid out 144% of its free cash flow as dividends, which is uncomfortably high. It's hard to consistently pay out more cash than you generate without either borrowing or using company cash, so we'd wonder how the company justifies this payout level.

Cash is slightly more important than profit from a dividend perspective, but given Sonoco Products's payments were not well covered by either earnings or cash flow, we are concerned about the sustainability of this dividend.

View our latest analysis for Sonoco Products

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Businesses with shrinking earnings are tricky from a dividend perspective. Investors love dividends, so if earnings fall and the dividend is reduced, expect a stock to be sold off heavily at the same time. Sonoco Products's earnings per share have fallen at approximately 20% a year over the previous five years. Such a sharp decline casts doubt on the future sustainability of the dividend.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. In the past 10 years, Sonoco Products has increased its dividend at approximately 5.2% a year on average. That's intriguing, but the combination of growing dividends despite declining earnings can typically only be achieved by paying out a larger percentage of profits. Sonoco Products is already paying out a high percentage of its income, so without earnings growth, we're doubtful of whether this dividend will grow much in the future.

The Bottom Line

Should investors buy Sonoco Products for the upcoming dividend? Not only are earnings per share declining, but Sonoco Products is paying out an uncomfortably high percentage of both its earnings and cashflow to shareholders as dividends. Unless there are grounds to believe a turnaround is imminent, this is one of the least attractive dividend stocks under this analysis. It's not an attractive combination from a dividend perspective, and we're inclined to pass on this one for the time being.

Having said that, if you're looking at this stock without much concern for the dividend, you should still be familiar of the risks involved with Sonoco Products. For example, we've found 4 warning signs for Sonoco Products (2 are potentially serious!) that deserve your attention before investing in the shares.

A common investing mistake is buying the first interesting stock you see. Here you can find a full list of high-yield dividend stocks.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:SON

Sonoco Products

Designs, develops, manufactures, and sells various engineered and sustainable packaging products in the United States, Europe, Canada, the Asia Pacific, and internationally.

Established dividend payer with proven track record.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Unicycive Therapeutics (Nasdaq: UNCY) – Preparing for a Second Shot at Bringing a New Kidney Treatment to Market (TEST)

Rocket Lab USA Will Ignite a 30% Revenue Growth Journey

Dollar general to grow

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Trending Discussion